PE in a crisis: lessons learned

The PE industry is showing signs of recovery after 3 or so years in the doldrums. See below for a few slides I presented last night that 1) highlight the disconnect in private and public markets in recent times, and 2) provide a view on US government policy relative to global LBO activity over the last 25 years.

Main takeaways: AI has caught a bid, while the rest of public and private markets have not. And: we probably should have seen inflation coming. If there was ever a time for discipline and stronger risk management in PE, it would have been to quell animal spirits in '21 & '22. See below each picture for additional commentary.

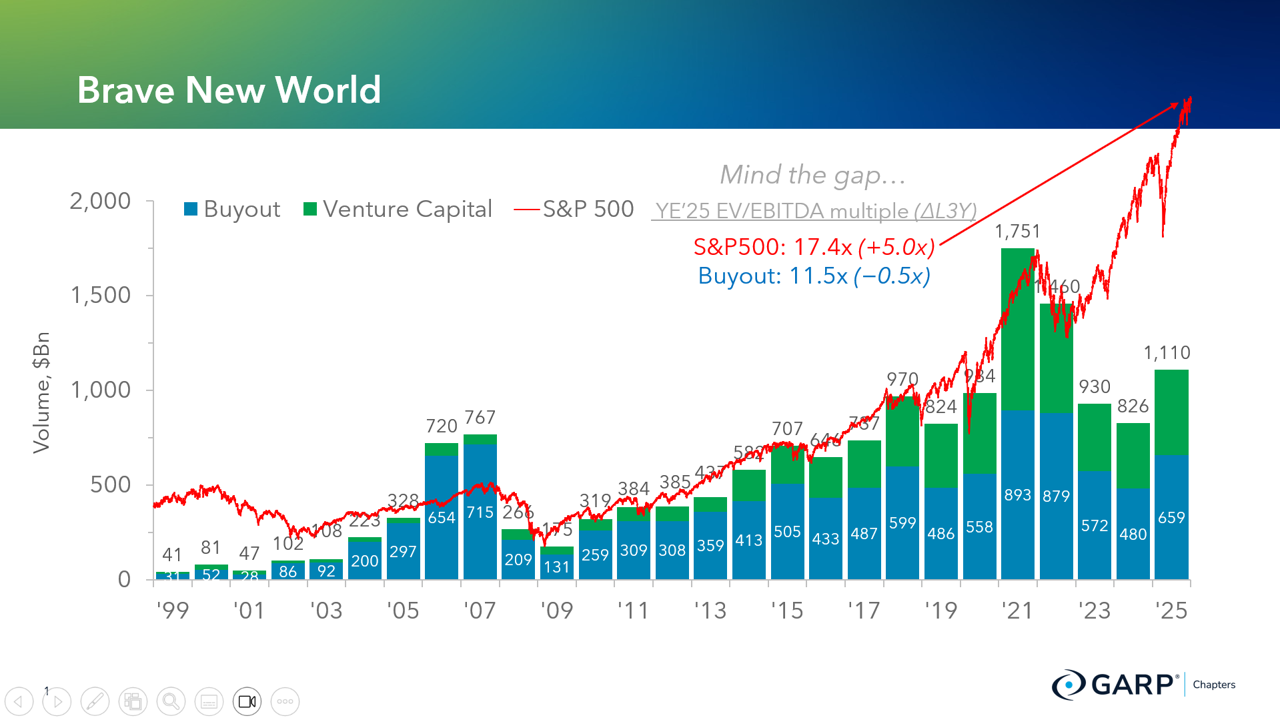

This chart overlays the S&P 500 on annual industry-wide LBO deployment since 1999. What is interesting is the divergence over the last 4 years, following a bull run in both public and private markets since the GFC. I included actual EV/EBITDA metrics for reference. AI and interest rates levels are plausible explanations for the deviation... which certainly can't last forever. Which leads me to my favorite chart from last night's session -->

