What Are Options?

Options are sophisticated financial instruments that derive their value from an underlying asset, such as a stock, bond, commodity, or currency.

What Is an Option?

An option is a financial derivative that grants the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a specific period. The fundamental components of an option contract include the underlying asset, strike price, expiration date, and type.

Options are sophisticated financial instruments that derive their value from an underlying asset, such as a stock, bond, commodity, or currency. They represent a contract between two parties, granting the holder the right to engage in a future transaction involving the underlying asset.

Their advantages lie in their flexibility and asymmetric risk profile. They allow the holder to gain exposure to the underlying asset's potential price movements by paying a relatively small premium upfront.

This premium is the cost of acquiring the option contract and represents the maximum potential loss for the buyer.

Options' versatility extends far beyond speculative strategies. They can be employed as potent risk management tools, allowing investors to hedge existing positions in the underlying asset against adverse price movements.

- Options provide the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a specific time period.

- A call option gives the buyer the right to buy a security at a given price.

- A put gives the buyer the right to sell a security at a given price.

- They can be used for hedging risk or speculating.

- Factors influencing contract pricing include the underlying asset's price, strike price, time to expiration, implied volatility, and interest rates.

History of Options

The history of options can be traced back to ancient times when contracts involving the rights to future transactions were used in trade and commerce. In the 17th century, they were traded at exchanges in London, Amsterdam, and Paris.

However, their modern form emerged in the latter half of the 20th century, when organized exchanges, such as the Chicago Board Options Exchange (CBOE), facilitated their standardized trading.

In the latter part of the 20th century, the introduction of the Black-Scholes model and the subsequent Nobel awards legitimized the work of derivatives traders and exchanges. As a result, their use has proliferated across and beyond the financial sector.

Contemporary study of options dates to the late 19th and early 20th century, to Louis Bachelier, the doctoral student of the renowned mathematician Henri Poincaré. His work on diffusion processes and random walks predated Albert Einstein’s work on Brownian Motion.

He passed away relatively obscure; however, rediscovering and later translating his work by influential mathematicians such as Andrey Kolmogorov and Paul Lévy brought his work to mainstream salience.

His seminal work and concepts predate the analysis of stock prices as random walks, which is closely related to the Efficient Market Hypothesis. Bachelier’s work provided the foundation for later development of the Black-Scholes Model.

How are Options used?

They are mainly used for three purposes:

- Hedging: They allow investors to mitigate risk by offsetting potential losses in their underlying positions. For example, a stock owner can buy puts to protect against downside risk. Meanwhile, a short seller can buy calls to limit potential losses if the stock price rises. Options provide an effective way to manage portfolio risk without necessarily liquidating the underlying position.

- Speculation: Options provide leverage, allowing investors to take positions with limited capital outlay. An investor can take a directional view on a stock by buying a call or a put. The leverage inherent in options amplifies potential gains (and losses) relative to the upfront premium paid.

- Arbitrage: They can be used to benefit from pricing inefficiencies and to take a relative value bet.

Key Factors of Options

The six relevant key factors are:

- S: Price of the underlying asset

- K: Strike price

- r: risk-free rate

- 𝝈: implied volatility

- T: time to expiry

- 𝜹: dividend rate

The strike price is determined at the time of purchase. It is the price at which the holder can exercise the contract to buy or sell the underlying asset. Similarly, the time to expiry is also set at the initial purchase.

Implied volatility is the market’s expectation of volatility for the duration of the option’s life. An important thing to note is that implied volatility is not realized volatility.

Beyond these factors, first and foremost is the description of the payoff at expiry. For instance:

