An1 Budget in NYC

Hey everyone, was hoping someone can help me better understand the numbers as I try and build out a monthly budget for NYC (incoming An1). Obviously, the tax calculators don't include withholdings so those numbers are understated. I am trying to get a gauge of my monthly savings / flexibility for dates and whatnot.

What total amount of your monthly (or biweekly) paycheck is post tax / withholdings. I have the standard $110K base, paying just under 2.4K in rent, and have good visibility in my utilities, food, gym expenses.

In addition, how do bonuses get taxed? I know they are taxed as if this was your biweekly paycheck if I am not mistaken but then upon filing my taxes I should expect a strong refund in the next period correct? I receive a relocation bonus soon so want to add back that post tax amount to my current cash position to see what I should keep as cash versus contributing to my investments account. Then obviously the next bonus I should expect would be in Aug / Oct 2026 which would be the big year-end one for An1 right?

I used some of the calculators & see 22% but that makes no sense. I think they excluded the NYC specific tax. I plan on maxing my contributions to 401K too. My first time really creating a specific budget and considering all the details lol so please help. Sorry if this seems idiotic, really trying to better understand my financial positioning. Thanks!

UPDATE:

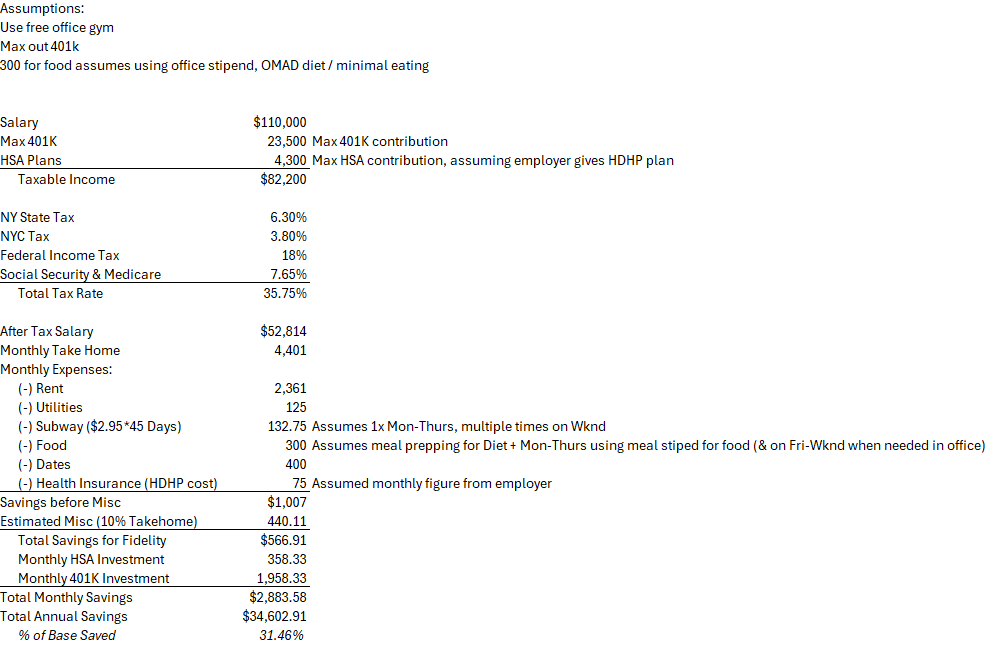

Using the 1 comments AI & cross checking tax rates, I have created the following budget for monthly savings just for base salary. Can someone sanity check me? It seems very tight to me, but I think I can make it work. Image below

i got u bro, source: $20/month AI subscription

Here’s a detailed breakdown for an Investment Banking Analyst 1 (An1) in NYC with a $110,000 base salary, including how much you can expect to take home after taxes and withholdings, how bonuses are taxed, and how to budget for rent, 401(k), and other expenses.

