Homemade Leverage

A financial practice to utilize the investors' personal borrowings to modify the firm's financial leverage.

What is homemade leverage?

Homemade leverage is a financial practice to utilize the investors' personal borrowings to modify the firm's financial leverage.

Homemade leverage applies to companies with no debt in their portfolio. In other words, these firms are unlevered. As we saw in the previous section, using fixed-income instruments maximizes EPS.

A fundamental principle of investing is that investors must get returns proportional to the risk they adopt by purchasing the firm's stock. Firms that issue fixed-income instruments to finance their operations are usually considered risky.

The risk associated with employing fixed-income instruments is called financial risk. Firms that issue bonds and debentures must earn enough revenue to cover interest expenses.

Financial risk is when the business cannot cover its fixed finance costs. As a result, such firms would have to increase EBIT to meet their obligations.

There is a considerable risk and the possibility of a significant return for the investor. Therefore, if the increase in EPS caused by financial leverage is more than the increase in EBIT, employing fixed-income instruments is considered favorable.

How can firms not carrying financial risk ensure a greater return for their shareholders? Simple answer. They don't.

Shareholders who want to gamble on riskier investments will borrow funds at the same rate as the company. Doing so can introduce leverage into the business and replicate the risk they desire. This is homemade leverage.

The idea of homemade leverage rests on the capital structure theory introduced by Amedeo Modigliani and Merton Miller. To understand the concept of homemade leverage, we must dive into this theory's motivation, principles, and criticisms.

- Homemade leverage is when individual investors borrow personal funds to invest in a company's equity instead of relying on the company's debt financing.

- This approach gives investors greater control over their risk exposure and financial structure, allowing them to tailor their leverage according to their personal risk tolerance and investment strategy.

- Homemade leverage aligns with the Modigliani-Miller theorem, which states that under certain conditions, the value of a firm is unaffected by its capital structure.

- Investors can customize the degree of leverage they take on, enabling them to optimize their returns and manage risk based on their individual financial situation and market outlook.

What Is Leverage?

In financial management, leverage is the application of fixed income to finance business operations. Since the interest or dividends do not change with output, maximizing output and reducing variable costs can maximize earnings.

There are broadly two kinds of leverage - operating leverage and financial leverage. Through operating leverage, firms seek to maximize earnings before interest and tax by maximizing sales revenue.

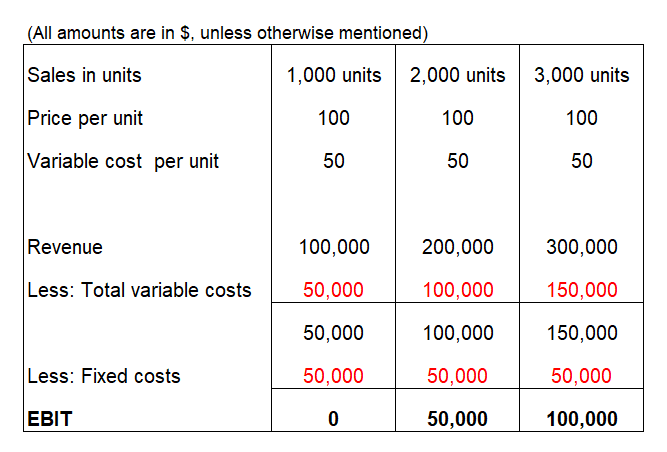

Let us look at the example of a company that sells a component for $100 per unit and incurs costs of $50 per unit on production. Therefore, irrespective of output, it must incur $50,000 per year. These are fixed operating costs.

Under different output scenarios, we can calculate the earnings before interest and tax (EBIT).

As we can see, an increase in sales revenue causes EBIT to increase because the fixed costs remain unchanged. Therefore, operating leverage is concerned with using fixed operating costs to maximize EBIT.

On the other hand, financial leverage is concerned with using fixed finance costs such as interest, taxes, and dividends to maximize the earnings per share.

