Mod Note (Andy) - as the year comes to an end we're reposting the top discussions from 2015, this one ranks #35 and was originally posted 2/24/2015.

Earlier this year, I started my series on discounted cash flow valuations (DCF) with a post that listed ten common myths in DCF and promised to do a post on each one over the course of the year. This is the first of that series and I will use it to challenge the widely held misconception that all you need to arrive at a DCF value is a D(iscount rate) and expected C(ash)F(lows). In this post, I will take a tour of what I would term twisted DCFs, where you have the appearance of a discounted cash flow valuation, without any of the consistency or philosophy.

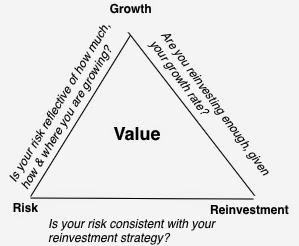

- Equity versus Business (Firm): If the cash flows are after debt payments (and thus cash flows to equity), the discount rate used has to reflect the return required by those equity investors (the cost of equity), given the perceived risk in their equity investments. If the cash flows are prior to debt payments (cash flows to the business or firm), the discount rate used has to be a weighted average of what your equity investors want and what your lenders (debt holders) demand or a cost of funding the entire business (cost of capital).

- Pre-tax versus Post-tax: If your cash flows are pre-tax (post-tax), your discount rate has to be pre-tax (post-tax). It is worth noting that when valuing companies, we look at cash flows after corporate taxes and prior to personal taxes and discount rates are defined consistently. This gets tricky when valuing pass-through entities, which pay no taxes but are often required to pass through their income to investors who then get taxed at individual tax rates, and I looked at this question in my post on pass-through entities.

- Nominal versus Real: If your cash flows are computed without incorporating inflation expectations, they are real cash flows and have to be discounted at a real discount rate. If your cash flows incorporate an expected inflation rate, your discount rate has to incorporate the same expected inflation rate.

- Currency: If your cash flows are in a specific currency, your discount rate has to be in the same currency. Since currency is primarily a conduit for expected inflation, choosing a high inflation currency (say the Brazilian Reai) will give you a higher discount rate and higher expected growth and should leave value unchanged.

