SEC Schedule 13E-3

It is a form that any publicly traded company or an affiliate must file with the United States Securities and Exchange Commission (SEC) when "going private."

What Is SEC Schedule 13E-3?

SEC Schedule 13E-3 is a form that any publicly traded company or an affiliate must file with the United States Securities and Exchange Commission (SEC) when “going private.”

A company may choose to go private for several reasons and implement various mechanisms, like a tender offer or asset sale.

Events qualifying for delisting shares from a securities exchange and filing Schedule 13E-3 may include a sale of assets, a tender offer, a merger, or a reverse stock split.

After filing a Schedule 13E-3 form, the company is delisted from the stock exchange, and the company’s shares are no longer traded on the open public marketplace.

The Securities Exchange Act of 1934 considers the following activities as criminal activities:

-

Trading on “material inside information”

-

Abusing discretionary authority

-

Trading excessively or Churning to make commissions

-

Exercising discretion without authority

An acquirer may purchase a target company’s shares because they feel the market is undervaluing the shares or avoiding scrutiny, as when a company goes private, its stock is no longer available for sale in the open markets.

The SEC Schedule 13E-3 requires a disclosure on the purposes of the transaction, whether the transaction is fair to unaffiliated shareholders, and any alternatives the company considered.

The SEC demands that companies disclose whether and why any of their Board of Directors disagreed or abstained from voting on the transaction and whether a majority of directors who are not company employees approved the transaction.

- SEC Schedule 13E-3 is vital when a public company goes private, triggered by events like asset sales or mergers.

- Companies file Schedule 13E-3 when they engage in events like the sale of assets, tender offers, mergers, or reverse stock splits, leading to the delisting of their shares from public stock exchanges.

- Going private allows firms to focus on long-term strategies, shed compliance obligations, gain tax benefits, and reduce shareholder challenges.

- Companies can choose from various structures like mergers or stock splits when going private.

- Schedule 13E-3 demands comprehensive disclosures about transaction fairness, funding sources, and contractual relationships.

Key Motivations for Going Private

A corporation may consider going private for several reasons, including:

-

Focus on long-term strategy: A public company is often pressured to meet analyst expectations and financial forecasts. By going private, a company may be able to focus on long-term strategic moves rather than short-term profits.

-

Elimination of mandatory public company disclosure and compliance obligations: Public companies must file periodic disclosures with the SEC under the Securities Exchange Act of 1934.

These public companies also must comply with the Sarbanes-Oxley Act of 2002, which imposes certain requirements on a public company’s financial disclosure, internal controls, and corporate governance.

In addition, these public companies must comply with the stock exchange rules on which their stock is traded.

Compliance with all these requirements often involves:

-

Disclosure of sensitive information about the company and its business,

-

Exposure of senior executives to personal liability for certain compliance failures and

-

Significant accounting, legal, and other expenses.

Going private eliminates a company’s obligations to comply with these requirements and the associated risks and costs.

The benefits of going private are:

-

Tax Benefits. When achieved through a leveraged buyout (LBO), the target and acquirer may realize the tax benefits of a more leveraged capital structure acceptable to the target as a public company.

-

Elimination of minority stockholder base: The controlling stockholder and management can be challenged by a vocal minority stockholder base through the courts or the proxy process. Considering that controlling shareholders may owe fiduciary duties to minority shareholders, buying out the minority can eliminate the distractions of dealing with unhappy shareholders and reduce the litigation risk to the controlling stockholder.

Going private does have disadvantages. A going private transaction results in the deregistration and delisting of the company’s stock.

The newly formed private company will no longer have visibility with the general public or easy access to the capital markets, a liquid acquisition currency.

Moreover, if a going private transaction is financed, the company may be saddled with a heavy debt load after closing.

Items Included in SEC Schedule 13E-3

The following items are included in Schedule 13e-3:

- Item 1 - Issuer and class of security subject to the transaction

- Item 2 - Identity and background of the individuals

- Item 3 - Past contacts, transactions, or negotiations

- Item 4 - Terms of the transaction

- Item 5 - Plans or proposals of the issuer or affiliate

- Item 6 - Source and amount of funds or other considerations

- Item 7 - Purpose, alternatives, reasons, and effects

- Item 8 - Fairness of the transaction

- Item 9 - Reports, opinions, appraisals, and certain negotiations

- Item 10 - Interest in securities of the issuer

- Item 11 - Contracts, arrangements, or relationships with respect to the issuer’s securities

- Item 12 - Present intention and recommendation of certain persons with regard to the transaction

- Item 13 - Other provisions of the transaction

- Item 14 - Financial information

- Item 15 - Persons and assets employed, retained, or utilized

- Item 16 - Additional information

- Item 17 - Material to be filed as exhibits

- Loan Agreements

- Fairness Opinions and Appraisals

- Contracts and Other Agreements

- Disclosure Materials Sent to Security Holders

- Statement of Appraisal Rights and Procedures

Applicability of Rule 13E-3

Rule 13e-3 under the Securities Exchange Act of 1934, the Securities and Exchange Commission’s going private rule, makes it illegal for an issuer or its affiliates to affect a going private transaction unless certain detailed disclosure requirements are met.

