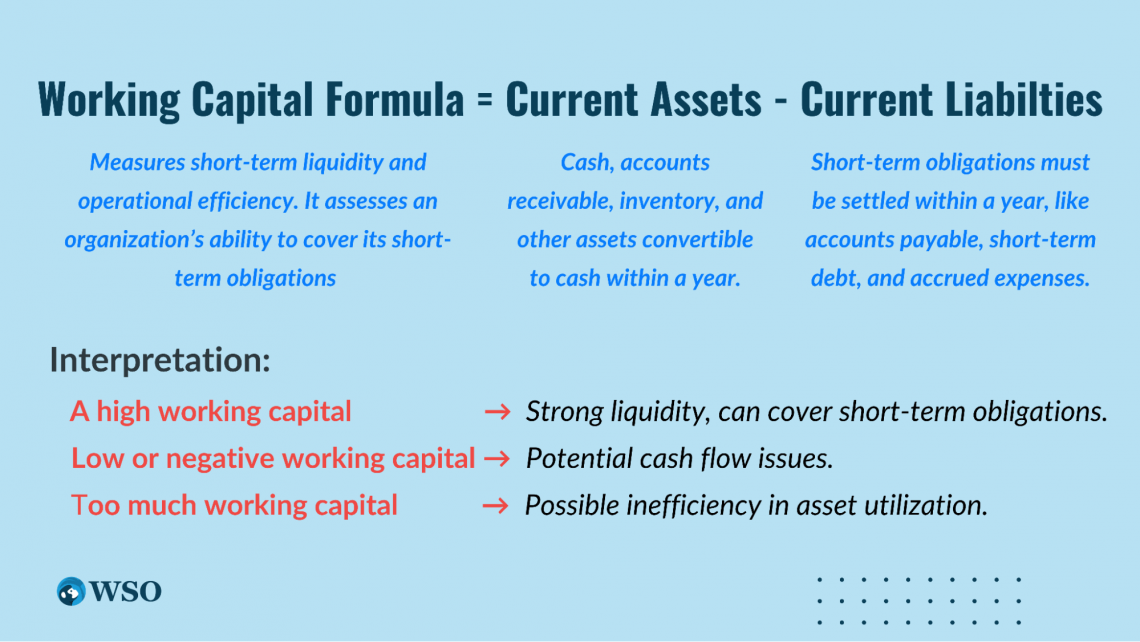

Working Capital Formula

A financial metric used to measure a company's short-term liquidity

What Is The Working Capital Formula?

The Working Capital formula calculates the difference between current assets listed in the balance sheet and current liabilities also listed in the balance sheet. This gives us a quick peek at a company’s short-term financial health and liquidity.

Working capital formula:

Working Capital = Current Assets - Current Liabilities

Although it is a simple addition and subtraction calculation, the formula tells us a lot about a firm's liquidity. Simply put, it tells you how much money a company can quickly get to pay the people knocking on their door that they borrowed money.

A company's balance sheet is all you need to calculate working capital. The following is a simple example.

-

Current assets = $500,000

-

Current liabilities = $350,000

-

Working capital = $150,000 ($500,000 - $350,000)

From this, we can see the company has $150,000 more current assets than current liabilities, or their net working capital is $150,000. This means they are pretty liquid, can meet all short-term debts with their current short-term liabilities, and have an extra $150,000 left over.

-

The working capital formula is current assets minus current liabilities, which can be found on the balance sheet.

-

A positive working capital indicates a firm’s ability to cover short-term liabilities. At the same time, a negative working capital shows the firm will have trouble covering these liabilities.

-

A positive working capital is desirable for a company’s financial health, but excessively high levels indicate a poor use of resources.

-

Too much working capital can indicate poor allocation of resources, while a moderate positive working capital is a good indicator of optimal financial health.

-

There are other formulas that indicate working capital, like the current ratio – another form of the working capital formula that divides current assets by current liabilities.

What Is Working Capital?

Working Capital is the difference between a company’s current assets and current liabilities. It is found using a formula that takes a firm's short-term assets and subtracts its short-term liabilities to determine how much greater short-term assets are than short-term liabilities.

This measure focuses on whether a company has enough liquid assets to pay off its liabilities that are coming due within the year. This is a short-term, near-sighted measure that allows a firm to assess how they are using their finances.

