Venture Capital Valuation Method

Discover the Venture Capital Valuation Method, a key tool for investors to assess early-stage startups

What is the Venture Capital Valuation Method?

The Venture Capital Valuation Method is one of the start-up valuation methods that investors and investors use to value early-stage startups based on expected future returns.

In startup funding and early-stage investments, venture capital is key to helping early-stage companies grow. However, one of the biggest challenges for both investors and entrepreneurs is figuring out how much a startup company is really worth, especially when it doesn’t have significant revenue or a financial history to lean on.

This is where the Venture Capital Valuation Method comes to the rescue. It is one of the most widely used in the startup space to value companies in their early stages.

Where traditional valuation models focus on established companies with steady cash flows, where we can utilize the DCF method and Comparable Company Analysis, this method is tailored to high-risk, high-reward startups due to their lack of positive cash flows and appropriate comparable peers.

The VC valuation method involves forecasting a company's potential exit value and then discounting it to the present to determine its current worth.

In this article, we will explain the VC Valuation Method, how it works, and how it compares to other types of VC valuation methodologies. We'll also review its advantages, limitations, and essential considerations for startups and investors.

- The Venture Capital (VC) Valuation Method is a framework venture capitalists use to estimate the value of a startup or early-stage company. It helps investors determine how much equity to receive for their investment.

- Venture capitalists use pre-money and post-money valuations to understand the company’s worth before and after investment. Pre-money valuation is the company’s value before investment, while post-money includes the VC’s capital infusion.

- This method focuses heavily on future growth projections, estimating the company’s potential value at exit (e.g., through an IPO or acquisition) and working backward to determine the current valuation.

- VC investors also consider equity dilution when calculating valuation. As more funding rounds occur, existing ownership stakes are diluted, so investors calculate how much ownership they need initially to achieve their desired return.

Understanding the Venture Capital Valuation Method

The VC valuation technique was developed for early-stage startups with high growth potential and associated high risks. The approach is centered around estimating the company's potential value and discounting it back to the present. This is done to execute the investment's potential returns.

The biggest challenge in valuing early-stage startups is the absence of consistent revenues, profits, or historical data. This absence of critical historical data makes it difficult to assign precise values to financial projections and forecasts, leading to obstructions in the company's valuation.

Financial metrics traditionally used to value established companies, like the PE ratio, can not be used in this aspect due to limited historical financial data. Nor can we use Discounted Cash Flow (DCF) valuation, which is based on projecting future cash flows of the firm and assessing the intrinsic value of the company.

This factor makes the VC valuation method a critical tool designed to aid VCs and entrepreneurs in assessing the true value of early-stage startups.

Steps in the Venture Capital Valuation Method

The VC valuation technique is one of the most used approaches for pre-revenue startup valuation that does not have adequate historical financial information. The valuation depends upon the amount of investment required, the exit value, the weighted average cost of capital or required rate of return, and exit multiples.

The calculation's backbone is the projection of the company's exit value and discounting it at the required rate of return specified by the investors.

The Venture Capital Method consists of the following six steps:

- Estimating the Investment Requirement: We estimate the total investment our venture will require to push it from the startup stage to the growth stage.

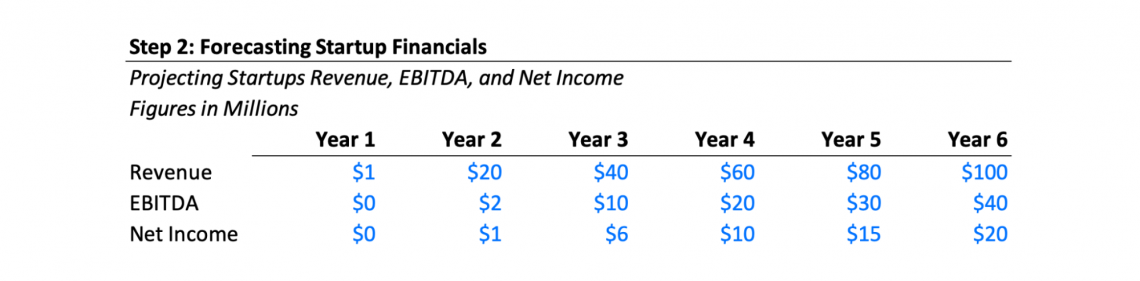

- Forecasting the Startup Financials: Startup financials include potential revenues, EBITDA, and Net Income. They must be projected over a specific time frame, typically five years.

- Determine the Timing of Exit: Determining when the VCs want to exit the firm. It's important to establish when the investor expects to exit the investment, usually executed through an IPO or merger/acquisition.

- Calculate Exit Multiple: Use comparable companies to determine appropriate earnings multiple (e.g., EV/EBITDA or revenue multiples) that will be applied to the startup's projected earnings at the exit time.

