JPMorgan Soars, UBS Sinks: The 7 Full-Service Banking Tiers You Need to Know in 2024 (Americas Edition)

Tier 1: The Titans

JPMorgan

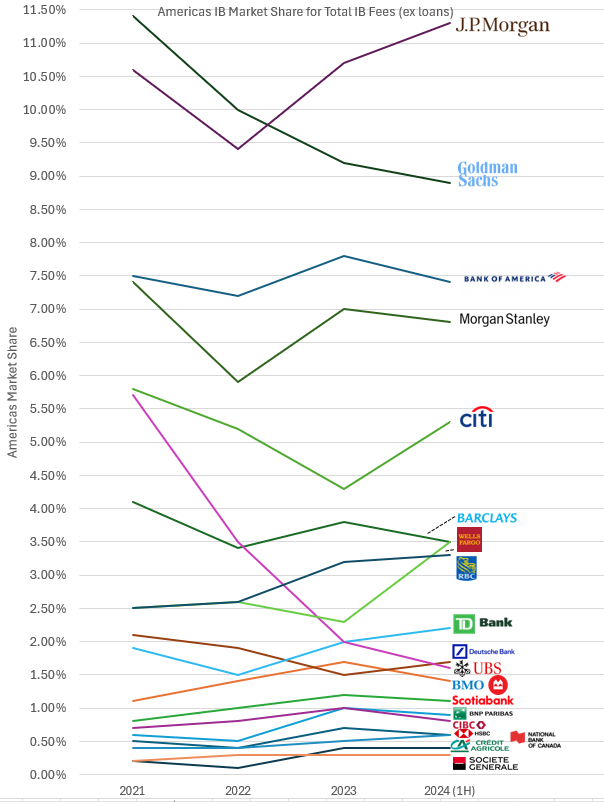

Americas IB Fees Market Share: 11.4% (2020) ➡️ 11.3% (2024)

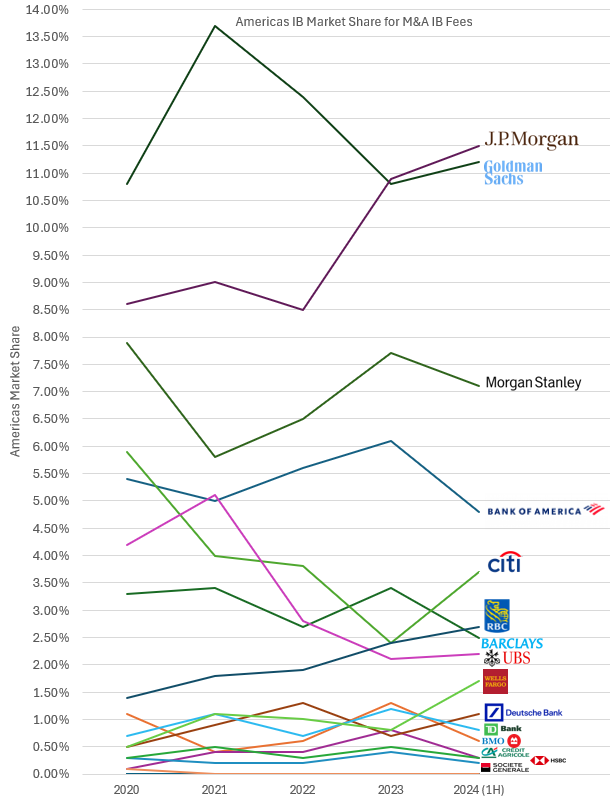

Americas M&A Fees Market Share: 8.6% (2020) ➡️ 11.5% (2024)

With Jamie Dimon at the helm, they're steamrolling the competition. Perhaps he's made a deal with the financial gods.

Americas IB Fees Market Share: 10.4% (2020) ➡️ 8.9% (2024)

Americas M&A Fees Market Share: 10.8% (2020) ➡️ 11.2% (2024)

A minor drop in total fees won't stop them from reminding you they're Goldman Sachs

Tier 2: The Heavy Hitters

Bank of America

Americas IB Fees Market Share: 8.9% (2020) ➡️ 7.4% (2024)

Americas M&A Fees Market Share: 5.4% (2020) ➡️ 4.8% (2024)

When JPMorgan is too busy, clients remember Bank of America exists.

