Non-Operating Income

Refers to the part of an organization's revenue that comes from activities outside of its primary business operations.

What is Non-Operating Income?

Non-operating income (NOI) is the part of an organization's revenue that comes from activities outside its primary business operations.

It might include things such as dividend income, investment earnings or losses, foreign exchange gains or losses, and asset write-downs. Non-operating revenue is also known as incidental or marginal income.

Non-operating revenue is the part of an organization's revenue that comes from activities outside its primary business operations. It might include dividend income, investment earnings or losses, foreign exchange gains or losses, and asset write-downs.

Separating non-operating revenue from operating income provides investors with a clearer sense of a company's efficiency in converting money into profit.

Earnings are likely the most scrutinized statistic in a firm's financial records since they demonstrate profitability when compared to analyst predictions and management guidance.

The issue is that earnings in an accounting period might be affected by factors that have little to do with the organization's day-to-day operations.

For instance, a firm might make a sizable one-time profit through the sale of a sizable piece of land, equipment, or property, a wholly-owned subsidiary, or investment securities.

These sorts of gains, together with revenue gained from recurrent occurrences outside of the company's primary line of business, can drastically alter a company's

results and make it difficult for investors to assess how effectively the firm's operations truly performed during the reported period.

-

Non-operating income (NOI) comprises revenue from activities outside a company's primary operations, like dividends, investment gains or losses, and asset write-downs.

-

Distinguishing non-operating income from operating income helps investors assess a company's financial efficiency and performance accurately.

-

Non-operating income, also known as indirect income, includes dividends, gains from asset sales, and interest income, providing additional revenue beyond core operations.

-

Separating non-operating income from operating income on financial statements aids stakeholders in understanding revenue sources and making informed investment decisions.

-

Examples of non-operating income encompass dividends, gains from securities sales, rental income, and profits from foreign currency transactions, impacting a company's overall profitability.

Understanding Non-Operating Income

Non-operating income is earnings from activities outside a company's core operations, like investments, asset sales, or subsidiary income. It's non-core revenue.

Non-operating revenue is income that is not directly tied to the organization's business; hence, it is also known as indirect income. It is included in profit calculations even if it is not directly tied to the business and is obtained by surplus investment from the firm.

Separating non-operating from operating income provides stakeholders and users of financial statements with a clear image and better knowledge on which to base investment decisions.

Non-operating is defined as any profit or loss derived from the organization's operations that are not directly related to the selling of goods or the provision of services.

The nature of non-operating varies depending on the type of revenue, such as income in the form of interest; dividends are repeating in nature, whilst income in the form of foreign exchange gain is non-recurring.

Example of Non-Operating Income

ABC Ltd. generates a profit of $500,000 from its operating activities. The following are the specifics concerning non-operational activities:

| Dividend earnings | $50,000 |

| Income from the Sale of Securities | $45,000 |

| Loss on Foreign Exchange Transactions | $25,000 |

| Interest paid on loan obtained to invest in securities | $12,500 |

| Asset Depreciation | $80,000 |

Determine the organization's overall revenue.

Solution: NOI Calculation

| Particulars | Amount ($) |

| Stock dividends | 50,000 |

| Income from the sale of securities Foreign | 45,000 |

| exchange transaction losses | (25,000) |

| Loan interest on non-operating investments | (12,500) |

| Asset depreciation | (80,000) |

| Total | (22,500) |

Calculation of the Organization's Total Income

| Operating Income | 500,000 |

| Less: Net Non-operating Income | (22,500) |

| Total Income | 477,500.00 |

More examples:

- The buying and selling of goods is the main activity of retail companies, which calls for a significant quantity of cash and liquid assets. A store may decide to invest its idle cash to make it work for it.

- $500 ($10,000 * 0.05) is regarded as non-operating if a retail store invests $10,000 in the stock market and makes 5% in capital gains in one month.

- When analyzing this retail organization, the $500 would be depreciated as earnings because it cannot be depended on as ongoing income in the long run.

- In contrast, the gains are categorized as non-operating if a technology company sells or spins off one of its divisions for $400 million in cash and shares.

- If the technology business generates $1 billion per year, it's easy to understand how the additional $400 million will improve earnings by 40%.

- A dramatic increase in earnings like this makes the firm appear to be appealing to investors.