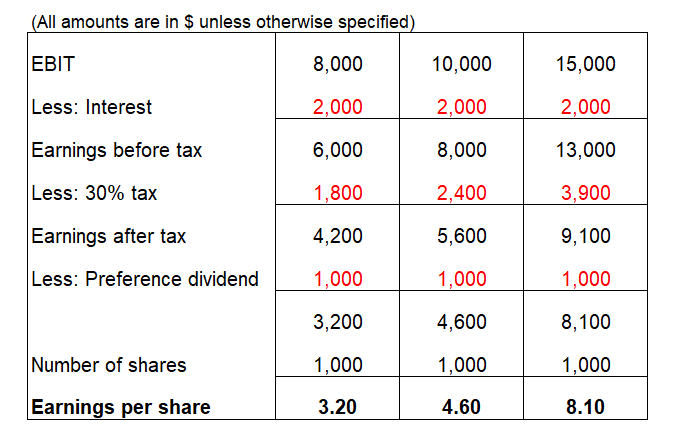

To understand financial leverage, we can look at the example of the same company; only now, it has to pay an annual interest of $2,000 and 30% of its earnings before tax as a tax payment. The business also paid a preference dividend of $1,000 this year.

Under different EBIT scenarios, we can calculate the earnings per share (EPS), assuming there are 1,000 shares outstanding.

As we can see, an increase in EBIT causes EPS to increase because the fixed finance costs remain unchanged. Therefore, financial leverage is concerned with using fixed finance costs to maximize EPS.

The major capital structure theories

Now, we know that the greater the leverage, the greater the financial risk associated with the company. So the objective of financial management is to maximize the wealth of shareholders.

Financial leverage concerns the Proportion of debt in the firm's capital structure. As a result, the company must adopt a capital structure to maximize its value and shareholder wealth.

This mix is what we can call the "optimal capital structure." In other words, this mix of debt and equity will contribute best to shareholders' wealth. So, what are these capital structure theories, and where do they factor in?

There are three fundamental theories regarding the capital structure that have contrasting viewpoints. These theories are:

- The net income approach, proposed by David Durand

- The net operating income approach, also proposed by David Durand

- The Modigliani-Miller theorem

The net income approach, penned by Durand, believes that the firm's capital structure is relevant to its valuation, while the following two theories hold otherwise.

Since the Modigliani-Miller theorem is the hypothesis that deals with the concept of "homemade leverage," we will explore this theory in detail in an upcoming section.

First, look at Durand's theories to get some background into the workings of leverage and valuation.

Durand Theory 1 - Net Oncome Approach

Durand laid down the net Income approach to suggest that a firm's capital structure choice is relevant to its valuation. In other words, a change in the capital structure will change the company's cost of capital and its total value.

We can measure the firm's financial leverage (capital structure) through its debt-equity ratio.

The net income theory makes a set of assumptions:

- Taxes do not exist

- The firm can raise debt at a lesser cost than equity. In other words, the cost of debt is less than that of equity.

- We learned that the use of debt brings with it financial risk. However, the net income theory assumes that the shareholders' risk perception does not change, even if the firm employs more debt.

The overall cost of capital is the weighted average of the cost of debt and equity (the weights being the Proportion of the two sources of funds in the capital structure).

Since the shareholders' risk perception remains the same irrespective of the debt employed, the firm can raise as much debt as required, and the cost of equity and debt remains unchanged.

In reality, employing more debt leads to greater financial risk, and shareholders will want a greater return to compensate them for this risk, leading to an increase in the cost of equity.

Since debt is cheaper than equity, employing more debt will reduce the overall cost of capital.

It naturally follows that reducing the cost of capital will positively impact the firm's value. The greater the amount of debt employed, the higher the price of the firm's shares.

The "optimal capital structure" is when the firm's value is the highest, and the cost of capital is the least.

Durand Theory 2 - Net Operating Income Approach

Durand suggested another theory that sharply contrasts the net income theory. According to the net operating income hypothesis, the firm's capital structure is irrelevant to its valuation.

In other words, no matter the leverage in the firm's portfolio, its value remains unchanged. As a result, the firm's influence affects neither the market price nor the cost of capital.

Another assumption of the net operating income theory is that the company's lenders do not perceive any risk in the firm's adoption of debt. Therefore, the cost of debt remains constant.

Since the firm's value is unaffected by leverage and the importance of debt is constant, the equity value can be derived by deducting the debt discount from the firm's value.