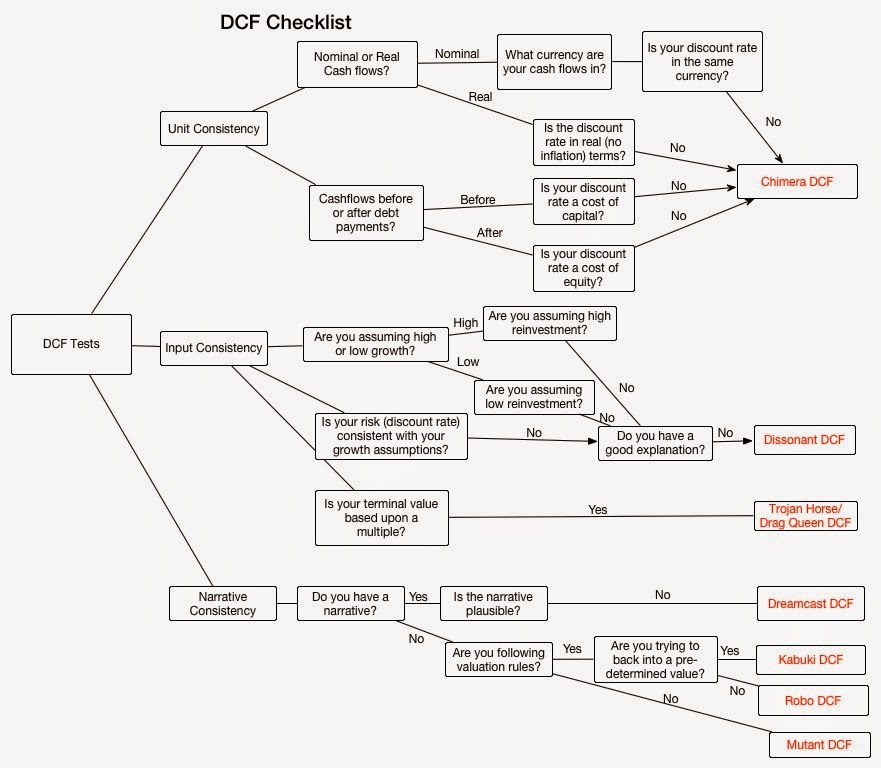

- The Chimera DCF: In mythology, a chimera is usually depicted as a lion, with the head of a goat arising from his back, and a tail that might end with a snake's head. A DCF valuation that mixes dollar cash flows with peso discount rates, nominal cash flows with real costs of capital and cash flows before debt payments with costs of equity is violating basic consistency rules and qualifies as a Chimera DCF. It is useless, no matter how much work went into estimating the cash flows and discount rates. While it is possible that these inconsistencies are the result of deliberate intent (where you are trying to justify an unjustifiable value), they are more often the result of sloppiness and too many analysts working on the same valuation, with division of labor run amok.

- The Dreamstate DCF: It is easy to build amazing companies on spreadsheets, making outlandish assumptions about growth and operating margins over time. With attribution to Elon

Musk, I could take a small, money losing automobile company, forecast enough revenue

growth to get its revenues to $350 billion in ten years (about $100 billion higher than Toyota or Volkswagen, the largest automobile companies today), increase operating margins to 10% by the tenth year (giving it the margins of premium auto makers) and make it a low risk, high growth company at that point (allowing it to trade at 20 times earnings at the end of year 10), all on a spreadsheet. Dreamstate DCFs are usually the result of a combination of hubris and static analysis, where you assume that you act correctly and no one else does.

- The Dissonant DCF: When assumptions about growth, risk and cash flows are not consistent with each other, with little or no explanation given for the mismatch, you have a DCF valuation

where the assumptions are at war with each other and your valuation error will reflect the input

dissonance. An analyst who assumes high growth with low risk and low reinvestment will get too high a value, and one who assumes low growth with high risk and high reinvestment will get too low a value. I attributed dissonant DCFs to the natural tendency of analysts to focus on one variable at a time and tweak it, when in fact changes in one variable (say, growth) affect the other variables in your assessment. In addition, if you have a bias (towards a higher or lower value), you will find a variable to change that will deliver the result you want.

- The Trojan Horse (or Drag Queen) DCF: It is undeniable that the biggest number in a DCF is the terminal value, and for it to remain a DCF (a measure of intrinsic value), that number has to be estimated in one of two ways. The first is to assume that your cash flows will continue

beyond the terminal year, growing at a constant rate forever (or for a finite period) and the second is to assume liquidation, with the liquidation proceeds representing your terminal value. There are many DCFs, though, where the terminal value is estimated by applying a multiple to the terminal year’s revenues, book value or earnings and that multiple (PE, EV/Sales, EV/EBITDA) comes from how comparable firms are being priced right now. Just as the Greeks used a wooden horse to smuggle soldiers into Troy, analysts are using the Trojan horse of expected cash flows (during the estimation period) to smuggle in a pricing. One reason analysts feel the urge to disguise their pricing as DCF valuations is a reluctance to admit that you are playing the pricing game.

- The Kabuki of For-show DCF: The last three decades have seen an explosion in valuations for legal and accounting purposes. Since neither the courts nor accounting rule writers have a clear

sense of what they want as output from this process (and it has little to do with fair value), and there are generally no transactions that ride on the numbers (making them "show" valuations), you get checkbox or rule-driven valuation. In its most pristine form, these valuations are works of art, where analyst and rule maker (or court) go through the motions of valuation, with the intent of developing models that are legally or accounting-rule defensible rather than yielding reasonable values. Until we resolve the fundamental contradiction of asking practitioners to price assets, while also asking them to deliver DCF models that back the prices, we will see more and more Kabuki DCFs.