- However, because the transaction cannot be repeated or duplicated, it cannot be classified as operating income and should be excluded from performance monitoring.

Non-Operating Income vs. Operating Income

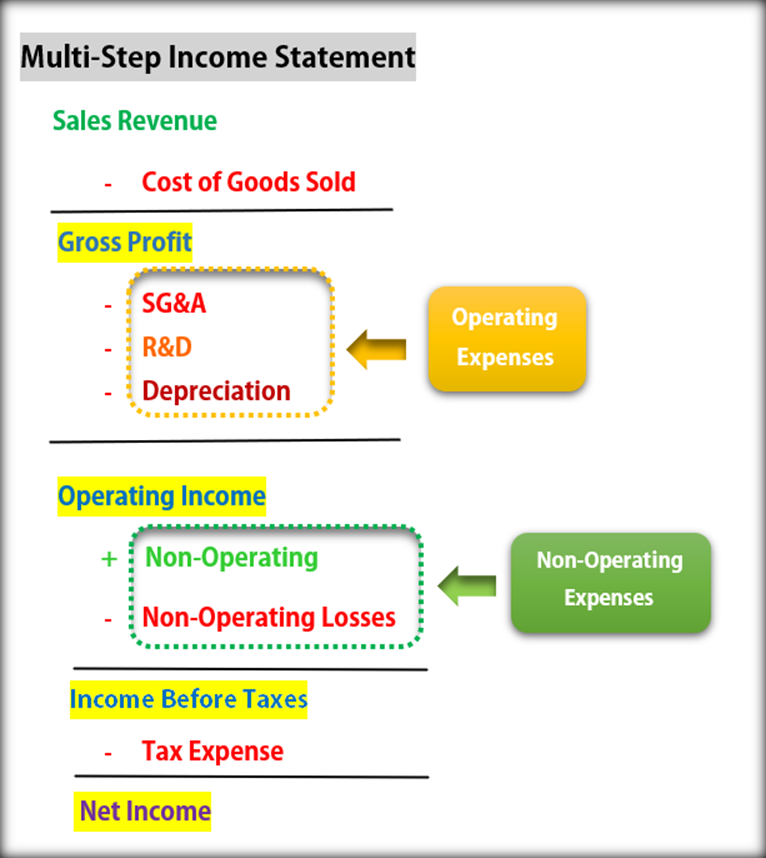

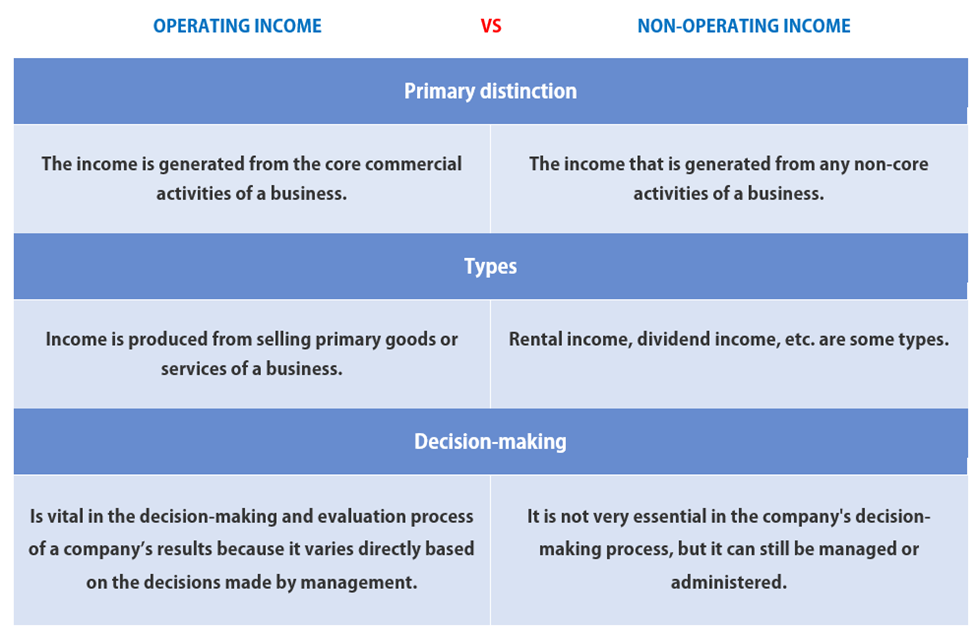

The income of a corporation is divided into two categories: operational and non-operating. Earnings before interest and taxes is another term for operating income (EBIT). It is the revenue earned by the company's primary operations. It demonstrates how well the firm performs in its day-to-day operations.