- Discounting the Exit Value to Present: Apply the investor's required rate of return (often between 20% and 50% for high-risk startups) to discount the future exit value back to its present value.

- Determine Valuation and Desired Ownership Stake: Calculate pre-money and post-money valuations, which help determine the level of equity an investor receives for their investments.

If you are interested in learning what VC interviews may look like, it's worth reviewing Venture Capital Interview Questions to see how these valuation concepts are often tested in interviews.

Example of Venture Capital Valuation

For example, we will run a hypothetical scenario of FinTcorp, a fintech startup looking to acquire initial investment from investors in the initial rounds.

Estimating the Investment Requirement

FinTcorp seeks $10mm in the initial investment in the first round of investments.

Forecasting the Startup Financials

The Financials are projected for six years, assuming the revenues grow by $20mm annually.

Determine the Timing of Exit

The VCs are expected to exit the investment by the end of year 6.

Calculate Exit Multiple

The comparable companies or comps or comparable peers are trading at 12x earnings. If the NI in the final year is $20m, then the exit multiple should be $240m.

Discounting the Exit Value to Present

Let us assume the investors' desired discount rate is 40%, and there is no debt in the capital structure.

So the discounted value of exit would be:

$240 / (1.4)^6 = $31.87m

Determine Valuation and Desired Ownership Stake

The post-money valuation is $31.87m, which is after we receive the funding.

The pre-money valuation would be:

$31.87 - $10m = $21.87m

When we divide the initial investment of $10m by the post-money valuation of $31.87m, we will know the amount of equity the VCs own.

$10 / $31.87 = ~31%

Advantages and Limitations of the VC Valuation Method

Although the VC valuation method is one of the most used valuation methodologies in the early-stage valuation landscape, it is noteworthy to go through its advantages and limitations.

Let us discuss the advantages and limitations of the VC valuation method below.

Advantages

The following are the advantages of the VC valuation method:

- Future-Oriented: The primary focus of the VC Valuation Method is the startup's future potential. This future growth should align with venture capitalists' objective of elevated returns from high-growth startups.

- Realistic Expectations: The valuation method sets realistic expectations for VCs and entrepreneurs by taking exit scenarios into consideration ensuring both are in alignment with the same financial goals.

- Flexible for High-Risk Investments: The startups are a high-risk and high-reward investment that demands the investors to adjust for high-risk premiums.

Limitations

The following are the limitations of the VC valuation method:

- Difficult Exit Projections: Exit value is the figure established on assumption-based projections that are highly speculative. This is particularly true in the case of tech or biotech companies.

- Subjectivity in Required Return: The required rate of return varies from investor to investor. The differences in the RoR can result from the differing risk tolerance, market conditions, and the investor’s policy.

- Ignores Current Market Conditions: The excessive reliance on the future projections makes the valuation method to ignore the ongoing market conditions that derail the valuation from the results that could have been if market conditions were taken into consideration.

Comparison with Other VC Valuation Methods

Different venture capitalists and investors use various methods to value early-stage startups. Below, we will compare the Venture Capital Valuation Method with three commonly used methods:

- The Scorecard Valuation Method,

- The First Chicago Method, and

- The Berkus Method.

Scorecard Valuation Method

The Scorecard Valuation Method compares the startup with other similar startups that have already received funding. This method looks at factors such as the team's strength, the size of the opportunity, the technology, and the product. Investors assign weights to these categories to create a score that helps determine valuation.

First Chicago Method

The First Chicago Method uses best, worst, and base case scenarios for startup valuation where each scenario is assigned a probability, and the expected value is calculated based on weighted averages.

Berkus Method

The Berkus Method assigns value to startup aspects like ideas, prototypes, teams, and strategic relationships. These values are summed up to calculate the total valuation.

| Valuation Method | Key Focus | Advantages | Limitations |

|---|---|---|---|

| Venture Capital Valuation Method | Potential exit value, discount rate | Future-oriented, realistic expectations | Speculative exit projections, subjective return requirements |

| Scorecard Valuation Method | Comparable startups | Simple and quick to apply | It may not reflect startup uniqueness |

| First Chicago Method | Multiple scenarios (best, worst, base) | Considers a range of outcomes | Complex and time-consuming |

| Berkus Method | Startup components | Easy to use for early-stage startups | Subjective relies on qualitative factors |

Conclusion

The Venture Capital valuation method is a critical tool for early-stage investment and startup valuation for its focus on the estimation of startups future value and discounting it back to the present using the specified required rate of return. This method is preferred for its alignment with high-risk and high-reward approaches.

Like any other approach, we may go for valuing a startup/company, it has challenges that users may face when using it. This may include overreliance on projections, varying required rates of return across different investors, and ignoring the market conditions in the assumptions and calculations.

When comparing the VC valuation method with other VC valuation techniques, this method stands out for its future orientation. The results can be used in conjunction with other VC valuation methods to reap its benefits.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?