Americas IB Fees Market Share: 7.9% (2020) ➡️ 6.8% (2024)

Americas M&A Fees Market Share: 7.9% (2020) ➡️ 7.1% (2024)

The Bridesmaid: Always the bridesmaid, never the bride. Close to the top but can't quite catch the bouquet from JPMorgan or Goldman.

Citigroup

Americas IB Fees Market Share: 6.9% (2020) ➡️ 5.3% (2024)

Americas M&A Fees Market Share: 5.9% (2020) ➡️ 3.7% (2024)

Their fees are dropping faster than my motivation on a Friday afternoon.

Tier 3: Bake-off Invitee

Barclays

Americas IB Fees Market Share: 4.2% (2020) ➡️ 3.5% (2024)

Americas M&A Fees Market Share: 3.3% (2020) ➡️ 2.5% (2024)

Stiff Upper Lip: Declining fees but keeping calm and carrying on. They might not top the charts, but they add a touch of class—or at least an accent.

Wells Fargo

Americas IB Fees Market Share: 3.5% (2020) ➡️ 3.5% (2024)

Americas Fees Market Share: 0.5% (2020) ➡️ 1.7% (2024)

From Scandal to… Stability?: Holding steady after all that drama. Impressive or expected?

Americas IB Fees Market Share: 2.5% (2020) ➡️ 3.3% (2024)

Americas M&A Fees Market Share: 1.4% (2020) ➡️ 2.7% (2024)

Rising up without making a fuss. Very Canadian of them.

Tier 4: The Lone Ranger

The Toronto-Dominion Bank

Americas IB Fees Market Share: 2.2% (2020) ➡️ 2.2% (2024)

Americas M&A Fees Market Share: 0.7% (2020) ➡️ 0.8% (2024)

The Middle Child: Not enough drama for higher tiers, not enough underperformance for lower ones. Just kind of... there.

Tier 5: The "Going the Wrong Way" Team

Deutsche Bank

Americas IB Fees Market Share: 2.1% (2020) ➡️ 1.7% (2024)

Americas M&A Fees Market Share: 0.5% (2020) ➡️ 1.1% (2024)

The Comeback Kid? Slight M&A fee increase, adorable effort.

UBS

Americas IB Fees Market Share: 4.4% (2020) ➡️ 1.6% (2024)

Americas M&A Fees Market Share: 4.2% (2020) ➡️ 2.2% (2024)

Buying Credit Suisse was like adopting a pet rock—high hopes, no payoff. Example where 1 plus 1 equals less than 1.

Tier 6: The Almost-There Team

Bank of Montreal

Americas Total IB Fees Market Share: 1.2% (2020) ➡️ 1.4% (2024)

Americas M&A Fees Market Share: 1.1% (2020) ➡️ 0.6% (2024)

The Little Engine That Could: Chugging along in Tier 6, they think they can, they think they can... but can they?

The Bank of Nova Scotia

Americas Total IB Fees Market Share: 1.0% (2020) ➡️ 1.1% (2024)

Americas M&A Fees Market Share: 0.3% (2020) ➡️ 0.3% (2024)

The Tortoise Without a Race: Slow and steady—but to where?

Tier 7: The Participation Trophy Recipients

Americas Total IB Fees Market Share: 1.1% (2020) ➡️ 0.9% (2024)

French Fizzle: Bringing a certain je ne sais quoi to underperformance.

Canadian Imperial Bank of Commerce

Americas Total IB Fees Market Share: 0.5% (2020) ➡️ 0.8% (2024)

The Imperial March: Marching in place, that is. Not quite conquering any new territory.

Americas Total IB Fees Market Share: 0.8% (2020) ➡️ 0.6% (2024)

HS-See You at the Bottom: Slowly descending the tiers like they're sightseeing.

National Bank of Canada

Americas Total IB Fees Market Share: 0.4% (2020) ➡️ 0.6% (2024)

National Treasure?: More like a well-kept secret. So secret that even clients can't find them.

Americas Total IB Fees Market Share: 0.3% (2020) ➡️ 0.4% (2024)

Agricultural Roots: Maybe they should stick to farming because the banking harvest isn't looking too good.