Gains and losses (expenses) from actions or circumstances unrelated to the company's primary business operations are included in non-operating income. A multi-step income statement identifies a company's operational and NOI, as demonstrated below:

Operating income is computed by deducting the company's sales revenue from the cost of products sold and other operating expenditures. The expenditures incurred to manage the company's fundamental activities are known as operating expenses.

Depreciation, SG&A spending, and R&D expenses are all examples. The company's earnings before taxes may be computed by adding the non-operating to the operating income.

The corporation declares a positive non-operating income if the overall non-operating profits exceed the total non-operating losses. If the company's non-operating losses outnumber its overall gains, it has a negative NOI (loss).

Operating earnings are recurrent and are more likely to increase in tandem with the company's growth. Operating income, as opposed to non-operating, gives more information about the company's fundamentals and growth prospects.

A corporation that performs better in its main business operations and produces the bulk of its revenue is more favorable than one that obtains the majority of its revenue from non-operating activities.

It's critical to distinguish between a company's capacity to profit from its primary business and other activities or aspects when assessing its true success.

A multi-step income statement can reflect a company's financial health more clearly than a single-step income statement, which does not distinguish between operational and non-operating earnings and costs.

It's critical to distinguish between money earned through day-to-day business activities and income created from other sources when evaluating a company's true success.

As a result, companies must report non-operating separately from operational income.

After subtracting operational expenditures such as labor, depreciation, and cost of goods sold, operating income is an accounting statistic that reflects the amount of profit realized from a business's activities (COGS).

It informs interested parties about how much revenue was converted into profit due to the company's routine and continuous business operations. On the income statement, operating income is recorded.

Non-operating should show at the bottom of the income statement, under the operating income line, to enable investors to identify between the two and understand where the revenue comes from.

The following are some examples of non-operating profit and spending items used in the calculation of NOI:

- Other entities' dividend income

- Interest in other entities' investments

- Rental revenue from a building, hall, or other location

- Profit from the sale of a fixed asset

- Gain on the sale of an investment in another company's debt or equity securities

- Gain accrued as a result of foreign currency transactions.

- Profit or loss on the sale of a fixed asset

- Loss on the sale of investments in other firms' debt or equity securities

- Loss incurred as a result of foreign currency transactions.

The computation of NOI may be expressed as follows in equation form:

Non-operating income = All non-operating revenues or benefits – all non-operating costs or losses

The following is an equation that may be used to calculate operating income:

Operating income = Total revenue from operations - the cost of goods sold - operating expenditures

Non-Operating Activities vs. Operating Activities

Operating activities include everything a firm regularly does to bring its products and services to market.

Non-operating activities are one-time occurrences that may have an impact on sales, costs, or cash flow but are not part of the company's regular core activity.

Operating activities:

- Developing a strategy

- Work organization

- Producing (or obtaining) goods and services

- Its products and services are marketed and sold.

- Day-to-day administration

Non-Operating activities:

- Relocating the company

- Expenses incurred as a result of weather damage

- Purchasing another company

- Purchasing or disposing of capital assets

- Taking out or repaying a debt

- Issuing new stock

While operating activities are commonplace and non-operating activities are unusual, they are disclosed separately in a company's financial statements and financial analysis.

Operating activity reporting clarifies the business's focus and earning potential, with two essential measurements being cash flow from operating activities and cash flow changes over time.

Non-operating activities are shown in the computation of net income for tax reasons but not in any evaluation of a company's regular financial performance.