This theory accounts for the presence of financial risk. Durand states that adding more debt into the business's portfolio would increase its financial risk.

Since equity shareholders are exposed to more risk, they would expect more significant returns. As a result, the cost of equity increases. The increase in the cost of equity is directly proportional to the increase in the debt-equity ratio.

I mentioned before that the overall cost of capital is constant. Ever wondered why? Well, using more debt would reduce the overall cost of capital, as debt is considered a cheaper alternative. This is according to the net income approach.

However, if the cost of equity increases with more debt, the advantage of using debt is exactly countered by such an increase.

In short, according to the net operating income approach, there is no such thing as an optimal capital structure, as the firm's total value is unaffected by leverage.

Homemade leverage and the Modigliani-Miller (MM) theorem

Now that we know what the various capital structure theories propose let us look at the approach that brought about the concept of homemade leverage.

As discussed earlier, homemade leverage applies to companies that do not have debt on their books. Therefore, the investor must borrow money to introduce obligation into the capital structure.

Amedeo Modigliani and Merton Miller agree with Durand's net operating income theory in that a firm's valuation is independent of its capital structure. The basic principles are guiding the theorem mirror those proposed by Durand.

- The cost of capital is constant, and the value of the business is unaffected by changes to its capital structure.

- The more the company employs debt, the more financial risk there is associated with the company. The shareholders will want a more significant return proportional to this risk, increasing the cost of equity.

The MM hypothesis makes assumptions fundamental to understanding these theoreticians' thought processes.

- The market in which the firm operates is perfect. This means that all investors have equal information, can buy business shares freely, and do not incur transaction costs.

- Investors have the same borrowing power as a corporate entity. You will see why this is important later.

- All businesses within a similar industry have the same risk associated with them.

- Every investor has the same projection and outlook of the firm's earnings.

- The firm does not retain money. All earnings are paid out as dividends.

- There are no taxes. Now, this is one of the significant flaws in the theory. Modigliani and Miller themselves address this.

How do Modigliani and Miller justify their theory?

The MM theory lies on the bedrock of the arbitrage argument. To understand what arbitrage means, let us take the example of the shares of MonkeyArmy Ltd.

Assume that, as of today, the shares are trading at $125.71 on the New York Stock Exchange (NYSE). However, the stakes are trading at $125.82 on the Hong Kong Stock Exchange (HKG). Usually, these differences are minuscule and last for seconds.

When such price differences exist, the trader who owns shares of MonkeyArmy Ltd. will sell these shares in the market where the price is higher (HKG) and repurchase them from the market where the price is lower (NYSE), pocketing a profit.

Exploiting such price differences is essentially the principle of arbitrage. When price differences exist, the market fixes them through arbitrage.

In the context of leverage, the MM hypothesis assumes the existence of two companies. They are identical except for one key difference: one business has employed debt, and the other is a pure equity firm.

Since Modigliani and Miller hold that capital structure is irrelevant, they also presuppose that, like the shares of MonkeyArmy Ltd., which cannot trade at two different price points, the values of both these firms cannot be other.

Through arbitrage, shareholders will sell the company's shares with a higher value and buy shares of the company with a lower value.

This will result in the value of the firm whose shares are being sold declining and the value of the firm whose shares are being bought increasing until equilibrium is restored.

Suppose the shareholder of a levered firm wants to sell their shares. In that case, they will borrow money in the Proportion of debt in such a firm's portfolio and invest it in shares of the unlevered firm, introducing debt into their capital structure.

Essentially, by replicating the levered firm's capital structure, the investor has introduced what is known as "homemade leverage."

A numerical example of the Arbitrage Argument

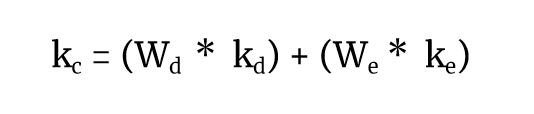

Before exploring the example, it is important to note how the overall cost of capital is calculated.

Where

- kc = Overall cost of capital

- kd = cost of debt

- ke = cost of equity

- Wd = Proportion of debt in the capital structure

- We = Proportion of equity in the capital structure

Let us now look at a numerical example to understand how arbitrage works.

