AUM / IP - Does it Matter?

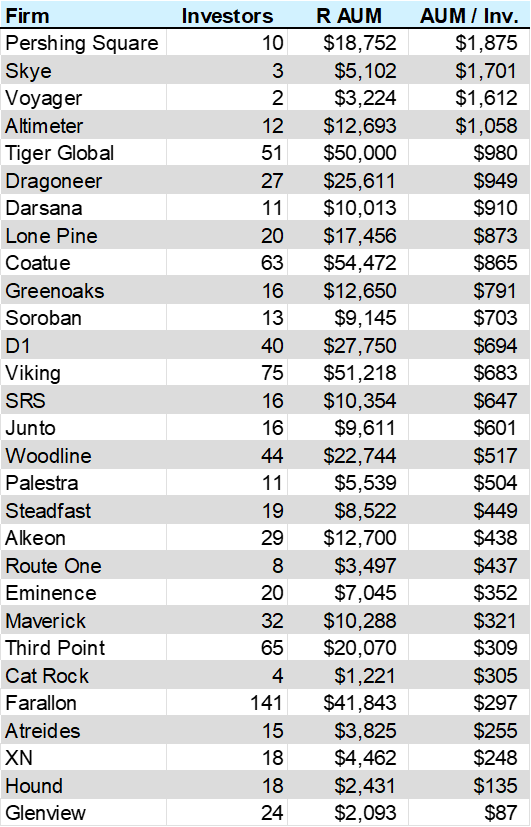

Would like to get a conversation going with some experienced monkeys about how to evaluate single manager hedge fund analyst job opportunities. Obviously there's only so much you can see from the outside but one frequently cited metric to look for is a high ratio of capital to investment professional implicitly translating to a lot of fees to go around. My question is, what are the limitations of this approach, and what are the limitations to information which could mislead? For example, I benchmarked a number of funds which are frequently discussed on this forum - the investor headcount stat is based on the disclosed number of employees in an investment advisory function and the R AUM is the regulatory assets under management as of the latest filing (generally 12/31/24 early 2025). Question one is, is this meaningful? Does leverage / mix of asset type (credit, equity, public/private) cloud it too much? Common sense would say Farallon is low because they're a diversified multi strat including in some more nascent strategies that probably are overweight headcount (credit) and / or have some more personnel-intensive strategies (RE). But would Xn's number, for instance, be a red flag relative to other funds with a similar strategy and asset mix like D1? Is performance in recent years (either return or sharpe) a better indication of a good seat? Would appreciate any perspectives (also curious if anyone is surprised by the numbers below). Apologies in advance if I fat fingered any numbers, I pulled this quickly.

Your AUM matters

11yr old account and 4 comments is crazy work

not that crazy

Yes absolutely. AUM is something of a meaningless figure because there are so many ways to calculate it, + it's a super dynamic number that changes day to day. Is it current cash? Is it the value of all holdings with leverage? without leverage?

Even regulatory AUM can be misleading. I've seen Balyasny's regulatory AUM go into the hundreds of billions, even though their stated AUM (at that time) was in the low-mid double-digit billions.

To answer your question, what makes a seat a good opportunity goes beyond what the headline numbers of a firm are. Culture, support, tech, leadership/role structure, and incentives all matter.

At single managers who don’t have pass throughs (and also usually don’t run massive back-leverage), AUM / head absolutely matters for total comp pool. ADVs use levered AUM so hyper levered fund structures are skewed. Also matters with how many products / strategies you run.

Can’t really use AUM / head to compare like a citadel seat with D1 but if you are comparing similar fund fee structures / leverage it absolutely matters how much a fund can pay. There is a reason why traditionally credit funds don’t really see massive paydays like equity funds do, they tend to run closer to $250-400m of AuM per investor given size of investment opportunities and complexity. even at scale and obviously returns are lower.

I can think of a couple single product non-tech focused investment partnerships that run > $2bn / head which even with lightened economics still would have an absurd comp pool.

Two thing to keep in mind as well is that different funds categorize investment professionals differently, e.g. Farallon number of 140 IPs looks pretty high. Additionally even for “2 and 20 / 1 and 20” single managers actual weighted avg fee structure can vary wildly.

