Fisher Effect

A theory that explains the relationship between inflation expectations, real interest rates, and nominal interest rates.

What is the Fisher Effect?

The Fisher Effect is an economic theory introduced by the American economist Irving Fisher in 1930. It explains the relationship between inflation expectations, real interest rates, and nominal interest rates.

It states that the real interest rate is equal to that of the nominal interest rate minus the expected inflation rate. Therefore, inflation increases as the real interest rates fall unless there is an increase in the nominal interest rates at the same rate as inflation.

r = i - πe

Where;

- r = real interest rate

- i = nominal interest rate

- πe = expected inflation rate

The equation is an approximation; however, the difference is small with the correct value as long as the rate of inflation and rate of interest is low. The discrepancy becomes large if either the rate of interest or the nominal interest rate becomes high.

There is one implication of this effect: nominal interest rates tend to mirror inflation while making the monetary policies neutral. This is an important relationship in the field of macroeconomics.

- The Fisher Effect is an economic theory proposed by economist Irving Fisher, which describes the relationship between inflation and both real and nominal interest rates.

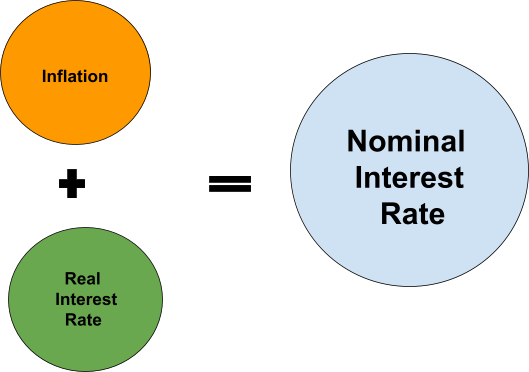

- It asserts that the nominal interest rate is equal to the sum of the real interest rate and the expected inflation rate.

- The Fisher Effect implies that changes in expected inflation will be fully reflected in changes in the nominal interest rate, leaving the real interest rate unchanged in the long run.

- Investors and policymakers use the Fisher Effect to separate the impact of inflation from the real return on investments. Understanding the expected rate of inflation helps them make better decisions about interest rates and investment returns.

Nominal Interest Rates and Real Interest Rates

The casual relationship between the nominal interest rate and inflation is described in the equation relationship.

An increase in nominal rates tends to decrease inflation. The key assumption is that either the real interest rate stays constant or changes by a small amount.

When the real interest rate is positive, it means a lender or an investor avoids inflation. When the real interest rate is negative, it means that the rate that is charged on a loan or paid on a savings account is unable to avoid inflation.

This effect has been extended to help with the analysis of the money supply and international trading of currency.

This effect is visible every time we go to the bank; the nominal interest rate is the interest rate that an investor has on a savings account.

Let us take an example on a savings account, if the nominal interest rate is 5% and the expected rate of inflation is 4%, then for real, the money in the savings account is growing at a rate of 1%.

The smaller the real interest rate, the longer time it takes for the savings deposits to grow substantially when it is observed from a purchasing power perspective.

The financial return that an individual gets when they deposit money is reflected through the nominal interest rates. Let us take an example, a nominal interest rate of 20% per year means that an individual will receive an extra 10% of the money deposited in the bank.

What Is A Fisher Equation?

The Fisher Equation is a concept in macroeconomics that defines the relationship between nominal interest rates and real interest rates under the effect of inflation.

According to the equation, the nominal interest rate is equal to that of the sum of the real interest rate plus inflation.

The equation is often used in situations where an additional reward is asked from the investors or lenders to compensate for losses in the purchasing power due to the high rate of inflation.

This concept is widely used in the field of economics and finance. It is frequently used to calculate the returns on investments or to predict the behavior of nominal interest rates and real interest rates.

For example, when an investor wants to determine the real interest rate that is earned on an investment after it is accounted for the effect of inflation.

The Fisher equation is expressed through the following formula:

(1 + i) = (1 + r) (1 + πe)

Where;

- r = real interest rate

- i = nominal interest rate

- πe = rate of inflation

If the real interest rate ( r ) is assumed to be constant, the nominal interest rate ( i ) changes when the 𝛑e rises or falls. Thus, the Fisher Effect states that there will be a one-for-one investment of the nominal interest rate to the expected inflation rate.

The constant real interest rate implies that monetary events such as monetary policy actions have no real effect on the real economy - there is no effect on real spending by consumers on durables and by businesses on equipment and pieces of machinery.

However, an approximate version of the previous formula can also be used:

I ≅ r + π

Another interesting finding in the Fisher Equation is related to monetary policies. This equation reveals that inflation and the nominal interest rates are moved together in the same direction by monetary policy. Whereas the real interest rate is generally not affected by the monetary policy.

Fisher Effect Applications

This concept is widely used in the field of economics and finance. It is frequently used to calculate the returns on investments or predict the behavior of nominal and real interest rates.

The applications of the Fisher Effect are mentioned below:

Monetary Policy

The central bank in an economy is often in charge of keeping inflation in a tight range. It is the practice to prevent the economy from overheating and the upward spiraling of inflation in times of expansion.

It is also very important to have a small amount of inflation to prevent a deflation spiral, finally pushing an economy into a depression during times of recession.