Americas Total IB Fees Market Share: 0.3% (2020) ➡️ 0.3% (2024)

So-So-ciete Generale: Not bad enough to be infamous, not good enough to be famous.

Dealogic as of July 1 2024

congrats on being a virgin!

Thanks! At least one of our assets is still untouched by a down market. 😏

Good new is that in a down market you’ll get laid

.

.

.

.

.

.

off.

Why are so many prospects and/or RBC analysts lying about their status on this site? Let's be so real here most people go into IB for exits and UBS and DB exit better than WF, RBC, and TD by very significant margins. Headhunters still consider them BB's whether you like it or not and they don't consider WF, RBC, or TD one. Same idea as Greenhill, where they are like not top even 20 in M&A but exit way better than all the MM firms that are ranked higher like WF or RBC.

Thanks for the clarity, Professor Prestige. I'll update my spreadsheet right away! We all look forward to your exit rankings supported by hearsay. 👏

Not by hearsay, backed up by data and evidence from friends at those firms vs friends at the MM's. UBS's top groups have people that end up at MFs and UMMs pretty frequently, not the case for the MMs mentioned. Same deal with DB. Not the same for RBC/WF, where a lower-side of UMM fund size is about the best you'll get and it's even worse for TD. It's just a matter of fact, not dissing those firms but they simply exit worse. I am at an MM as well btw, and just think this website has gone too much on the pro-MM side of things to where we are just misleading prospects. If you are trying to maximize exits, you should take the BB/EB offer. Some people on this website are out here telling people to take TD over DB like cmon man, it's getting kinda ridiculous.

Edit: Anyone who downvotes this literally just hasn't looked at exit data for any of those firms and it shows. It's fine to want to feel better about being at RBC/WF, but it's not fine to willingly mislead prospects and interns just so you can feel better.

Curious (not in IB which explains my ignorance) - what makes a non BB (like a tier 2 IB) that much inferior to a BB. It’s sounds like these firms should be avoided

MS dropping

Congrats on managing to land 3 offers from JPMorgan, RBC and Wells Fargo!

Also adding on to above comment. Rankings are meaningless just like university rankings are meaningless. A few year fluctuation in league table ranking (which nobody really cares about/looks at) doesn't suddenly delete the historical pipeline of candidates at top PE firms/ PE seniors background and desire to hire people from same bank/ PE seniors perception of bank etc etc. This is why UBS etc have better exits than Wells fargo/RBC and it isn't debatable. Same reason why banks recruit more from low tier Ivies which rank poorly in league tables these days vs state schools which rank above them.

Greenhill is the absolute greatest example of this, not even t20 in M&A fees or IB fees... still treated as an EB in terms of recruiting and has better exits than rapidly growing and much stronger atm franchises like Jefferies and RBC.

Agree but also part of that is due to EB model which have proportionally less deal fees in league tables than banks which lend because they A) don't lend so aren't able to stick their name on as an advisor when they only did a bit of financing and B) do less deals due to smaller size (the deals they do are usually large cap), so for analyst experience it doesn't matter given small class size.

No need to apologize for UBS recent performance or lack therof

There’s this bank called “touching grass capital” you should check out

Never heard of them, any info?

Is BofA truly above Morgan Stanley? lol

Yeah for total fees cause of lending

I believe this excludes lending. Likely capital markets and trading?

PF UBS could be pretty high in the LTs

This combination would still be even behind BofA pf.

Also based on recent deals appears like only the non deal generating half of Barclays came over to UBS.

Today’s Direct TV - Dish had a sponsor involved yet UBS still snubbed while Barclays was on it along with PJT, JPM, BofA, Evercore, LionTree and MS.

https://ir.echostar.com/news-releases/news-release-details/directv-acqu…

Math only works (10% share) using Past Forma and rather than Pro Forma values

Congrats on the JPM role, coping hard

Now do Europe

Please remove gridlines intern

Wanted to easily see how far GS and UBS have each fallen

Thank you for not using the new logo

Would be interesting to see similar stats in the AsiaPacific market

Imagine UBS buying CS, getting all the talent from Barclays just to be within a whisker of BMO for total IB fees

Apologies for the spillover but I’m tired of misleading rhetoric like this.

