Let's Debate Multifamily Modeling

Hey all - I'm in search of some best practices and hopefully some consensus when it comes to multifamily modeling.

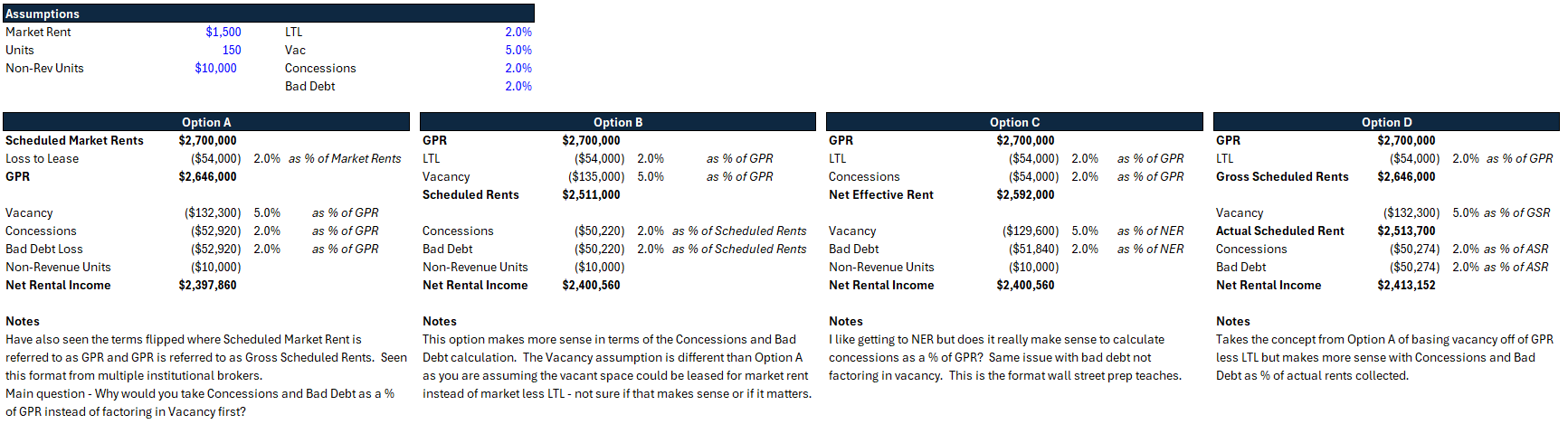

A bit of background, I have spent most of my career in hotels but am pivoting to a generalist role. As such, I'm in the process of building out a fairly robust multi model. I have found the inconsistency in how people model multifamily properties to be frustrating and am looking to get a clearer picture of what this group thinks are best practices and why. My issue is that the variations in how different groups model MF cashflow (some of which seem conceptually unsound) have left me with analysis paralysis. None of this could actually matter in practice but would at least like to understand the why a bit better from the multi experts.

I have included a photo of what seem to be the most logical options/prevalent in institutional investment and my notes on each. Would love to hear everyone's thoughts or how your firm does things. If there's a way to attach an excel file, I can do that as well just don't know how.

Based on the most helpful WSO content, here are some best practices and insights for multifamily modeling:

Key Considerations in Multifamily Modeling:

Cash Flow Modeling:

Risk Assessment:

Model Sophistication:

Presentation and Justification:

Practical Tips:

Community Insights:

By following these best practices and leveraging community insights, you can build a robust and reliable multifamily model that helps you make informed investment decisions.

Sources: Lunch & Learn -Ins and Outs of Multifamily, Multifamily Developers and Acquirers: What do you look for in property management firms?, Real Estate Development Modeling, Life in Acquisitions (Analyst/Associate), How to Convince My Boss to Include Excel Modeling Into the Job?

It’s all really semantics. There is no right answer. And as you can see 3 of the 4 methods land around 2.4M. And the $3K difference isn’t going to make a difference in your deal.

Option 4 is the only one where I actually disagreed. Reason being concessions should be based on gross rent - as that is rent at market. And concessions should be based on market rent. Loss to lease is to deal with the fact that you may have rents continually increasing each month, but a lease you signed 10 months ago is still at the same rate. Therefore you have a loss due to a lease.