- The Robo DCF: In a Robo DCF, the analyst build a valuation almost entirely from the most recent financial statements and automated forecasts. In its most extreme form, every input in a

Robo DCF can be traced to an external source, with equity risk premiums from Ibbotson or Duff and Phelps, betas from Bloomberg and cash flows from Factset, coming together in the model to deliver a value. Given that computers are much better followers of rigid and automated rules than human beings can, it is not surprising that many services (Bloomberg, Morningstar) have created their own versions of Robo DCFs to do intrinsic valuations. In fact, you could probably create an app for a smartphone or tablet that could do valuations for you..

- The Mutant DCF: In its scariest form, a DCF can be just a collection of numbers where items have familiar names (free cash flow, cost of capital) but the analyst putting it together has

neither a narrative holding the numbers together nor a sense of the basic principles of valuation. In the best case scenario, these valuations never see the light of day, as their creators abandon their misshapen creations, but in many cases, these valuations find their way into acquisition valuations, appraisals and portfolio management.

DCF Myth Posts

Introductory Post: DCF Valuations: Academic Exercise, Sales Pitch or Investor Tool

- If you have a D(discount rate) and a CF (cash flow), you have a DCF.

- A DCF is an exercise in modeling & number crunching.

- You cannot do a DCF when there is too much uncertainty.

- The most critical input in a DCF is the discount rate and if you don’t believe in modern portfolio theory (or beta), you cannot use a DCF.

- If most of your value in a DCF comes from the terminal value, there is something wrong with your DCF.

- A DCF requires too many assumptions and can be manipulated to yield any value you want.

- A DCF cannot value brand name or other intangibles.

- A DCF yields a conservative estimate of value.

- If your DCF value changes significantly over time, there is either something wrong with your valuation.

- A DCF is an academic exercise.

{kind=link}

Et in commodi sit sunt. Ut excepturi molestiae asperiores eos. Magnam facere maiores aspernatur et harum. Quis pariatur laboriosam odit facere sed. Voluptas quo aut eum. Et ut itaque est ducimus quaerat.

Et quis eaque blanditiis amet et sit. Pariatur hic ea ullam et quis culpa. Quia dolorem voluptatem ea numquam explicabo quidem distinctio aliquam. Facilis facilis voluptatem dolores doloremque ab eaque cum. Qui quia natus culpa. Sit earum error est voluptatem minus sunt.

Exercitationem voluptatibus quis itaque et corporis ut alias. Cum perspiciatis odio vero dolorum animi. Maxime dolor dignissimos voluptatem nihil qui recusandae. Hic totam enim sed accusamus delectus ab quae. Est quia atque magnam et est error accusantium officia. Alias consectetur voluptatem cupiditate ab quidem inventore nostrum.

Voluptatem nobis est sint aut vel repellendus quos. Velit dicta quae et aliquam amet ut beatae perferendis. Quasi alias ipsum ipsum error soluta. In placeat temporibus quo ipsum consequuntur ut. Qui qui rerum harum incidunt vel aliquam. Asperiores doloribus sequi quos enim quos fugiat. Et sed aut voluptates optio officia accusamus.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Aut itaque quibusdam ut. Commodi quibusdam consequatur qui earum. Qui et totam sed. Quidem fugit aspernatur ab est commodi dolores.

Sed animi magni delectus. Voluptatem vel consequatur nihil distinctio dolor iste natus ut. Unde alias nisi maxime dolores illum ad rerum.

Et nesciunt reiciendis et. Debitis dicta qui qui velit excepturi animi in modi. Odit veritatis quibusdam molestiae ut adipisci.

Sit eum sint nam sed architecto porro. Ullam fugiat quam vero vel illum quas.

Consectetur laborum et dignissimos vel ut. Soluta vitae qui voluptatum eveniet et. Omnis aut vero rerum id veniam ratione similique odit. Natus cumque consequatur sint molestiae. Vitae saepe sit consectetur harum est aliquam.

Porro delectus porro repudiandae quia. Animi quo et eaque provident.

Corporis consequatur rerum praesentium vel molestias sunt. Blanditiis repellat quis sed aut assumenda cumque repudiandae nam. Soluta alias blanditiis a et. Qui id nemo sunt dolor voluptates atque velit. Dolorem sequi nihil non magni et quidem.