More about operating and non-operating activities

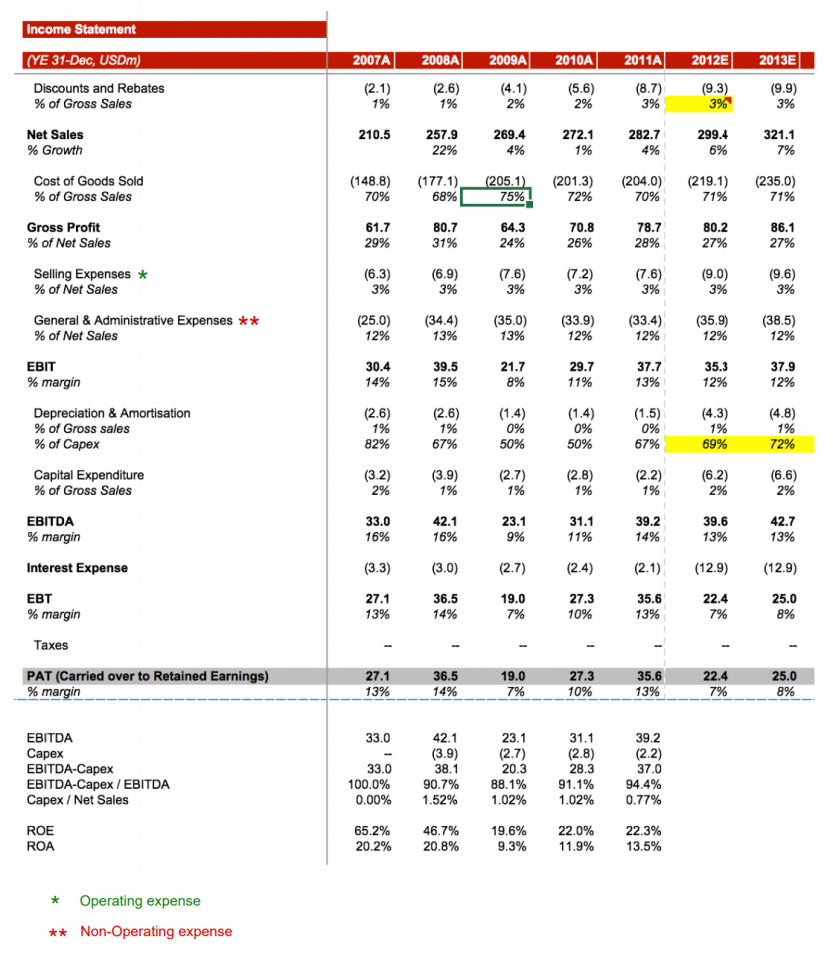

The template income statement here explains how to account for operating and non-operating activities.

Pros and cons of non-operating income

Some of the pros and cons are:

Pros:

- Non-operating recurrent revenue is considered a safe income since it is the least the organization may generate.

- Losses from a business can be offset against non-operating revenue, lowering the net loss.

- Non-operating revenue contributes to the organization's profitability as well as profit sharing.

- Most non-operating losses are one-time events, whereas non-operating profits are ongoing.

Cons:

- Non-operating earnings might raise the organization's tax burden.

- If NOI is negative, it might lower the organization's net income, impacting its performance.

- Non-operating income or losses are unrelated to the organization's primary business activity, although they do contribute to its profit or loss.

- A higher NOI implies flaws in the company's operations.

- When NOI exceeds operating income, it casts doubt on the organization's operations and activities, and investors may lose interest in investing.

Non-operating income includes but is not limited to, dividend income, gain or loss on foreign currency transactions, asset impairment loss, interest income, and other non-operating revenue streams.

It can be both beneficial and negative. If non-operating income is positive, it contributes to profit and allows for additional profits to be reported in the income statement.

However, if non-operating income is negative, it reduces profit and has the opposite impact on the company. Non-operating income is included in earnings even if it is not part of the primary operation.

When non-operating revenue exceeds operating income, it raises questions about the organization's operations, purpose, and activities. Non-operating revenue is beneficial to the organization, but it should be limited and smaller than operating income to retain the company's market reputation.

When a company's operating profit is low, it may try to hide it with significant non-operating income. Be wary of management teams who strive to identify measures that include overstated, independent gains.

Earnings before interest and taxes (EBIT), for example, comprises money from non-core company operations and is frequently used by firms to hide poor operational outcomes. Non-operating income is frequently the reason for a large increase in earnings from one quarter to the next.

Attempt to determine where money was created and how much of it, if any, is related to the company's day-to-day operations and is likely to be repeated. Operating revenue can assist, but that isn't always the case.

Unfortunately, experienced accountants occasionally find ways to disguise non-operating transactions as operating income to boost income statements’ profitability.

Researched & Authored by Fatemah Kamali

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?