Thanks - I feared I would be told there's no right answer - unsatisfying for sure. I feel like we can at least find a most logical method. My rebuttal to your second point would be that you're only giving concessions on occupied units, so it would make more sense to deduct vacancy first. Bad debt would follow the same logic - you can't have credit loss on vacant units. I get your point on LTL, but if you have a unit with market rent at $1,600 but the property manager leases it at $1,500 and gives one month free rent, that concession would be based on the $1,500, not the market rent.

We're currently working on some adjustments for this (London based BTR / Multifamily shop working with Top US LP (bank, fund...))

My 2 cents and how our model (inherited from a major US bank AM arm):

ERV = Market rent trended (takes into account economic growth and capex uplift %, when we complete value-add capex we say ERVs go +x%)

Loss to lease = (GPR - ERV)

GPR = Contracted Rent

- Concessions

- Vacancy Loss

= Residential Rent Received

Then comes ancillary, parking, bad debt to give you your net before diving into OPEX

My point is: Loss to lease should not be an assumption as it is an output

On void / vacancy: We have a general void % assumption (call it 97% for stab. BTR) and it makes sense to apply this to GPR - what I've recently worked on to give a clear picture of income available to service debt is to get to a dynamic void calcs with the following:

Vacancy % = 1-Void %

Void % = Expiries * Churn Rate * Void days / total days in the month

-> Void days (Your AM guy or PM tells you how long on average a unit stays empty during this month - 20 in July, 10 in Dec... and you index/match to this)

-> total days in the month = number of units * number of days in that month

Appreciate the detailed reply. I get what you're saying on LTL being the output, not the input. From a projection standpoint, it's much easier to make it the input. Say my current market rent is $1,600 and in-place rent is $1,500, so in-place LTL is 6.3%. I would model 6.3% going in and reduce the LTL % in a year if marking rents to market was part of the business plan. But agreed on modeling in the rent growth and capex lift to ERV. Are you modeling concessions and vacancy as a percentage of GPR?

To each their own but this feels like overkill. It doesn’t really matter if loss to lease is an input or output - you get to the same level.

And frankly - my model is always wrong. So never really need to ‘fine tune’ it. Just make sure it’s pretty damn close.

Jesús Christ get a hobby

Helpful! I will let Jesus Christ know that you would like him to get a hobby.

For reference, this is how ARGUS does it:

Potential Market Rent (PMR)

- LTL

Potential Rent (PR)

- Vacancy (% of PR)

Scheduled Multifamily Rent (SMR)

- Concessions (% of SMR)

- Credit Loss (% of SMR)

Effective Multifamily Rental Income

If you are using Argus for multifamily you need a hobby

Required at a top lifeCo — Allianz, PGIM, MetLife, Nuveen

I like

GPR

- LTL

- Vacancy

- Bad Debt

- Concessions

- Non Rev Units

- Other Revenue Loss

Net Effective Rent

- Utility Reimbursement

- Other Income

Effective Gross Income

Here is what I am thinking about:

For Retail and Office building, you may look for the Argus Enterprise, to see the spreadsheet result generated by this weird software.

For multi, you may start with Market rent first,

then the loss to lease, Potential rental income.

Vacancy , Concession, credit loss. Ex. If vacancy is 5% of Potential rental income, concession (2%) should be 2% * (1-5%)*Potential rental income to avoid double counting. Then you adding your other income to get the effective gross income.

But actually you are right, different big shops have different underwriting practices. So it just depends on your assumptions and justification.

Hope it can help you .

My model goes:

Base Rental Income

Renovation Premium

Less Loss to Lease (% of Base Rental Income)

Gross Potential Income (GPI)

Vacancy (% of Base Rental Income + Reno Inc ) (Does not include LTL)

Credit Loss (% of GPI less Vacancy)

Concessions (% of GPI less Vacancy)

Non income units (% of GPI less Vacancy)

Base Rental Income

Other Income

Effective Gross Income

Expenses

NOI

Et quia distinctio ut voluptatem velit. Rem aperiam odit voluptatem illum dolore culpa. Id ea eos tenetur voluptate perferendis culpa occaecati voluptatem. Labore praesentium doloremque et dolorem eligendi provident. Impedit similique dolor earum quia.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...