Suppose the working capital formula returns a positive value. In that case, a company has extra assets that can be used to invest in other projects, pay down other debt, issue dividends, or buy back shares. This indicates an efficient company ready to handle unexpected events or disasters.

If a firm has more short-term liabilities than short-term assets. In that case, the formula will yield a negative WC number, indicating the firm will have liquidity issues and have trouble paying its short-term liabilities.

This is a sign that a company may have trouble paying its debts in the near future.

Working Capital Components

The main components of WC are directly in the formula of current assets and current liabilities.

All of these components can be located on a company’s balance sheet. Current assets include items such as cash, cash equivalents, accounts receivable, inventory, marketable securities, prepaid liabilities, other liquid assets, and more.

What Are The Current Assets?

They are items on the balance sheet expected to provide the firm with economic value in the next year and can be easily liquidated. They are expected to be used in one year.

Some examples are:

-

Cash: Cash on hand is a primary current asset. Cash is deemed to be a current asset because it is liquid and can be spent in whatever capacity the firm decides.

-

Cash equivalents: These are items on a company’s balance sheet, like short-term government bonds, money market funds, or other safe financial instruments that can be sold for cash quickly.

- Since they can be converted to cash quickly, usually within three months, they are considered current.

-

Marketable securities: These are similar to cash equivalents but are slightly riskier and may take longer to convert to cash. Marketable securities include stocks and bonds and may take longer to convert to cash but can still be done relatively quickly.

-

Inventory: This is a current asset that will show up most of the time in a working capital equation, as it will be a substantial amount for some companies. It is a current asset because it is expected to provide future benefits to the company within a year.

-

Accounts receivable: It is another current asset that will make up most of a company’s financial statements. Accounts Receivable will sometimes be higher depending on how much sales a company produces on credit. Since these amounts are collected within a year, they are current.

-

Prepaid expenses: These are payments made by a company in advance for services or goods they will benefit from in the next year, making them current. These include items such as rent or insurance.

-

Other liquid assets: These include any other short-term asset that can be converted into cash or benefit a firm in the next year.

What Are The Current Liabilities?

They are the obligations a company owes that are due within one year. These are the balances that the liquid assets need to “cover” and will tell us if WC is sufficient (positive or negative).

Some examples are:

-

Accounts payable are like accounts receivable. Most companies also buy stuff on credit and will pay cash within the next year, making accounts payable a common current liability. These include items the company has been billed for, like supplies.

-

Accrued expenses are costs a firm has incurred but not paid or billed for and are due within a year, making them current. These include expenses like salaries or interest.

-

Deferred revenue is revenue the firm has received for goods or services it has yet to provide or perform. It is a current liability because the company usually has to provide these goods or services within one year.

-

Short-term loans are funds a firm has borrowed and has to pay back within a calendar year, making them a current liability.

-

The current portion of long-term debt is the amount of long-term debt a company will owe in the current year, making it a current liability, much to the name.

Note

It is important to note that not every company will always have all these components. For instance, any service company selling their expertise instead of a physical product will likely not have significant inventory.

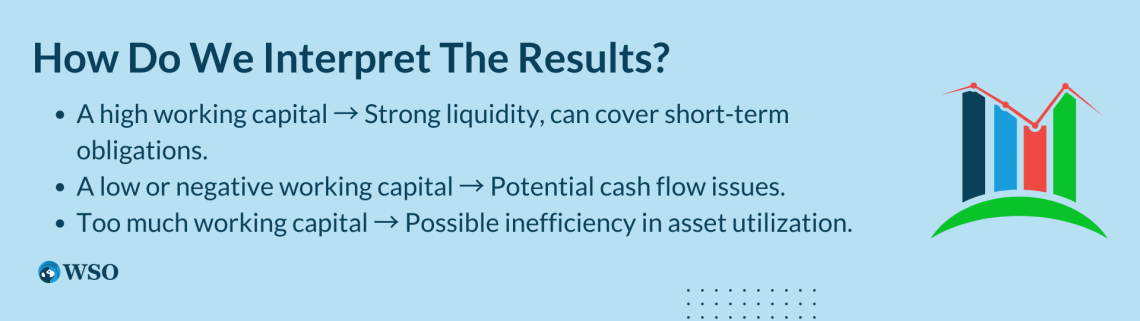

Positive Vs. Negative Working Capital

A positive working capital amount indicates a company's positive liquidity, showing it has enough liquid assets to pay for its upcoming obligations. Any positive amount will show they have enough cash to meet their obligations.

