Discussion: Deep Value or Value Trap? Analyzing the Institutional Rotation into "Distressed" Sectors

The spread between growth and value multiples has reached levels that historically precede a mean reversion. While the retail narrative remains fixated on AI capex and semiconductor earnings, institutional flow data suggests a quiet but significant rotation is underway beneath the surface.

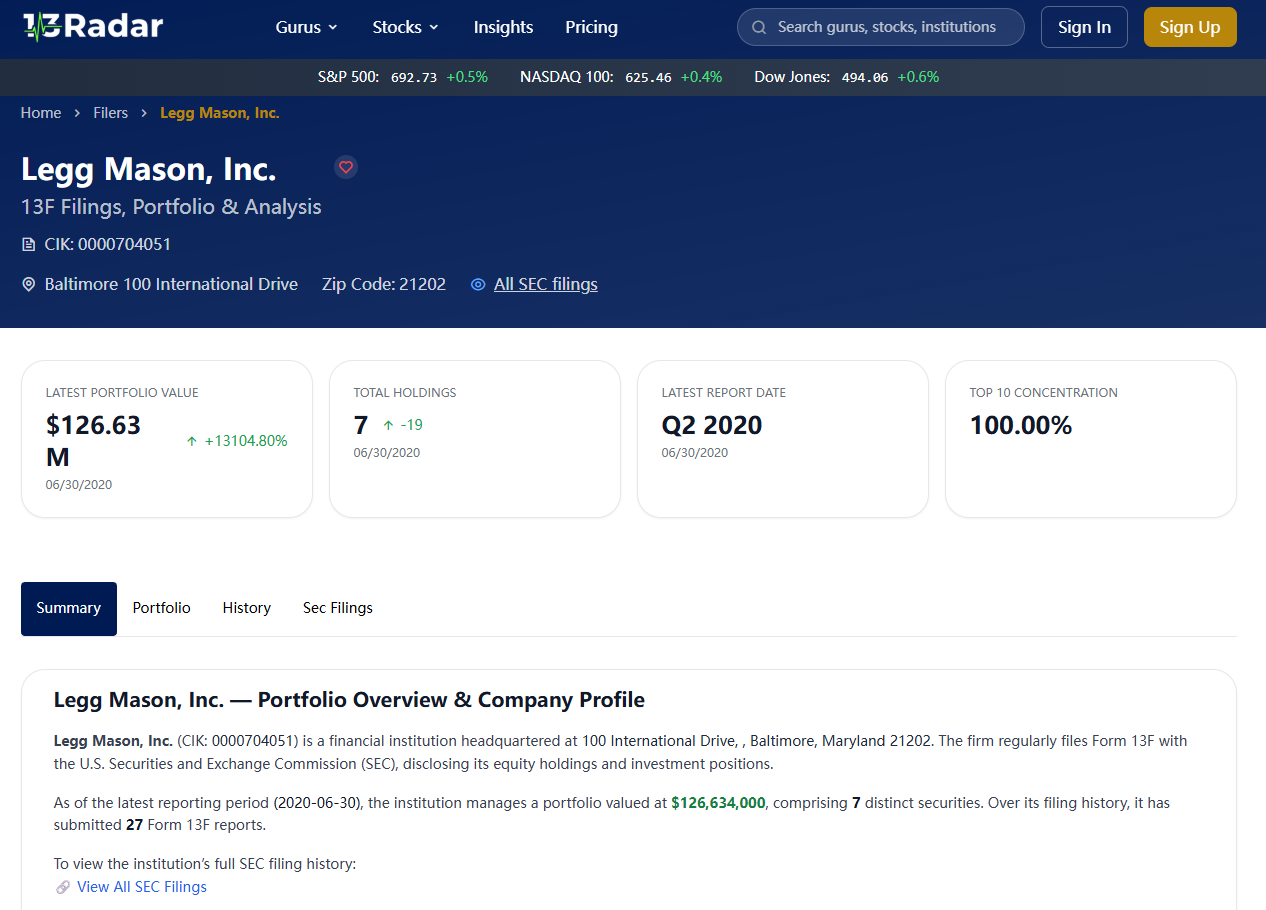

A granular look at the legg mason portfolio allocations reveals a distinctive shift in risk appetite. The smart money appears to be moving away from crowded momentum trades and positioning for "event-driven" catalysts in sectors that the broader market has effectively priced for bankruptcy. This raises a question for the forum: Is this a premature move into value traps, or are we seeing the early stages of a broad sector rotation?

1. The Arbitrage in "Sum of the Parts" (SOTP)

One of the more notable trends in the recent filings is the accumulation of shares in legacy conglomerates and media assets. The market is currently applying a massive "conglomerate discount" to these firms due to their complexity and lack of pure-play growth stories.

However, the institutional thesis seems to rely on corporate actions rather than organic growth. By acquiring assets where the breakup value (sum of the parts) significantly exceeds the current market cap, funds are effectively buying volatility-free options on potential spinoffs or restructuring events. In a high-rate environment, this balance sheet arbitrage offers a safer path to alpha than chasing P/E expansion.

2. Energy: FCF Yield vs. ESG Flows

Despite the prevailing ESG headwinds, the allocation towards Integrated Oil Majors remains stubborn. The financial logic appears to be driven purely by Free Cash Flow (FCF) Yield spreads.

While tech valuations imply perfection, the energy sector is trading at single-digit multiples while returning record capital to shareholders via buybacks. The bet here isn't on the price of oil going to $100, but rather on the sector's ability to act as a hedge against geopolitical tail risks and inflation stickiness. It is a defensive allocation disguised as a cyclical play.

3. Contrarian Positioning in REITs

Commercial Real Estate (CRE) sentiment is at an all-time low, yet there is selective buying activity in specific REIT sub-sectors, particularly Data Centers and Industrial Logistics.

The market has punished the entire asset class indiscriminately. However, looking at the cap rates relative to treasury yields, certain high-quality REITs are now trading at discounts to their Net Asset Value (NAV). The institutional accumulation here suggests a belief that the "rates higher for longer" narrative is fully priced in, and any stabilization in the yield curve could trigger a sharp re-rating in these hard assets.

Summary for discussion: Are you guys seeing similar flows in your coverage universes? Or is this rotation likely to get crushed if the soft landing narrative fails?

The discussion raises some compelling points about the current institutional rotation into sectors that are perceived as distressed or undervalued. Here's a breakdown of the key themes and considerations based on the most helpful WSO content:

1. Deep Value vs. Value Trap

2. Energy Sector Allocations

3. REITs and Commercial Real Estate

4. Institutional Rotation and Risk

Key Takeaways for the Forum:

Are others seeing similar trends in their coverage universes? Or are there additional sectors where institutional flows are signaling potential opportunities?

Sources: Q&A: HF Analyst @ $5bn+ Fund - Breaking In and Transition to Risk-Taking Role, Q&A: Emerging markets investment analyst, Long term, concentrated, deep fundamental investing, How do you feel about the current state of CRE?, Reflections from year 4 as an equity analyst

Dolores harum aperiam eum officia magni eos. Quas et nemo perspiciatis voluptate incidunt est.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...