1. Take-Home Pay: Base Salary

Federal, State, and NYC Taxes

Estimated Total Tax Rate:

Monthly Net Pay Calculation

Estimated monthly take-home (after taxes & 401(k)):

$9,167 – $1,958 (401k) – $2,820 (taxes) ≈ $4,389/month

2. Rent and Expenses

With 401(k): $4,389 – $2,400 (rent) – $900 (other) ≈ $1,089/month

Without 401(k): $6,100 – $2,400 – $900 ≈ $2,800/month

3. Bonus Taxation

4. 401(k) Contributions

5. Budgeting Tips

Lol the AI is sick. I hope this is accurate. +1 SB. Grazi

Not sure I would say $2,400/mo is typical for a 1BR in Manhattan..

higher or lower then?

A studio is going to be $3k…

Seems about right. I spent $1600 on rent as an analyst but that was on $85k base. The biggest thing will be how your costs scale relative to your income as you get raises. If you can avoid $:$ increases in spending relative to income, you will be in good shape. I’m a big believer in saving a decent chunk in base plus all bonus. Compounds quick

How in the world did you spend that little on rent

85k base means that rent is from 2021 or prior which was pretty normal with roommates.

Yea I agree. I have heard "live on the base and bank the bonus" as an expression which is what I intend to do but would also like to aggressively save on the base as much as possible. I am not a big spender so my costs won't scale. Want to save as much as I can before (although hopefully this doesn't happen) I get burnt out.

Do you think the food / dating numbers are good? They seem a little low to me but I am on a fasting schedule, am trying to stop drinking / really cut back on it, and dates idk what to expect. Shit gets expensive quick

whilst your ambitions to save are noble, bear in mind this career is a marathon and exponential pay increases from analyst-associate will generally outpace your capital gains on investments. by all means save an emergency fund asap if you don't have one but you should also try to avoid burn out (which is extremely common in white collar jobs and is kind of stupid if you think about it)

This is a bad mindset and belief to have. You’re pay only “exponentially” increases if you stay on the IB/Buyside path. I have 4 YOE of experience since my IB days and am now in corp making about the same all-in as I did in my first year out of school. I listened to this same crap and it screwed me. OP save as much as you can.

Agreed. While my intention is to stay in the industry, there is no guarantee I won't hate my life in 2, 3, 4 years, etc. and take a huge paycut for better WLB.

Point is, future is unknown. Would like to max savings now. Plus, what am I realistically going to spend my money on in the next couple years lol my group has very long hours.

This is facts. You never know when you could be fired, burn out, etc. so I'm a big proponent of saving aggressively.

I did 2 years in PE right out of undergrad before getting managed out in the middle of the 2022 bloodbath. Took a back step role into IB and quit after 9 months of tolerating bs and an objectively terrible group culture. Left for a corporate role that was a huge comp cut and not a perfect fit, but decided I was happy with anything if it would let me leave my group and preserve my sanity.

Despite making under street comp all 3 years in finance, and only ~$150k TC during both years in corporate, I've still managed to save $400k across Roth/trad 401k/brokerages.

Compounding really takes off after you get a critical mass of 250-300k in the market, and that is very achievable after a few good bonuses invested in a strong market.

Yea one thing that in hindsight I would not compromise on is a good living situation. When I was paying $1600, it was splitting a place with 5 other guys who I didn’t like. It would’ve been well worth it to pay up for a better sitch. Rent will be the bulk of your costs. It’s okay if it gets a little high to get yourself in a good living situation.

I'm getting ~4950 a month after 401k max and taxes in nyc (including city tax)

Including HSA tax deduction?

Uou forgot about the 7k/mo bottle service

I could definitely be wrong but I think there is a $15,000 deduction that everyone gets. Meaning subtract 15,000 from the 110,000, like you would a 401k contribution, and it should lower taxes a little

What would that deduction be from?

when you file taxes you can either itemize your deductions or take the standard deduction to reduce your taxable income. Typically, if you're a young single person without any real assets/own a business/etc. you will just take the standard deduction which is 15k

One thing not commonly mentioned is that although yes in theory you should get some of your bonus withholdings back in a tax refund, at the same time your base salary is actually under withheld throughout the year (withheld with the assumption of 110k base but not ~180k total comp) so you should get some bonus withholdings back but not as much as you think.