A significantly positive amount isn’t necessarily the best, either. If a company has too high a working capital amount, it could mean it is holding too much cash and not investing it correctly to grow the firm long-term.

Additionally, an overly positive amount could indicate that a firm is not collecting its accounts receivable quickly enough.

Higher working capital is still preferred to lower or even negative levels, but too much should be shied away from. This can be done with the current ratio (discussed at the end of this article), which is the working capital formula expressed as a ratio (current assets / current liabilities).

If the ratio is above 1.0, working capital is positive, and the firm can cover its short-term debts. A ratio above 2.0 indicates a firm has twice as many short-term assets as they do short-term liabilities and may indicate it is not optimally investing its assets.

This means that a moderate positive working capital is best in most cases and should be managed since it changes from day to day.

| Aspect | Positive Working Capital | Negative Working Capital |

|---|---|---|

| Definition | Current assets > current liabilities. | Current liabilities > current assets. |

| Liquidity | High; easy to meet obligations. | Low; potential liquidity issues. |

| Cash Flow | Flexible for growth and emergencies. | Tight; depends on efficient management. |

| Industries | Retail, manufacturing, services. | FMCG, e-commerce, grocery chains. |

| Perception | Indicates financial stability. | May signal risk or efficiency. |

| Example | Retailer maintaining inventory for demand. | Grocery chain collecting upfront from customers. |

A negative working capital indicates poor liquidity, as a firm will not have enough short-term assets to meet its liquidity requirements. This is a problem for the short-term financial health of a company, as long-term assets cannot be used.

To fix this situation, a company may have to issue short-term debt to meet liquidity requirements.

When Negative Working Capital Is Acceptable

Negative working capital could be a general risk to a company’s financial health. It means the firm does not have enough short-term assets to pay its short-term liabilities.

Whether or not it is bad depends on the type of business being run. Companies that sell inventory quickly, such as grocery stores, do not need an extensive inventory supply and may raise the necessary cash in a short period. Therefore, it is a less significant issue.

A temporary negative working capital is not necessarily bad; a prolonged negative net working capital could be bad.

Suppose a company also purchases materials with credit, and the goods are sold before payment to the supplier is due. In that case, the negative working capital will turn positive before the payment is due.

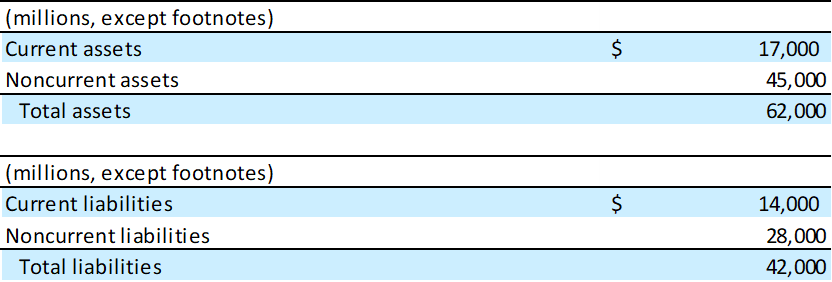

Example calculation with the working capital formula

Below is another set of financial information about Buy Corp. This company has current assets of 17,000 million, current liabilities of 14,000, non-current assets of 45,000, and noncurrent liabilities of 28,000. We will demonstrate the working capital equation with this example.

When calculating working capital with the above example, it is essential to remember the working capital formula only requires current assets and current liabilities.

Therefore, since current assets are 17,000 million and current liabilities are 28,000 million, working capital will equal 3,000 million (17,000 million - 14,000 million).

It is essential not to make the mistake of taking total assets and subtracting total liabilities (62,000 million total assets - 42,000 million total liabilities), as this number in 20,000 million is not the working capital of a company; this is the amount of shareholder’s equity on the balance sheet.