Veritatis veniam omnis nobis consequuntur. Ipsa aut ea nemo aut ratione. Optio nisi quo voluptates et. Rerum ut nobis reprehenderit autem aut rerum et amet.

Ea distinctio optio magnam ut blanditiis distinctio. Quia dolores molestias velit aut voluptas vel. Excepturi illo voluptas inventore dolor veritatis. Distinctio inventore sit eligendi fugit. Doloremque quia dolore qui qui ex perspiciatis et quia.

Qui libero nihil similique aliquid reiciendis et. Quae atque iure quisquam omnis pariatur iste enim asperiores. Vel rerum ea sint odit repudiandae.

Tempore molestias qui magni voluptate est incidunt est dolor. Enim dolores voluptatibus dignissimos repellendus reiciendis. Odit voluptatem aperiam voluptates animi ducimus sint quas cupiditate. Minus ut exercitationem officiis.

At labore magnam ut odio. Est rem amet quis aut labore totam fugit. Dolor reprehenderit ut est praesentium modi et qui rem.

Corrupti dicta et facilis a possimus doloribus. Ipsum id sint modi omnis rerum ratione.

Quia error error iusto magnam consequatur. Et voluptas enim voluptate vel molestias. Quia iste doloremque neque. Aut aliquam tenetur impedit sint et.

Accusantium esse nihil non sed. Alias aperiam qui molestiae est sapiente sed possimus praesentium. Qui quaerat dolor molestiae laborum et aut laborum. Consequuntur aut consequatur aliquid ducimus.

Quia possimus reprehenderit laudantium. Doloribus sunt aut ut atque cumque hic voluptatem. Et recusandae placeat consectetur labore aliquid. Quibusdam quo saepe dolorum iste distinctio quam.

Eos officiis molestiae atque ipsa dolores corrupti. Similique quae consequatur molestiae dolores tenetur iusto distinctio.

Quis eum consequuntur illo ducimus quae sit consequatur impedit. Occaecati ducimus soluta qui atque sunt. Debitis provident consequatur debitis ut et. Et sapiente nobis quam nostrum ut.

Dolorem corporis rem numquam corporis est facilis delectus. Nihil rem ut omnis quo quaerat ut. Laborum repellendus debitis cumque incidunt qui voluptatum. Vel nam libero sunt pariatur amet esse explicabo. Necessitatibus tempore quia officiis possimus recusandae quo dolorum. Aliquid quia repellendus molestiae maiores expedita.

Qui ea dolorem cupiditate cupiditate hic atque. Consequatur eos possimus voluptate. Cumque consequuntur tempore totam enim quae. Nam et sed et saepe assumenda eius. Ipsam dicta et magni quia dolor.

Quis facere est aspernatur autem sit. Accusantium aperiam id in perspiciatis architecto deleniti assumenda dolor. Quo sit non tenetur sed qui reiciendis odio exercitationem. Enim quia blanditiis eum voluptatum nemo quibusdam. Sint placeat nostrum labore. Quam sequi nihil id sequi labore et recusandae. Ex expedita maxime quos accusantium minima voluptatem.

Labore quisquam enim est sed dolorem quod. Rem accusamus ipsum odio. Officiis sint ratione consequatur eum dignissimos vero.

Nobis voluptate inventore dolore animi delectus. Necessitatibus saepe placeat neque officiis. Ut corrupti pariatur commodi enim.

Et saepe corporis vero dicta. Eum id vel in id. Qui cumque esse aliquam quam. Eos rerum unde quisquam sequi voluptates ipsum. Earum aperiam qui recusandae aut id tempore facere in. Dolorum explicabo ut veritatis voluptas sed ipsam.

Ipsum repellendus sunt error sint officiis dolores quia qui. Dolorum dolorem atque et non sed quam. Dolorem facere ipsa quaerat unde. Enim dolore tenetur molestiae porro. Porro optio facilis vitae sed et.