Considering JPM has multiples of the # of bankers and balance sheet as GS / MS I wouldn’t say this is impressive at all. Honestly, even if they grow in market share, as they keep hiring more bankers, the less impressive they appear to me. When everyone and their brother works as a JPM banker, it reduces the appeal.

This also makes exits per capita even more uphill (without even getting into discussions about stifling oncycle) while making fees per head stagnant for pretty much everyone.

I know people in M&A and other groups who were essentially forced to stay on as a 3rd year analyst because they couldn’t exit well and because there were so many associates above them. You might say well it’s a performance factor but this rarely happens at MS / GS. If it were a performance thing that just means JPM doesn’t attract the talent that GS / MS does in the first place.

This is a bizarre cope and completely inaccurate with respect to # of bankers.

Did you look at M&A market share? Is it really your contention that JPM has 60%+ more bankers than MS? Have seen many revenue per head stats that fly directly in the face of this assertion.

Obviously true about balance sheet but that's a weird way to caveat leadership.

If JPM is the only firm in the list with stable IB market share and significant increase in M&A fees, who are getting the other increases? I can see RBC is one on the IB market share front, but who else? All the other firms ex. GS and WF saw decreases in market share.

My thought was EBs but would like to seek clarity.

Dealogic pull did not appear to include EBs, but can also take some market share as well as other mm firms. These look like just a handful of the main ones but thouhsands of shops out there doing deals

I think RBC deserves to be amongst the heavy hitters

Well I'm clearly not looking to 'exit' but you definitely don't want to be at a bank losing market share even if it has a legacy name if you're VP or above. Prestige with HH means very little at this point, lol. Although it's quite staggering to see all the juniors on the site clamor for exits when through experience I know that very few will stay at where they are so focused on exiting to.

Wells tripled market share in 4 years, impressive!

Never heard a good anecdote about working at a French bank.

Agree

bump

Good post

Laboriosam dolorem sapiente error esse culpa asperiores. Eveniet laudantium consequuntur nam ut eius asperiores. Enim atque dolor est voluptate quod sed occaecati. Voluptates quia sequi quibusdam quam et distinctio laborum. Porro sit consequatur explicabo cum in quasi voluptatem est.

Quia cupiditate deserunt sapiente perspiciatis. Distinctio impedit unde sit et exercitationem non laborum. Eveniet maxime repellendus occaecati iure id. Modi et alias rerum similique et. Error et voluptatem sit iure molestiae maiores laborum. Occaecati modi eum rerum ab sit voluptatum.

Enim occaecati veritatis ad ut. Nulla eveniet rerum qui placeat sequi pariatur. Praesentium occaecati consequuntur est. Ut nesciunt aut hic ut veniam tempora.

Ut doloremque tempora fugiat dolorem similique rerum. Nemo ut cum perferendis eaque et necessitatibus. Ut eum aut accusantium ut.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Consectetur consequatur voluptatem sunt tempora id. Qui iusto in consectetur error ab porro. Molestiae recusandae optio dolorem id amet sed ad. Adipisci sit et explicabo est. Tenetur corrupti qui aperiam reprehenderit est eius nam. Voluptas reiciendis laborum qui quia nobis at cum.

Animi aut quo voluptatem animi. Et sint neque voluptatum. Rerum non assumenda ab accusantium.

Dolor a deserunt iure quaerat voluptate quo perspiciatis. Inventore sed quas nisi. Debitis suscipit rem neque optio provident distinctio. Doloremque sed et pariatur dolorem illo accusamus nobis ut. Ipsam tempore minima enim quod. Eaque rerum repellendus voluptas similique labore recusandae aut. Ut numquam veritatis quos possimus aliquam.

Sequi aliquam eum reiciendis magni qui iste sed dolores. Nihil sapiente rem vel et est deleniti ea. Quia qui porro quos corrupti qui et dolores. Commodi ex est exercitationem voluptas.

Quis qui expedita illo consectetur consectetur odit. Neque nesciunt natus unde fuga aliquid expedita dicta. Voluptatibus suscipit veniam nam sequi.

Ea suscipit vitae et ducimus dolorum labore consequatur. Et est numquam repellat.

Velit totam quis quas voluptates similique. Atque suscipit quae sunt. Aut quo at ipsum voluptas sunt.