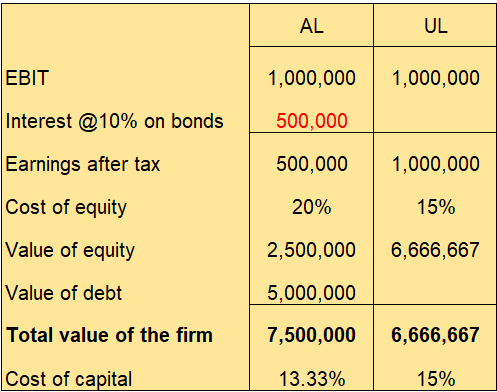

Assume that there are two firms, UL and AL, the unlevered firm, and AL, the levered firm.

The only difference between the two firms is that AL has bonds worth $5 million, carrying an interest of 10%. Both firms have the same earnings before interest and tax (EBIT): $1 million. Since AL is levered, its cost of equity would be higher.

Let us say that AL's cost of equity is 20%, and UL's cost of equity is 15%.

We can see that the value of the levered firm is higher than that of the unlevered firm. As a result, investors would sell shares of AL and purchase shares of UL to bring the market to equilibrium.

Assume that Patrick holds a 10% stake in AL. Since the equity value is $2.5 million, Patrick's share would be $250,000. Since the cost of equity is 20%, Patrick would receive a dividend of 20% from his share. The dividend would amount to $50,000.

Patrick would now have to introduce homemade leverage. Since the firm has bonds worth $5 million, Patrick would take a loan proportionate to his stake in the firm. He will have to borrow $500,000 at 10% interest (same as the firm's interest rate).

On Patrick's loan, he would have to pay interest of $50,000.

Now that he has bought a 10% stake in UL, his holdings will amount to $666,667, 10% of the firm's equity value. In addition, UL's capital cost is 15% so Patrick will receive a dividend income of $100,000 from UL.

Patrick's dividend income from UL 100,000

Less: Patrick's interest obligation of 50,000

Patrick's net income by investing in UL 50,000

Notice that Patrick is getting the same income of $50,000 that he was getting as a shareholder in AL. However, this time, his investment outlay is lower.

- Patrick's stake in UL 666,667

- Patrick's borrowing - 500,000

- Patrick's investment - 166,667

Contrastingly, his own investment outlay in AL was $250,000. The magic of homemade leverage!

Challenges with homemade leverage

A fundamental issue with Modigliani and Miller is that it assumes that homemade leverage is a perfect replacement for debt in the business's books.

There seem to be a few issues with this assumption. So, let's look at them and see whether personal and corporate leverage is perfect substitutes.

- Companies are subject to the limited liability principle. An investor's risk exposure is much higher if he borrows in his own name because he can be made personally liable to pay off the debt.

- The investor would have to oversee all the legal formalities if he borrow in his own name. The company has already taken care of these formalities in a levered company. This, however, is a weak issue. Let's dig deeper.

- Large business entities can borrow at lower interest rates because they are usually extremely creditworthy. However, this might not be the case for individual investors. The interest rates charged would be much higher. As such, there is no way we can consider corporate and personal leverage perfectly substitutable.

- The MM theory assumes that there are no brokerage costs. However, if these costs are factored in, the shareholder would actually have to sell a much bigger stake than required to get the same amount as he was getting in the levered company.

However, the fundamental problem with the MM hypothesis arises when taxes are considered.

Taxes

The Modigliani-Miller theorem assumes that taxes do not come into the picture. However, both theoreticians reached a consensus and eventually admitted that corporate taxes would change the very foundations of the theory.

Modigliani and Miller provided a framework to explain the role of taxes and how they fit into their theory.

The interest that a business pays on its borrowings is usually tax-deductible. For example, if the interest on the firm's debt is 10%, and the firm is liable to pay a tax of 30%, its effective interest rate would only be 7%.

It naturally follows that the firm that employs debt would have a greater value and a lower cost of capital. The income available to be distributed to equity shareholders increases because of the reduction in interest costs.

Modigliani and Miller state that the value of the firm that employs debt would be more than the value of the unlevered firm by the amount of the tax savings it accrues.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?