Minsky Moment

The onset of a market collapse is followed by reckless speculative activity involving high debt amounts taken by investors.

What is a Minsky Moment?

The Minsky Moment is the onset of a market collapse which is followed by reckless speculative activity involving high debt amounts taken by the investors. This term is frequently used to discuss past or future financial crises.

It is named after an American economist, Hyman Minsky, who defined it as the time when there was a sudden decline in the market that inevitably led to a market collapse that eventually led to a larger economic crisis.

This crisis generally occurs when investors take part in excessively aggressive speculative activity and increase credit risk during a prosperous time in the market.

According to Hyman Minsky, markets are completely unstable and oscillate between stable and unstable periods.

It is the peak point when speculative activities reach an unsustainable extreme, leading to an unpreventable market collapse and rapid price deflation.

According to the hypothesis, rapid instability occurs because extended periods of steady investment gains and prosperity encourage a diminished perception of market risk, which promotes the risk of investing borrowed money instead of cash.

The repetitive chain of Minsky moments is the general concept of a “Minsky Cycle”.

Hyman Minsky, an economist, argues that markets (particularly bull markets) have the general characteristic of being unstable. The term " bull market” denotes a period during which the market experiences a sudden increase.

It refers to a moment of time when there is a sudden increase in a major crisis of asset values, resulting in an increase in debt.

It is based on the idea that if the period of bullish speculation extends, then it will gradually result in a crisis, and the longer this period extends, the worse the crisis.

An accurate example of this moment is the financial crisis of the year 2008. At the peak of this financial crisis, a substantial number of markets assumed they were at their all-time lows, eventually leading to the selling of assets to cover market debts and higher default rates.

- A Minsky Moment is a sudden market collapse that follows an extended period of bullish activity driven by unsustainable speculation and debt.

- Minsky's hypothesis states that periods of economic stability and rising asset prices lead to increased risk-taking and borrowing, eventually resulting in a sharp market correction or financial crisis.

- A Minsky Moment is triggered when borrowers can no longer meet their debt obligations, leading to a cascade of asset sales, plummeting prices, and widespread panic.

- During a Minsky Moment, the rapid unwinding of speculative positions and forced asset sales can lead to significant declines in market value, increased volatility, and a loss of confidence among investors.

Understanding Minsky Moment

A Minsky Moment is based on the idea that if these periods of bullish speculation last for a long time, this will eventually lead to an economic crisis, and the longer this period of bullish speculation occurs, the more severe this crisis will be.

Hyman Minsky’s main theory of this economic theory was centered around the concept of market instability, especially in bull markets. He felt that long periods of bull markets ended in cataclysmic crashes.

According to Hyman, an abnormally long period of bullish economic growth causes an unprecedented asymmetric rise in market speculation, eventually leading to a market crisis and instability.

It is also associated with high amounts of debt taken on by both institutional and retail investors, followed by prolonged periods of bullish speculation.

The term “Minsky Moment” was coined by Paul McCulley in 1998 to describe the Afghan Crisis of 1997. This crisis was caused due to the pressure on dollar-pegged Asian currencies by others, which eventually caused the fall of the same currencies.

Retail and institutional investors may decide to take more credit during this promising market period after increasing, which leads to a sudden change in market value, eventually leading to the fall of the market. Therefore, it is called the Minsky Moment.

When the markets are good and profitable for a long period of time, investors keep on borrowing money and adding risk to their portfolios. They continue to take on risks, speculating that the prices will continue to increase.

However, when asset prices stop rising, the investors will have borrowed so much money that they will have no cash left to pay off their debts.

When the lenders call in for their loan repayment, the investors have to start selling their assets to repay the loans. However, this can immediately trigger a collapse in the prices, and the market witnesses the above-mentioned moment.

Hyman Minsky's Financial Instability Hypothesis

According to an assumption based on underlying classical economic theory, the economy seeks equilibrium and is fundamentally stable.

The theory suggests that when there is an excess, the rational market sees it and finds a way to either make money or lose it, thereby moving the economy back to equilibrium.

According to this theory, diseases, wars, and technological advances are external shocks to the economy. These are the bubbles that can cause potential crashes in the economy.

Hyman Minsky proposed a theory labeled the "financial instability hypothesis" that holds that the economy will create its own bubbles and crashes.

The gist of his theory is that a stable economy sows its own seeds of destruction because stability leads people to take risks. This risk-taking nature creates financial instability, eventually resulting in crisis and panic.

Unfortunately, neither Minsky nor his theory were taken seriously during his lifetime. He died in 1996, before the Great Recession and the dot-com bubble, both of which validated his theory. His theory is now accepted as the primary explanation for the boom-and-bust cycles in the economy.

This theory is rooted in the excessive risk-taking and the panic that follows when this risk-taking fails, and the economy collapses. Increased risk-taking causes an increase in debt.

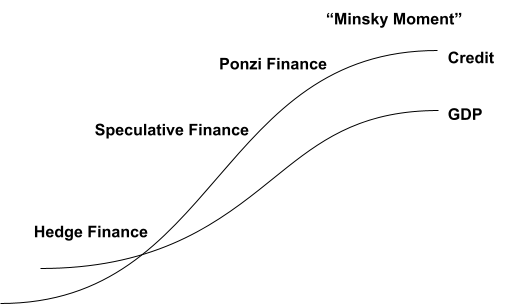

There are three stages that led to this moment: the hedge phase, the speculative phase, and the Ponzi phase.