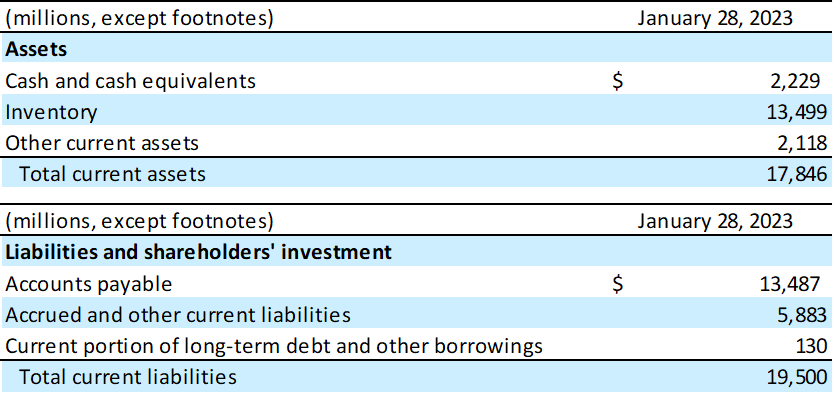

Working Capital Formula with Target’s balance sheet

Below is Target’s (NYSE: TGT) balance sheet. The boxed sections are the relevant sections for the calculation of working capital. We can see the various line items in each box and how they contribute to total current assets and total current liabilities.

Here, we zoom in on the boxed areas to calculate the working capital formula. We see their current assets are cash and cash equivalents, inventory, and other current assets.

Their current liabilities are accounts payable, accrued and other current liabilities, and the current portion of long-term debt.

To find Target’s working capital:

Current Assets = (Cash and cash equivalents + Inventory + Other current assets)

(2,229 + 13,499 + 2,118) = 17,846

Current Liabilities = (accounts payable + Accrued and other current liabilities + Current portion of long-term debt and other borrowings)

= 13,487 + 5,883 + 130 = 19,500

Working Capital = Current assets - Current Liabilities

= 17,846 - 19,500 = -1,654

Therefore, Target has a negative working capital of -1,654 million.

Other Working Capital Formula Forms

Beyond the simple formula we have looked at above, there are other formulas that deal with working capital and tell us about a company’s short-term financial health. The SEC also outlines a few of these here.

Current ratio (aka working capital ratio)

This is another version of the working capital formula in which current assets are divided by current liability instead of subtraction.

Current ratio = Current Assets/ Current Liabilities

The intuition is the same, except a ratio above 1.0 is like a positive working capital formula, as we have been discussing, and a current ratio below 1.0 is similar to a negative working capital formula.

When the ratio is greater than one, it implies that the company is more liquid because it has more short-term assets than short-term liabilities and can cover all short-term obligations with these assets.

A ratio of less than one implies insufficient short-term assets to cover short-term debt liabilities.

Working Capital excluding cash

The working capital formula can exclude cash to return the formula with only the cash content, yielding a formula that doesn’t include the implications of cash.

Working capital excluding cash = (current assets - cash) - current liabilities

This tells more about a company’s operational efficiency when only considering its non-cash, short-term assets, not just its long.

It helps businesses know more about their operational efficiency when relying on something other than cash.

Quick ratio (acid test)

The quick ratio is another measure that can tell a firm how much liquidity they have on their most liquid assets.

Quick Ratio = (Cash + Marketable Securities + Accounts Receivable)/ Current Liabilities

This equation ignores inventory since some companies may need help to liquidate their inventory.

This way, a firm can tell how easily they can cover their current liabilities when only considering their most easily liquidatable or most current assets.

Conclusion

In conclusion, the working capital formula is a simple subtraction formula calculated as current assets minus current liabilities.

The answer measures a company's efficiency and short-term financial health and shows us the company's ability to cover its short-term liabilities with its short-term assets, which will differ depending on the company's strategy and its industry.

If the company has a positive working capital, it is a good sign for its financial health, as a negative amount indicates a company will have difficulty paying down its debt soon. It helps us see how well a company is doing right now and in the near future.

Working Capital Formula FAQs

Current Assets and Current Liabilities. Both are found on the balance sheet and are often labeled as “total current assets” and “total current liabilities.”

Any asset or liability not expected to be used within the coming year. Total assets and total liabilities are not used in the formula; they are only current.

When a company’s working capital is positive, it is sufficient to cover current debts.

Businesses need resources and capital to function day-to-day. Without assets that provide benefits in the short term or liabilities that allow the company to fund projects, businesses could not operate every day.

Size of a firm, industry, nature of the business, the economy, credit, government regulations, and more.

Anything above 1.0 means a firm can pay off its short-term debts, but 1.5 - 2.0 is a good target. Anything above 2.0 could be considered excessive.

Free Resources :

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?