-

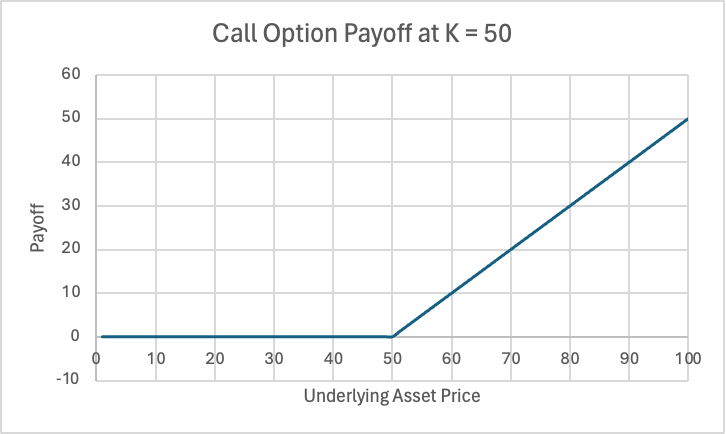

A call pays max(0, ST - K) at expiry,

-

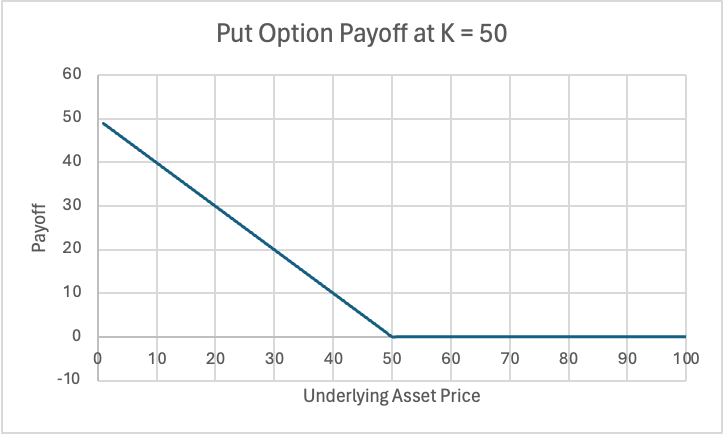

A put pays max(0, K - ST) at expiry.

The expiration date is the date on which the contract becomes void, and the holder must decide whether to exercise or let it expire worthless. Options can be exercised on or before the expiration date, depending on their style, American or European.

An American option (only related in name) can be exercised before expiry. Meanwhile, a European one can only be exercised at expiration.

These factors allow us to value options. The underlying asset could be any asset, such as a bond, stock, commodity, currency, or another derivative.

Moneyness

Options in their lifecycle can be broadly grouped under 3 categories depending on the underlying asset’s price. These categories are:

- In-the-money: Positive payoff if it were to expire today

- At-the-money: Underlying asset is trading at the strike price

- Out-of-money: No payoff if it were to expire today

Moneyness is an important term when referring to derivatives. It provides broadly the reference from which important properties are later inferred.

Options Risk Metrics: The Greeks

The Greeks are essential measures used to quantify the risk and sensitivity of options to various factors. Some of them are:

Delta

It measures the rate of change in an option's price with respect to changes in the underlying asset's price. Delta ranges from 0 to 1 for calls and from 0 to -1 for puts.

A delta of 0.5 for a call implies that for every $1 increase in the underlying asset's price, its value will increase by $0.50.

Gamma

It represents the rate of change in delta for a given change in the underlying asset's price. It measures the convexity or curvature of the option's value. Gamma is the highest at the money.

Gamma is particularly important for derivative traders who need to actively manage their delta exposure as the underlying asset price moves. As gamma is almost never zero, the delta changes when the underlying asset’s price changes.

Theta

It measures the rate of change in an option's price with respect to time, assuming all other variables remain constant. It quantifies the time decay of a contract’s value as it approaches expiration.

Options with longer expiration times tend to have lower theta values as time decay accelerates closer to expiration. Theta is generally negative for a long-option position.

Vega

It measures the sensitivity to changes in the underlying asset's implied volatility. Higher volatility generally increases the value of the contract, as it increases the probability of larger price movements.

Vega is crucial for traders who need to manage their exposure to implied volatility risk. A crucial point is that realized volatility is not necessarily implied volatility. Markets are forward-looking, and the past does not necessarily predict the future. Vega is not a Greek letter.

Rho

It measures sensitivity to changes in interest rates. Rho is more significant for longer-term options, as interest rates have a greater impact on their present value. It is particularly relevant for contracts on interest rate-sensitive instruments, such as bonds.

Psi

It measures the change in price with respect to the change in the dividend yield of the underlying asset.