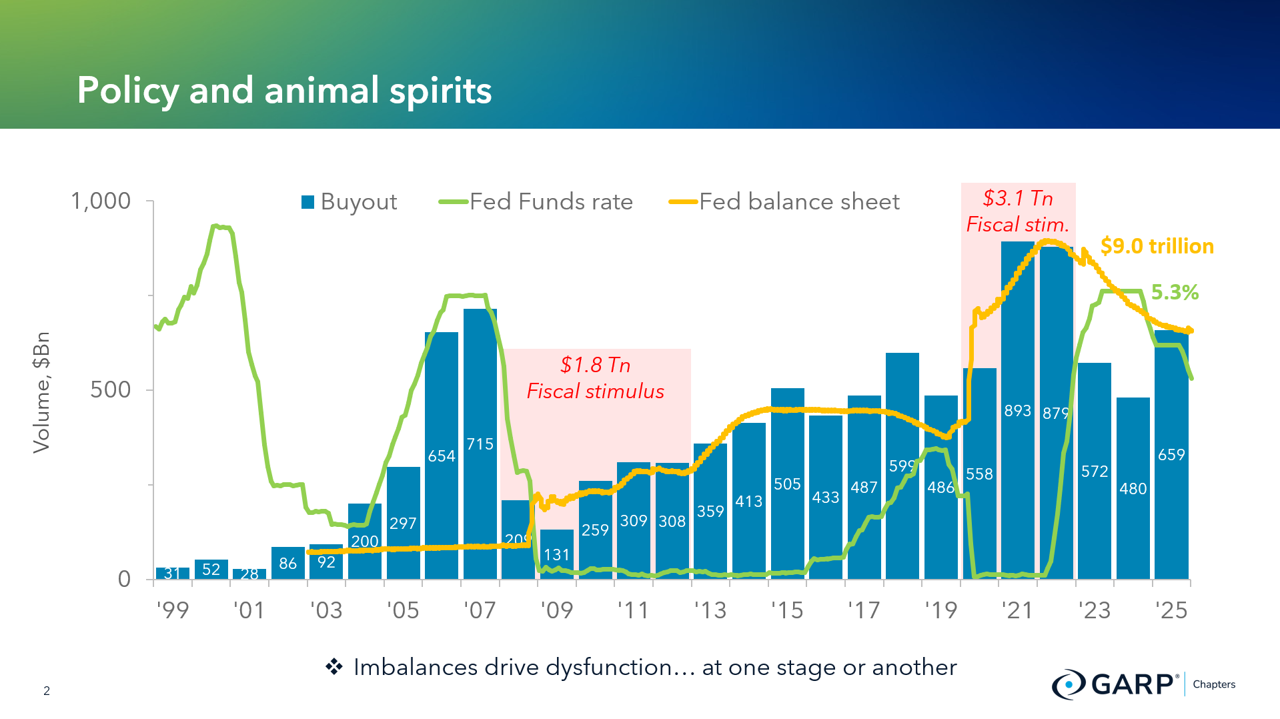

Looking at the chart above, you can consider US monetary policy in an accommodative position anytime the orange line is above the green line... and the wider the gap, the more accomodative. The orange line reflects quantitative easing (i.e., the purchase of private loans by the Federal Reserve) while the green line is the Fed Funds rate.

Looking at the chart above, you can consider US monetary policy in an accommodative position anytime the orange line is above the green line... and the wider the gap, the more accomodative. The orange line reflects quantitative easing (i.e., the purchase of private loans by the Federal Reserve) while the green line is the Fed Funds rate.

When coupled with fiscal stimulus, it seems unsurprising that 1) PE firms went set new highs in annual deployment in '21 and '22, as the world was awash in cheap liquidity, and 2) inflation followed shortly thereafter. Note, the fiscal stimulus shown in the graph is above average growth in fiscal spending at any point over the last few decades... so the figures shown on the graph are on top of what we would see in "normal" US government spending.

Autem sed ea et aliquam reiciendis. Quia quam ducimus ipsam deleniti minus tempore. Maiores non est itaque ut aperiam et doloribus.

Assumenda aliquam eveniet vero non deserunt voluptates. Eum dicta architecto voluptatem quam perferendis aut eos. Animi numquam voluptas voluptas natus repellendus aspernatur eos. Nihil saepe saepe provident animi aut. Ut accusamus dolores voluptas itaque rerum autem quis.

Maxime aperiam sed nostrum libero. Optio unde tempora eligendi sint quidem laborum et. Quam fugit voluptatibus nulla culpa quibusdam suscipit nulla delectus.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...