The key insight is that stability in itself is destabilizing because, during times of economic stability, healthy investments lead to euphoria, overextended debt, and increased financial leverage, eventually causing a Minsky Moment that leads to recession or even a financial crisis.

Phases leading to A Minsky moment

Hyman Minsky’s Financial Instability Hypothesis postulated that there are three phases that lead to a Minsky Moment. These are three credit lending stages, with risk levels increasing in each subsequent stage that finally ends with a market collapse or bubble burst.

The three credit lending phases are explained below:

Hedge Phase

It is the first phase of the Minsky Theory. It is the most stable phase of total debt in the economy. The market is characterized by strict credit policies and high lending standards, along with memories of recent collapses.

Borrowers can use cash flow from investments to meet the principal and interest expenses.

Hedge Financing Units can fulfill all the payment obligations with their cash flow: the greater the weight of equity financing, the greater the possibility of it being a hedge financing unit.

Hedge units are typically governments with floating debts, banks, or corporations with floating issues of commercial paper.

Speculative Borrowing Phase

This phase follows the hedge phase. In the speculative borrowing phase, cash flow from the investments can be used to cover only the borrower’s interest payments, not the principal.

The level of debt increases while profit rises, the economy starts rising, and the credit guidelines are loosened.

According to the investors, the investment values will continue to rise, but the interest rates will not. Borrowers meet their interest expenses, but the repayment of the principal will be stressful from the investment income.

Speculative finance units are able to meet their payment commitments even if they cannot repay the principal out of cash flow. Such units need to roll over their liabilities.

Ponzi Phase

This is the phase before the bubble bursts or the market collapses and is the riskiest phase in the cycle. The cash flow from the investments is not enough to cover the principal payments and interest.

This phase exhibits optimistic people making irrational decisions and taking risky decisions. Investors believe that the value of assets will rise to allow them to sell the assets at higher prices, enabling them to pay off their debts. Therefore, they borrow money.

This phase is characterized by high debt, high risk-taking activities, high asset values, and an increase in the sale of assets. Still, the borrowers find it difficult to pay off their interest expenses and principal.

Finally, these events led to the collapse of the market and subsequent recession.

Catalysts and Effects of a Minsky Moment

It generally occurs when investors engage in excessively aggressive speculation and take on excess credit risk during prosperous times or bull markets. Investors borrow to capitalize on market sentiments.

The longer a bull market extends, the more debt is taken on by the investors, and hence, there is more risk. This decreases the prices of assets from speculation, finally resulting in margin calls and credits being unpaid, affecting borrowing rates across the market.

The Minsky Moment defines the peak point at which speculative activities reach an extreme, leading to the rapid decline in prices and the unpreventable collapse of the market. This is followed by an extended period of instability.

Cash is generated by the assets acquired by investors, which are used to pay off the debt that was taken to acquire them. A point arrives when there is not enough cash to compensate for the debt due to the decreased value of assets under leverage.

It happens due to a slight retracement of the market, which is normal behavior, eventually resulting in the decreased values of leveraged assets.

As a result, debt collectors begin to make calls about loan repayments. It is already difficult to sell speculative assets, so investors are required to sell fewer speculative assets.

This creates a market spiral, a sharp decline in liquidity, and increased cash demand in the market that might require central banks to intervene.

The inevitable collapse of the market is caused by the rapid decrease in credit volume. The market then follows a long period of market instability.

For example, an investor borrows funds to invest when the market is in a prosperous time or a bull market. But when the market comes down for a bit, the leveraged assets might not be able to pay off the debts.

When lenders begin to demand debt repayment, investors will be forced to sell off less speculative assets in order to repay the loans. The sale of these assets causes the market to decrease.

How Minsky Moment can Help us be Better Investors

Hyman Minsky’s financial instability hypothesis is an essential model for all of us to have in our toolkits. This hypothesis has three cycles, and they each have their own characteristics, lengths, and risks.

The state of euphoria and panic lasts longer than we expect it to end. Outside shocks such as pandemics, earthquakes, geopolitical events, and any other natural or man-made disaster can also have big effects.

It is impossible to predict precisely when the economy will transition from one part of the cycle to another or how long each cycle will last.

If we have a rough estimate of our position in the cycle, then investors and business owners can come up with good strategies.

As the markets and economy move from a state of boom to euphoria, it's very essential to have a healthy margin of safety in the form of cash and high-quality bonds.

Smart businesses increase their cash to shore up their liquidity and they resist the temptation of taking up debts too.

Then, when the stage of panic and profit-taking occurs, the smart business owners can redeploy their safety margins (cash or high-quality bonds) into bargain-priced risk assets.

The financial instability hypothesis by Hyman Minsky is full of lessons, but the most essential one to remember is to avoid being caught up in the dread of the panic phase of the cycle or the greed of the euphoric phase of the cycle.

However, it is impossible to foresee the transition phase of the cycle or to precisely time market tops and bottoms.

However, recognizing where we are in the cycle may help us stick to a better investment strategy and avoid following the others full speed into a bust.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?