Option Pricing Methods

Pricing options accurately is crucial for effective risk management, trading strategies, and valuation. Several models have been developed to determine fair prices, each with its own assumptions and applications.

Binomial Model

Originally derived by William Sharpe and later formalized by Cox, Ross, and Rubinstein, this discrete-time model uses a binomial tree to represent the possible movements of the underlying asset over time.

It considers the asset's price movements and the time to expiration. The binomial model assumes that the underlying asset can only move up or down by a certain amount in each time step, with probabilities derived from the asset's volatility and risk-free rate.

The Binomial model approaches the Black-Scholes Model result by reducing timesteps to infinitesimal length.

Trinomial Model

An extension of the binomial model, it incorporates three potential price movements (up, down, and unchanged) at each node.

Monte Carlo Simulations

It is a computational method that generates pseudo-random numbers to simulate possible outcomes. These computational methods use random sampling techniques to simulate multiple possible scenarios for the underlying asset's price over time.

Complex option structures and underlying asset dynamics can be simulated, including stochastic volatility, jump processes, and non-normal distributions. Monte Carlo simulations are particularly useful for pricing exotic options and derivatives where payoffs are path-dependent.

Black-Scholes Model

Developed by Fischer Black and Myron Scholes, this widely used model provides a closed-form solution for pricing European-style options.

It relies on assumptions such as constant volatility, continuous hedging, zero-trading costs, and log-normal asset price distribution. All of which turns out to be incorrect in real-life applications.

Still, the Black-Scholes model is renowned for its simplicity and tractability, making it a popular choice for pricing vanilla options as an initial approximation.

Further on Pricing Models

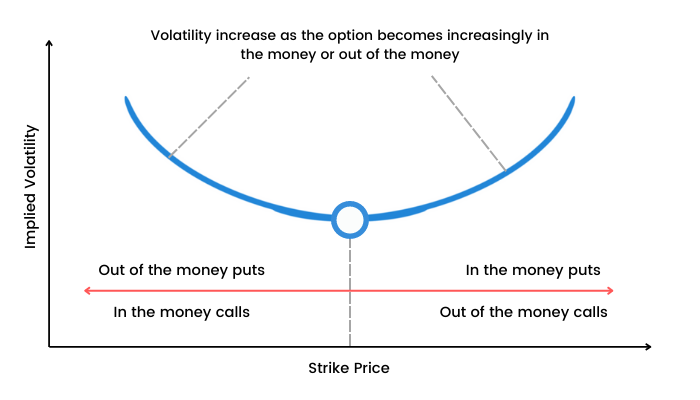

Specifically, in the case of the Black-Scholes Model, it does not explain commonly observed phenomena such as volatility smiles or skews. Implied volatility across strike prices and across time is not constant.

Additionally, the work pioneered by Paul Lévy and Benoit Mandelbrot showed that stock returns are also not normally distributed but have fat tails. Ultimately, the Black-Scholes model does not capture these phenomena.

More sophisticated models, such as Merton and Heston, were later developed to explain some of these observations. That being said, it is important to recognize that all pricing models are, at the end of the day, just models. They do not necessarily describe the real world.

For instance, none of the models mentioned above takes liquidity into account. Executing trading strategies based purely on pricing models without considering market microstructure will lead to large losses.

Exotic Options

In addition to standard contracts, there are various exotics that cater to specific risk profiles and trading strategies. Some of them are:

- Barrier: These have an additional condition related to the underlying asset's price reaching a predetermined barrier level. Barrier options can provide cheaper premium structures, but also carry additional risk.

- Swaptions: These are options on swaps, giving the holder the right to enter into a swap agreement at a predetermined fixed rate on a future date. Swaptions are commonly used by financial institutions and corporations to manage interest rate risk and hedge their exposures.

- Asian Options: The payoff of these contracts depends on the average price of the underlying asset over a specific period rather than the spot price at expiration. They are less sensitive to price fluctuations and are often used in commodity markets to smooth out volatility.

- Compound: These are derivatives where the underlying asset is another option contract. They offer additional leverage and flexibility but also carry a higher risk.

- Rainbow: These options have multiple underlying assets, with the payoff depending on the performance of one underlying asset. Rainbow options allow investors to gain exposure to multiple assets.