No clue where they got 140. About half sounds right, seems like Wikipedia would agree.

per latest ADV

all 4 matter

With #4 mattering the most

this is the hardest to find out, no?

I had a few cases where I went though the whole process only to find out PM doesn't pay well, obviously felt a huge waste of time and energy... do you have any advice on how to figure out early in the process?

All four matter. But I’d flag your table has some clear errors.

Some of the AUM for a lot of these guys is for a single strategy (for example, privates only, private credit, real estate, etc). Put differently different amounts of AUM at different fees for different teams. It’s not all fungible. Of course many places manage various portfolios with one team.

All four matter. But I’d flag your table has some clear errors.

Some of the AUM for a lot of these guys is for a single strategy (for example, privates only, private credit, real estate, etc). Put differently different amounts of AUM at different fees for different teams. It’s not all fungible. Of course many places manage various portfolios with one team

One other factor is how much PM thinks you’ll make for him in future. It’s not all retrospective but also prospective. At a leaner place (like a lot of these even if very mis labeled due to various pockets of capital) the cost of attrition is very high for a strong performer who prints alpha $. Yes can you find someone to build a stupid model and pitch stuff; but no, can’t trust people that quickly, understand their style, their biases, their weaknesses — all of which you need to take into account in putting on / sizing an analyst position as a discretionary PM.

Fee-dollars-per-IP is ultimately what matters for the size of the bonus pool

AUM is one component of that, but so is strategy/mandate (expected return %) and very importantly FEE STRUCTURE. Many large SMs have the majority of their money in lower fee Long-Only vehicles. Some newer launches will have a large portion of the fund with a seed investor at discounted terms including a hurdle in many cases. Some capital may be first-loss vehicles. Founder capital doesn’t generate fees. Is it a management fee or a pass through?

Regardless none of this matters above a fairly low bar, because the actual compensation arrangement to the analyst / non-founder investment team is a fairly efficient market at the concentrated / low headcount shops tend to have a similar expected value of comp to the comparable pod role

Tiger in 2021 must have been a crazy experience. Peak aum (according to aum13f idk the validity) was about 120 bn.

Also crazy that their prize horse during that time JC is suing the firm - crazy times

I'd argue that it doesn't matter as much as people like to claim. What mostly matters is the split that founders are willing to give and how they want to structure compensation. Just because you are at a fund with $20bn and 10 IPs does not mean you are guaranteed to get a big part of the fee pool. When there is a ton to go around, sometimes they may chuck out some more money at everyone, but ultimately if its discretionary it stays that way...

Maybe only exception was legacy Tiger stuff pre 2022 when the numbers were so huge and everyone was doling out a lot I feel like. But if you are a 2+2 and its your first or second year, and the fee pool is like $100mn, you don't just get $1mn automatically for being there. You get a combo of your competitive rate in the market for taking this career path and just enough to keep you from killing yourself after you do the math on how much the founder keeps... The founder keeps as much as they can for the family trust and it'll always be that way

.

Ut iusto ducimus occaecati beatae voluptates impedit animi. Incidunt quidem autem dicta vero occaecati quam ducimus. Assumenda laborum nam et reiciendis qui eius quo. Et impedit officiis eum non ratione doloremque quo.

Inventore possimus quidem et quod ut rerum odit. Nulla et iste explicabo at aliquid ipsa nostrum. Excepturi maiores et error nobis quia. Totam quo eum esse qui. Odio dolorem unde est non atque saepe explicabo mollitia.

Optio doloremque debitis itaque deleniti molestiae delectus. Aut laborum sit voluptatum voluptatem sint sequi. Aut ipsum consequatur eos est quia in fugit. Omnis adipisci et dolorem dolorum quia. Nihil possimus ex quae nisi sed quasi. Dolorem et occaecati autem aut est.

Aut nihil esse perferendis qui. Nihil quia commodi voluptas facere. Omnis qui nulla unde omnis. Ea rem et asperiores. Blanditiis maxime temporibus beatae tempore aut quaerat a. Dolor aut non dicta ratione dolorum eum. Voluptas repellendus quae rem consequatur autem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...