Pecking Order Theory

Businesses' approach to fund investment opportunities

What is the Pecking Order Theory?

The pecking order theory relates to the source of funding a business decides to use to fund investment opportunities. When businesses want to expand, they do so in a myriad of ways- they could invest in research & development, take on new projects, hire more staff, etc.

However, to accomplish that, they are going to require funding. The pecking order theory thus explains the systematic approach businesses will follow when deciding which source of funding to obtain.

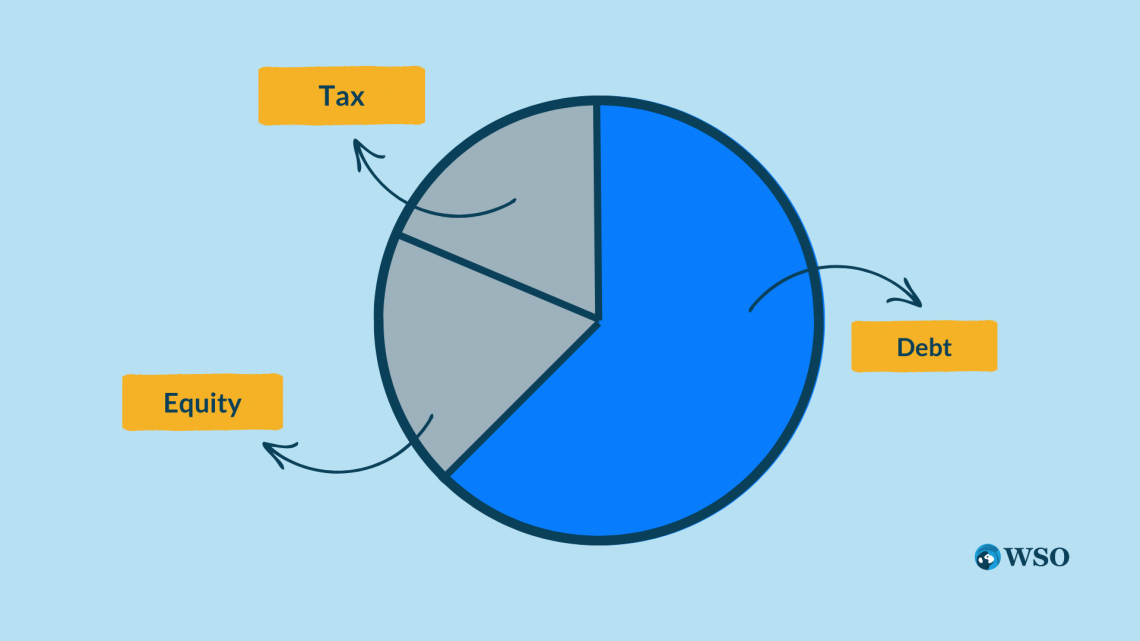

When businesses do seek funding, there are essentially three ways to fund their projects:

-

Finance internally using retained earnings

-

Debt financing by issuing fixed income or getting loans from creditors or lenders

-

Equity financing by issuing shares, relying on the primary/secondary markets

All three methods of raising capital are distinctly different. It is important for those working in corporate development to decide on which source to rely on because it will significantly impact the firm’s capital structure.

Why does a firm’s capital structure matter in the first place? Simply put, the main objective of a firm’s management is to maximize shareholder value.

To accomplish that objective, management ideally wants the highest market capitalization for their business and also the lowest cost of capital possible - both of which are connected to the capital structure of the firm (more on this later).

Following the theory of pecking order in capital structure, when deciding which source of funding to undertake, firms will prefer to do so by seeking the least costly options first.

What is the order? Broadly speaking, it would be to seek internal financing where possible, then move on to the debt. When issuing debt is no longer prudent, only then will firms seek equity funding.

- Pecking order theory describes how companies prioritize funding sources - internal funds first, then debt, then equity as a last resort.

- Equity financing is seen as the most costly due to signaling effects that can lower share prices.

- Debt is preferred over equity where prudent due to tax benefits and lower risk/cost for debt holders.

- High leverage strains cash flows so companies limit debt to optimal levels based on circumstances.

- Firms aim to maximize shareholder value so pecking order aligns with accessing lowest cost financing first.

Understanding The Pecking Order Theory

Why would firms prefer internal financing over debt over equity? The main reason is that issuing equity is more costly to the firm than its alternatives (more on this later).

If you ever follow markets, then you can see that share prices almost always fall following a company’s announcement of additional equity offerings.

Traditional neoclassical economics has always (among others) believed in two things: perfect knowledge and rationality. While both assumptions are unrealistic, let’s relax on the less believable assumption - perfect knowledge.

Realistically speaking, although there is widely available information accessible to investors, the ones who know the most about a company are likely to be the upper management and seniors of the company.

It would be reasonable to assume that the firm's decision-makers are intelligent and rational people (if not, they wouldn’t be running the company).

So let’s say that a firm is about to take on a project that requires additional funding. Let’s look at the option of raising capital via equity from both the CFOs and the investors' perspectives, starting with the CFOs.

CFO: “I ONLY want to issue equity if it is overpriced. My stock is currently trading at $3, but I believe it is worth $4. If we were to issue equity, why would I give away a free 25% to new investors?