The rule seeks transparency for its stockholders and stakeholders, susceptible to manipulative tactics and other potential coercion by the parties to the going-private transaction.

Generally, parties to a going-private transaction subject to Rule 13e-3 must file a Schedule 13E-3 with the SEC and amend or update the filing as necessary.

The schedule is filed in addition to, and not in place of, proxy or information statements, tender offer documents, or other SEC filings required in connection with the transaction.

Excepted Transactions

Rule 13e-3 contains exceptions for certain transactions that otherwise would be subject to the rule.

1) Rule 13e-3(g)(1): Tender Offer/” Clean Up” Transaction

Under Rule 13e-3(g)(1), an acquirer who has become an “affiliate” of the issuer by a tender offer can engage in a “clean-up” transaction within one year of the termination of the tender offer as long as the consideration offered in the clean-up transaction is at least equal to the highest consideration offered in the tender offer and certain other conditions are met.

2) Rule 13e-3(g)(2): Issuer Stockholders Receive Equivalent Equity Securities

Another important exception is Rule 13e-3(g)(2), which provides that Rule 13e-3 does not apply to transactions in which the issuer’s stockholders receive equivalent equity securities.

Such transactions are viewed by the SEC as being outside the purpose of Rule 13e-3 since stockholders maintain an equity interest and are not being “cashed out.”

The SEC has stated that the exception applies if stockholders are offered the opportunity to elect either cash or stock consideration so long as the cash is substantially equivalent to the value of the stock consideration offered. Both options are offered to all stockholders.

When to File SEC Schedule 13E-3?

When the schedule must be filed depends on the structure of the going private transaction.

-

For one-step mergers, Schedule 13E-3 is filed at the same time as the preliminary or definitive proxy statement or information statement filed in connection with the transaction.

-

For tender offers, this schedule is filed as soon as practicable on the date the tender offer is first published or distributed to stockholders.

-

For other going private transactions in which a proxy statement or tender offer documents will not be filed, the schedule is filed at least 30 days before the first purchase of securities.

If the issuer will be taken private through a series of transactions, then the scheduled disclosure must be filed concerning the first transaction and amended with each subsequent transaction.

For example, if the acquirer plans to buy shares of the issuer’s stock on the open market and then launch a tender offer, the schedule should be filed before the market purchases and amended once the tender offer is launched.

Note that, under Rule 13e-3(f)(1)(i), the Schedule 13E-3 disclosure must be provided to stockholders no later than 20 days before the purchase of shares, stockholder vote, or other corporate action.

The rule thus imposes an effective 20-day waiting period on consummating a going private transaction.

SEC Schedule 13E-3 Requirements

The only substantive consequences are that these transactions must meet a minimum waiting period and certain filing requirements.

The disclosure requirements largely mirror the tender and proxy offer rules, except for a few additional items. The disclosures required by Rule 13e-3 will generally be provided in the proxy statement or offer to Schedule 14D-9/purchase for the transaction, as the case may be.

The target and affiliates (if any) engaged in the transaction must file a Schedule 13E-3 incorporating this information.

The areas where additional disclosures are required are:

1. Fairness of the Transaction

The filing person must provide information regarding the fairness of the transaction.

It includes the beliefs of the filing person such as

-

Whether the transaction is fair to unaffiliated shareholders.

-

Whether the transaction requires the approval of at least a majority of unaffiliated stockholders.

-

A fair discussion of the “material factors” upon which the belief is based.

-

Whether a majority of the non-employee directors approved the transaction.

-

Whether a majority of the non-employee directors retained an unaffiliated representative on behalf of the unaffiliated stockholders to negotiate the terms of the transaction.

-

And whether directors abstained or dissented from voting on the transaction, and if so, why.

2. Reports, Opinions, Appraisals, and Negotiations

The disclosures must also include a description of all reports (including oral reports), appraisals, and opinions from outside parties who are” materially related “to the transaction or related to the price or fairness of the transaction.