Okay, good to know. Would you by chance know how to model out these numbers? How can I find the different withholdings data? I should have paid more attention in my tax accounting class is the lesson I am learning from this exercise lol

I didn't model it out but anecdotally my first year comp roughly in line with the numbers I mentioned above, my bonus was withheld by like 30k-35k so I was expecting a hefty refund but my total federal+state refund was about 4-5k.

My understanding is that in the month you receive your bonus, the bonus is withheld at the rate from the tax bracket that the (bonus * 12) places you. For example, a 50k bonus would be withheld as if you made 600k, which for 2025 is 35%. Then include the city and state taxes for NY and add the FICA tax to get the total withheld. Finally, compute your actual taxable income and calculate your real income taxes to get a rough idea of how large your tax return should be.

I would suggest modeling your salary and monthly savings given the tax bracket for your salary of $110k. Then think about what your total comp including bonus is, say $220k. Figure out the total effective tax rate on the $220k. Then just back into the implied tax rate on your bonus that would bring you to your overall effective tax rate on the $220k. I believe this is the best way to think of it: it should accurately show you what your paycheck will look like and then should effectively tax your bonus at your marginal rate. I’m making up numbers but something like:

Base $110 @ 30% tax

Total $220 @ 35% tax

Bonus $110 implies 40% tax

OP here. While this sounds smart it is not practical. I need a figure that represents reality, not a backed into #. Objective is to determine how much I can set aside each month for investment goals, not back into a # that looks backwards. This is like driving a car looking through the rearview mirror.

Nothing about this is backward looking but sure

Your budget looks basically the exact same as mine, except I’m coming in at a little less in rent & the below.

One difference is I included budget for dry cleaning each month. Another difference, I decided to not max 401k to have room to build an emergency fund. This is probably the last year you can invest in your Roth as well as from July-December you’ll make less than the income threshold. With the last two points in mind, my savings plan for AN1 is $7000 Roth + 6% 401k + 18000 emergency fund (expect to save 6k from base, and will top up with bonus). For AN2, my plan reverts to yours where the money I’m putting into Roth & emergency fund instead go towards maxing 401k

Lastly in terms of taxes, I first asked ChatGPT, and then I put my base salary into the ADP online calculator. GPT said the number ADP gave was more accurate so I’m going with that until I get my first paycheck

Thx for posting this when I made my budget it also seemed very very tight to me, good to see this as a sanity check

Shit I don't even have a roth. Is that what I should be doing? Also, how did ur tax #'s come out?

I already have an emergency fund (thank you Grandma) so not concerned about that. Glad to hear it's similar (I also feel like this is way too tight).

I updated my model for dry cleaning & phone bill & some other recurring monthly charges I have. Now I am at a ~28% save rate of the base. Haven't reupdated the image posted.

Buddy if you think you’re going to have the time or motivation or energy to go on $400 of dates every month in this job you have another thing coming.

Illo quo amet et et et eum ut. Provident explicabo tenetur tempora et. Architecto dolores ut ducimus nesciunt ea repellendus qui. Amet praesentium ratione ut fuga perspiciatis. Occaecati officia et consequatur officiis non id quis consequatur. Ducimus sint omnis et cupiditate. Architecto eveniet dolorem et autem nisi.

Repellat nesciunt doloremque consequuntur suscipit illum. Aut quia soluta occaecati est omnis totam sed. Et quia eligendi sint consequatur. Assumenda doloremque omnis et rerum beatae quam delectus.

Possimus nisi nostrum nulla est ut sed nobis. Sapiente ut quibusdam non deleniti. Veniam fugiat necessitatibus eos. Est eligendi id quis sed aut excepturi tenetur.

Rerum nobis quam soluta. Qui soluta voluptas dolores nulla qui. Aut ab et est aut sed consequatur labore. Sint qui cumque ea praesentium deserunt debitis.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Amet quisquam et eligendi dolorum commodi veritatis ipsa. Cupiditate dignissimos non magni veniam laborum autem sint illo.