That would not be fair to my current shareholders, and from a business perspective, it would be stupid to give away free money. However, I would issue shares if I thought my stock was worth $2. At least that way, my shareholders can profit off this equity-raising exercise.”

Investors: “As much as I research this company, I really can’t know everything about it. However, I am sure that its management knows much more about the company than I do.

The company decided to issue additional shares. Wouldn’t they only do that if they think their share price is overpriced? Their equity must be overvalued! I better sell my stake before the market realizes this.”

The above is a classic example of signaling theory. Rational individuals who observe the actions of other rational individuals can make inferences from those actions.

The general message management conveys to investors when they issue equity is that management thinks their equity value is overpriced purely because it wouldn’t be smart to issue stock if it was underpriced.

So from an investor's perspective, why would they want to hold/buy that company’s stock if even their own management doesn’t have faith in it?

Whether the company’s equity is overvalued following management’s decision to issue equity or not, investors are forced to draw that conclusion because of information asymmetry.

Investors cannot possibly know the full picture and the right action would be to only issue equity if it is overvalued.

In fact, a company issuing debt will signal to investors that they are confident in meeting its debt obligations and that they have a strong cash flow. A company relying on retained earnings signals that they are flushed with cash and would not even need to incur any debt expenses.

Debt vs. equity in capital structure

When a business operates, you can think of its profits being financed by two key stakeholders: debt holders & shareholders.

A company’s capital structure is often expressed as a debt-to-equity ratio. If their debt-to-equity ratio is 4, then for every $100 invested, $80 came from debt, and $20 came from equity.

Understanding the difference between debt and equity is important to gauge its impact on a firm’s capital structure (and maybe why it is preferred over equity where possible). First, assuming the firm is not insolvent, debt holders will always get paid.

Whatever way the debt is structured, firms must meet those interest expenses and principal repayments. In contrast to debt, equity holders are guaranteed nothing.

The return shareholders get will depend on the management and how much they’d like to pay out in the form of dividends.

Because debt holders are theoretically guaranteed money, their returns are often considered less risky and lower than the expected return for equity holders.

Debt and Cost of Capital

Because debt is less risky compared to equity, a company that increasingly finances itself using debt over equity will reduce a company’s cost of capital. You will realize this when you calculate the firm’s cost of capital.

Knowing that the management of the firm would want to maximize shareholder value, what effect do you think a lower cost of capital would have on a company’s market capitalization?

Suppose you are familiar with the discounted cash flow model in valuing companies. In that case, you’d know that having a lower cost of capital would mean that all future free cash flows will have a greater present value because of a lower discount rate. All of that results in a higher market cap.

Debt and Taxes

This one will definitely be familiar to accounting students. Although a business is financed by both debt holders & shareholders, its profits are also shared with Uncle Sam (the government) in the form of taxes.

However, the stakeholders who get paid follow a structured order. The profit that businesses generate will first be distributed to debt holders in the form of principal repayments & interest expenses.

Then, Uncle Sam reaches his hand out and takes his cut. This would be in the form of taxes, and Uncle Sam’s cut can be calculated as:

(EBIT - Debt Repayments)* (Corporate Tax Rate)

Only after all debt holders and Uncle Sam get paid does the remaining money get distributed to shareholders. This further reinforces why equity is considered riskier than debt. The shareholders are paid last.

You might be wondering why debt holders are paid first. The main reason is that in the eyes of the government, debt is considered an expense, and expenses are tax deductible.

If this is your first time learning about this, then you probably feel that a business would be able to pay less to Uncle Sam if they choose to finance themselves with a higher proportion of debt. That feeling would be right, which is a key reason debt is so beneficial.

The reduction in tax expenses arising from incurring debt is known as tax shields. The name is self-explanatory, and the formula is provided below:

Debt Expenses * Corporate Tax Rate

For example, if a business incurs $900k in debt expenses and the corporate tax rate is 33.33%, then the firm is saving ~$300k in the form of tax shields because the $900k in debt expenses were not taxed.

Although we’ve established here that debt has many significant benefits to a firm, there is a reason why firms are not all debt-financed.

The truth is that debt strains a company’s cash flows and forces it to expend money on debt obligations, while equity does not have the same pressure.

In fact, investors are generally cautious when firms are over-leveraged because it may be a sign of financial distress, and a highly leveraged firm runs a greater risk of insolvency than a firm that does not have that much debt.

Many people argue that the strain on a company’s cash flows due to incurring more debt increases the company's risk and raises the cost of equity.

If enough debt is incurred, the reduction in the cost of capital due to an increase in the debt-to-equity ratio may be offset by the increase in the cost of equity, resulting in no change, or the worst case scenario, increasing the cost of capital.

Therefore, going back to the pecking order theory, firms generally prefer to issue debt where necessary. Still, if it is dangerous to do so, they will opt for equity instead. The most preferred option will still remain as internal financing because that has no cost at all.

Therefore, knowing that firms will require funding at different points in time, its capital structure is solely the result of the decisions made by the management, given the market conditions and health of the firm at those same points in time.

Researched and authored by Jasper Lim | Linkedin

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?