A copy of each report, appraisal, or opinion must be filed as an exhibit to Schedule 13E-3 as the SEC takes an expansive view of the reports covered.

The target and its affiliates, along with their advisors, should be aware that a few documents that may need to be disclosed and filed with the SEC, such as banker board books and other materials from outside parties, including preliminary materials, shared with the target or its affiliates, including any acquirer who is an affiliate,

Events That Trigger SEC Schedule 13E-3

Private equity firms often purchase a struggling company, reorganize its capital structure, turn it into a private entity, and issue stocks once a profit can be realized.

Two methods private equity firms or influential individuals use to take private companies include a management buyout (MBO) and a leveraged buyout (LBO).

In a management buyout (MBO), the company’s management team purchases the assets and the operations of the business they manage. This often appeals to professional managers due to the greater rewards of being owners of the company rather than employees.

In a leveraged buyout (LBO), a company will acquire another using borrowed money, called leverage, to meet the acquisition cost. The company’s assets are often used as collateral for the loans and acquiring company’s assets.

Leveraged buyouts allow companies to make more significant acquisitions than usual, as they do not have to commit as much capital upfront.

Either way, the company's shareholders decrease to the point that it is no longer needed to file reports with the Securities Exchange Commission, such as a quarterly 10-Q or annual 10-K, along with a Form 8-K for material changes outside of a regular reporting period.

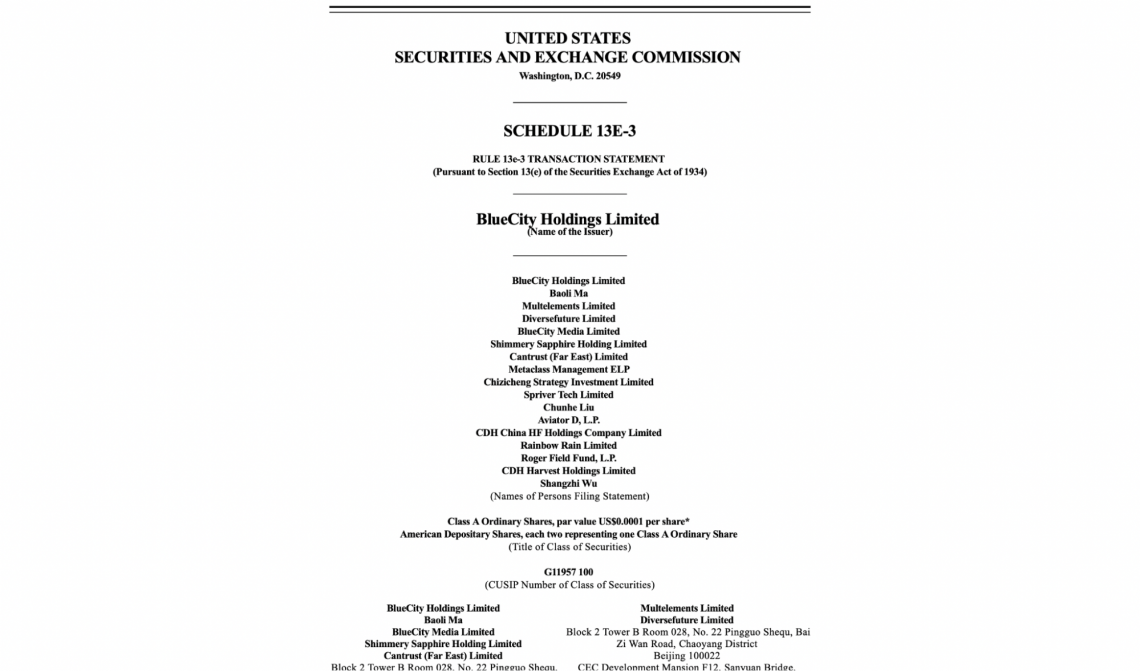

Example of the SEC Schedule 13e 3: Founded in 2011, Blue City Holdings Limited (Nasdaq: BLCT) has become a world-leading online LGBTQ platform that provides a comprehensive suite of services to foster connections and enhance the well-being of the global LGBTQ community through our platforms.

On 25th May 2022, Blue City Holdings filed a Schedule 13e 3 with the SEC.

SEC Schedule 13E-3 FAQs

Yes, filling it is mandatory when "going private".

Yes, all companies must fill the schedule when "going private".

No, these schedules are documents that are made publicly available, free of cost.

All schedule filings are available to the public via the SEC's EDGAR database or on the company’s own website.

or Want to Sign up with your social account?