- Basket: These options, similar to Rainbow, have multiple underlying assets. However, the payoff is usually structured as a weighted average of all underlying assets.

Pricing exotics often requires more sophisticated models and techniques, as closed-form solutions in many cases may not exist.

Typical Option Strategies and Positions

Options are highly versatile instruments that offer the possibility of hedging and speculating. Exposure to underlying risk factors can be obtained through a myriad of positions. Here are some of the well-known option positions.

Delta Hedging

Delta hedging is an option strategy where a trader aims to achieve positive PnL by betting on the implied volatility and realized volatility discrepancy. In other words, the trader has a view on the future realized volatility.

A common position to take is to long N number of calls with delta 𝚫 and short 100x𝚫xN shares to achieve delta neutrality (assuming each option holds 100 of the underlying security). By doing so, the trader hopes to see realized volatility larger than implied volatility.

Since the gamma is positive, if the price goes up significantly, the trader will realize larger gains from the options as the delta increases. Similarly, if the price goes down significantly, short stocks will gain more value compared to the value lost by the options as the delta decreases.

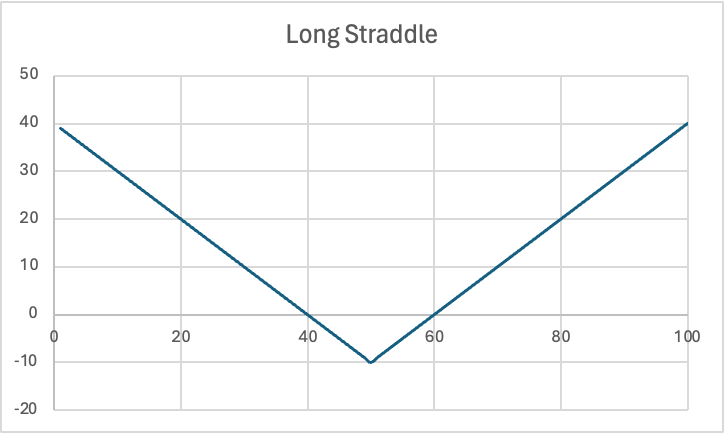

Straddle

The straddle is an option strategy in which the trader takes a long put and long call position. The aim is to bet on volatility. A large change in price results in profit. However, a low price change results in a loss.

Alternatively, a short position on volatility can be achieved by shorting a straddle.

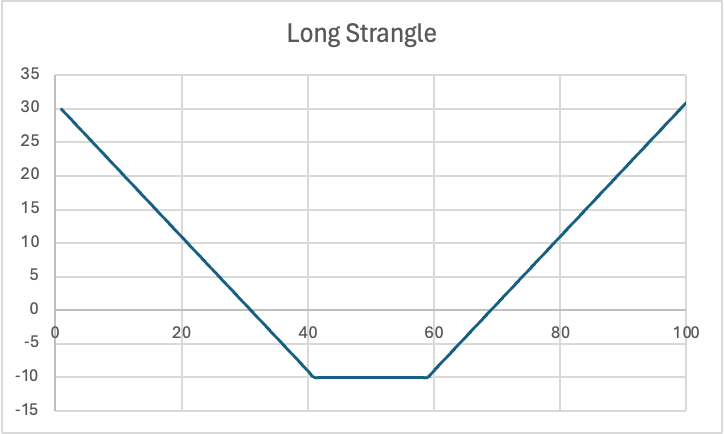

Strangle

Similar to a straddle, a long strangle position can be created by buying a put and a call. The difference is that the call has a higher strike price than the put. Again, this position allows one to take a directional bet on future realized volatility.

A strangle will be cheaper than a straddle. However, the price movement needs to be higher than that of a straddle for the strategy to realize profits. Similarly, a short strangle position can be utilized to short volatility.

Options in Corporate Finance Applications

Options have found interesting applications beyond derivative markets. One of these areas is evaluating a firm's capital structure. Recognizing debt and equity as contingent payments on a firm’s assets makes it possible to treat them as options.

It is possible to price debt and equity by noting a firm’s assets as the underlying security while modeling debt and equity as options. This also provides an additional way to model distressed debt. The following is an example.