The central banks have the main tool, and they can set the nominal interest rates. The central banks achieve this through many mechanisms like changing reserve ratios, open market operations, etc.

When there is a given fixed interest rate, we observe that there is an increase in the nominal interest rate, which will bring down inflation expectations and prevent overheating.

Similarly, when there is a decrease in the nominal interest rate, it can increase inflation expectations and provide more investment, thereby avoiding a deflation spiral.

Measuring Portfolio Returns

A major objective of investing is in order to generate more returns to outpace inflation. It is very necessary because if the returns are lower than the inflation, then the purchasing power of the total wealth of the investor will be lower than their investing rate.

Let us take an example, an investment in the country is generally considered risk-free and offers a yield of 2% over one year. Let us assume that the inflation in a country is 3% per year, and a business is needed to purchase goods worth 100$ today.

Their cash is invested in government debt, which means they get $102 in a year. The goods are now worth $103 as the rate of inflation was 3%. Hence, when the business needs to make a purchase, there is a shortfall of 1%.

The example given above shows an important point that liquidity issues can be created in the future by ignoring the impact of inflation. This effect is important as it helps investors to calculate the real rate of return on their investments.

It can also be used to determine the required nominal rate of return, thereby helping the investor to achieve their goals.

Markets of Currency

In the markets of currency, this effect is called the International Fisher Effect (IFE). It defines the relationship between the nominal interest rates of two countries and the rate of spot exchange for their currencies.

Hence, the future spot rate can be calculated by the given nominal interest rates in the two countries and the spot exchange rate.

The formula to calculate the future spot rate is:

Futures Price = Spot Price (1 + rD) / (1 + rF)

Where:

- rD = Nominal Interest Rate in the Domestic Currency

- rF = Nominal Interest Rate in the Foreign Country

It is evident from the equation that if the foreign rate is higher than that of the domestic rate, then the domestic rate is expected to be depreciated relative to that of the foreign currency. It is known as the International Fisher Effect (IFE).

The International Fisher Effect (IFE)

The International Fisher Effect (IFE) is an economic theory that states that the expected disparity between the exchange rate of the two currencies is approximately equal to the difference between the two countries' nominal interest rates.

According to this theory, countries with higher nominal interest rates experience high rates of inflation, which results in the currency's depreciation against the other currencies.

This theory is based on the analysis of interest rates that are associated with present and future risk-free investments, such as treasuries, and it is used to help in the prediction of currency movements.

It is in contrast to other methods that only use inflation rates to predict the exchange rate shifts, that is, instead of functioning as a combined view relating to the interest rates and inflation to a currency’s appreciation or depreciation.

It stems from the concept that real interest rates are independent of other monetary variables, such as changes in a nation’s monetary policies, and it provides a better prediction of the health of a particular currency within a global market.

It provides the assumption that the countries with lower interest rates will also experience lower levels of inflation, finally resulting in an increase in the real value of currency associated when compared to the other nations.

The nations with higher interest rates are more likely to experience depreciation in the value of their currency.

It is calculated as:

E = (i1 - i2)/(1 + i2) ≈ i1 - i2

Where;

- E = the percent change in the exchange rate

- i1 = Country A’s interest rate

- i2 = Country B’s interest rate

The Fisher Effect and the IFE are related to each other but are not interchangeable. The Fisher Effect claims that the combination of the real rate of interest and the expected rate of inflation is represented in the nominal interest rates.

The IFE is expanded on the grounds of the Fisher Effect while suggesting that the nominal interest rates reflect the rates of inflation that drive the expected inflation rates and the currency exchange change rates.

There are mixed results regarding the IFE, and it shows that other factors also influence movements in currency exchange rates.

Historically speaking, when significant magnitudes more adjusted interest rates, then there was more validity of the IFE.

Evidence Of The Fisher Effect

After everything that is discussed above, this effect is the most important policymaking in the economy as it is applied to monetary policies. There are many studies performed by economists in order to prove the existence of the Fisher Effect and how to measure it.

The different shreds of evidence by the economists are mentioned below:

Mishkin 1991, 1995

Fredrick Mishkin of Princeton University wrote a paper and found that this particular effect exists for the long term, but in the short term, the paper has not yet found any relationship between inflation and nominal interest rate.

Another paper from Fredrick Mishkin conducts an empirical analysis of this effect in Australia, but in vain, he again found the same conclusion.

Jaffe and Mandelker, 1976

Jaffe and Mandelker studied the relationship between inflation and returns on risky assets. To be precise, they studied the relationship between returns from stock markets and inflation.

Most studies about this effect study the relationship between the risk-free rate (or nominal interest rate) and inflation. There was no existence of this effect in the stock market returns from their study.

It is found that increased inflation is negatively correlated with market returns. The findings run counter to the relationship as described by the Fisher Effect.

Uribe, 2018

This is one of the most recent investigations, and accordingly, it holds for the temporary changes in the nominal interest rate. But when there is a permanent increase in the nominal interest rate, the opposite is true, and inflation occurs due to an increase in the nominal interest rate.

The facts mentioned above are entirely opposite of the mechanism in the monetary policy section. The author calls this mechanism the Neo-Fisher Effect.

It is entirely a new theoretical framework in response to the unconventional monetary policy that has been used since the Great Financial Crisis (GFC) of 2008.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?