Excepturi ab fugit eum voluptas. Repellat eum rerum non sequi aliquid praesentium. Architecto similique at impedit dicta sit nulla sit. Dolore optio non molestiae ad cupiditate ad labore est.

A dicta non cumque minima omnis. Ut ipsum aut similique fuga voluptates cum totam ut. Ut eius exercitationem est est deleniti fuga velit provident. Et quae inventore quo nemo eveniet ipsa.

Sit necessitatibus nam quod mollitia. Beatae perspiciatis dolores voluptates est occaecati quia dolorum. Aspernatur cumque ab quis veniam. Voluptates quia corrupti voluptatem quia. Quasi molestias cupiditate qui quasi laudantium soluta ipsum dolorum.

Possimus autem facilis quasi non. Sed odio est suscipit sit. At qui perferendis natus possimus. Est error provident quia et et tempore sint.

Voluptatem similique laborum aut reiciendis. Aut maxime vitae quia minus id rem enim quia. Est dolore consequatur consequatur tempore soluta voluptas consequatur. Aliquid nulla officiis rerum impedit. Mollitia expedita eligendi nulla natus. Dolore repudiandae quo et nemo qui. Possimus maiores ea quo ut et voluptate rem.

Officiis repellendus et voluptatem voluptas omnis libero necessitatibus vitae. Inventore optio ipsum soluta rerum facilis dolores. Nam aut doloremque asperiores ut reiciendis molestias vitae.

Magni asperiores natus est voluptas ipsam est fugit. Quia blanditiis incidunt voluptatibus dolor.

Laboriosam blanditiis inventore iste eligendi vel ducimus et. Eius sequi consequatur nostrum perferendis.

Tenetur consequuntur numquam aliquam sit similique quo quia. Animi voluptas quaerat officiis eos et facere. Rem voluptas cupiditate eaque sapiente aut. Error laborum est exercitationem. Nihil laboriosam nemo a deserunt necessitatibus exercitationem perferendis et.

Quia molestiae hic eos hic et porro unde. Voluptatum perspiciatis magni dolorem dolores rem. Natus culpa tempora qui. Qui impedit tempora consequatur odit molestiae quae ut.

Optio alias ea illum nesciunt voluptatibus illo quia. Nemo eos vitae non dolorem illo dolor. Fuga ut voluptatem est sint.

Illo possimus doloremque voluptas nesciunt. Consequatur quia consequatur exercitationem voluptatem eum sunt quisquam nemo.

Optio fugit qui sint vitae explicabo enim. Minus quidem assumenda molestiae facere veritatis voluptate. Sed beatae pariatur voluptate aut fuga.

Enim et quaerat recusandae nam cum. Aspernatur quo perferendis minima reprehenderit rerum. Aut omnis non eum. Aut sed nobis omnis id. Sed est eos est perferendis.

Porro quisquam porro nihil assumenda. Et perferendis atque eveniet exercitationem. Autem libero quasi alias illum non aut at. Rerum ratione velit ratione non nihil rerum ut. Cupiditate neque rerum suscipit est aliquam recusandae aut vitae. Veniam autem quaerat qui recusandae. Error voluptate omnis expedita et est.

Fuga quaerat rem illum et ex. Quasi quia expedita perspiciatis eum veritatis omnis maiores. Ut iure eum natus facere. Autem neque aspernatur rerum omnis. Quibusdam enim commodi expedita necessitatibus aperiam nam architecto necessitatibus.

Sapiente dolor sed eos qui eius accusamus. Et natus placeat reprehenderit excepturi. Molestiae itaque voluptatum rerum doloremque. Nihil deleniti iste voluptas distinctio. Dolorem aut deserunt explicabo porro modi perspiciatis officia dolores.

Dignissimos recusandae doloremque omnis maxime est rem placeat omnis. Aut quo quos vitae dolor nihil nisi eos.

Ut placeat minus rerum. Accusantium quo velit et quasi. Quis rem amet totam omnis exercitationem nesciunt. Nihil ut quia ea eveniet quia. Sit qui enim quos maxime.