Corporate Finance Example

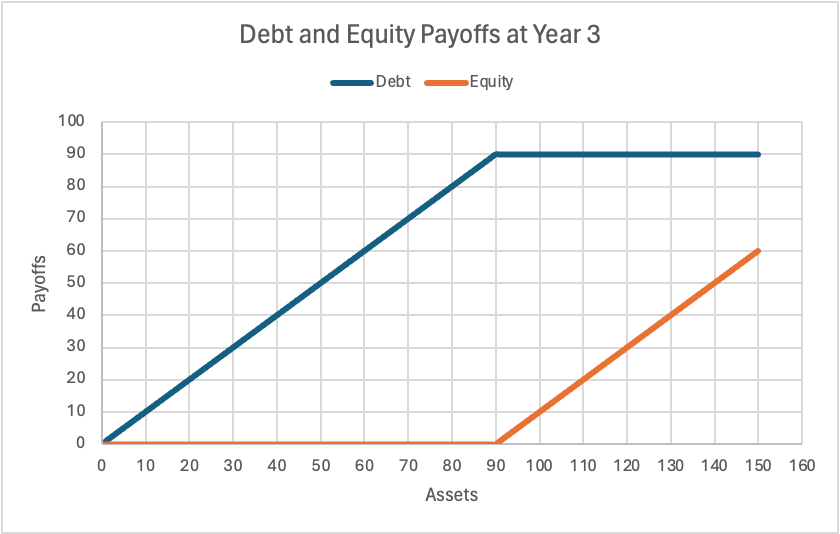

Firm A’s assets are currently valued at $100 million. It has zero-coupon debt with a face value of $90 million, which is maturing in 3 years' time. It has no cash. We start by plotting the debt and equity payoffs.

It is immediately noticeable that the payoff of the equity is, in fact, the same as a call. We can write the payoff for equity at year 3 as,

E3 = max(0, Assets - D3)

D3, the strike price, is $90 million in this case. By modeling the volatility for assets, we can use the Black-Scholes model to price the equity, E0.

Furthermore, we can apply the fundamental accounting equation,

Assets = Liability + Equity

If we have calculated E0, then today’s value of debt would be

D0 = A0 - E0

We can iterate this exercise if there are multiple tranches with junior debt to price all tranches.

From this point, valuing a credit default swap (CDS) is also straightforward for this firm’s debt.

Recognizing that the payoffs from a CDS and the risky debt should total a risk-free debt’s payoffs (effectively treating CDS as a put option), we can quickly write the following equation: (assume r as the annually continuous compounding rate)

$90million * e-rT = CDS + D0

By moving D0 to the left side of the equation, we can find the premium for the CDS.

Conclusion

Options are powerful financial instruments that offer tremendous flexibility and versatility in trading and investment strategies. Their ability to provide leverage, hedge risk, and facilitate speculation makes them invaluable tools.

At their core, they represent the right, but not the obligation, to buy or sell an underlying asset.

However, the complexity of options also necessitates a deep understanding of the various factors influencing their pricing, such as the underlying asset's price, strike price, time to expiration, implied volatility, and interest rates.

The Greeks, Delta, Gamma, Theta, Vega, Rho, and Psi provide crucial insights into the sensitivity of option prices to these variables, enabling traders to manage their risk exposures effectively.

The advent of sophisticated pricing models, like the Binomial model, Black-Scholes model, and Monte Carlo simulations, has revolutionized the way options are valued and traded.

These models, along with their extensions and adaptations for exotic options, allow market participants to price and structure complex derivative products tailored to their specific investment objectives and risk profiles.

Options FAQs

American options can be exercised before expiration, while European options can only be exercised on the expiration date.

The option premium is the price the buyer pays to the seller for the contract.

Implied volatility is a measure of the market's expectation of future volatility in the underlying asset's price.

A: The Greeks (Delta, Gamma, Theta, Vega, Rho and Psi) are measures used to quantify the sensitivity of an option's price to various factors.

Hedging involves taking an offsetting position in an option to reduce or mitigate the risk associated with an existing position in the underlying asset.

Market makers provide liquidity in the options market by consistently quoting bid and ask prices for various contracts.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?