Syndicators - The hidden and not so hidden ways they make their money(?) help me figure this out

Hey guys,

First and foremost, I am a multifamily developer and as someone who builds ground up construction, I've always envied a lot of the acquisitions guys and feel like they don't add a ton of value. These guys have been raking in the money the last 10 years, growing to thousands of units, and exiting for large sums of money, while us developers may only get a handful of projects done during that time.

Also, the typical pref structure has the LP's leaving with 75% of the profits at a sale, so I always assumed these guys would front load the fees or maybe sale an asset to a fund, which I'm guessing is what these guys did.

Now, I'm trying to figure out how one group makes their money. I don't want to single these guys out, but help me figure out what's going on.

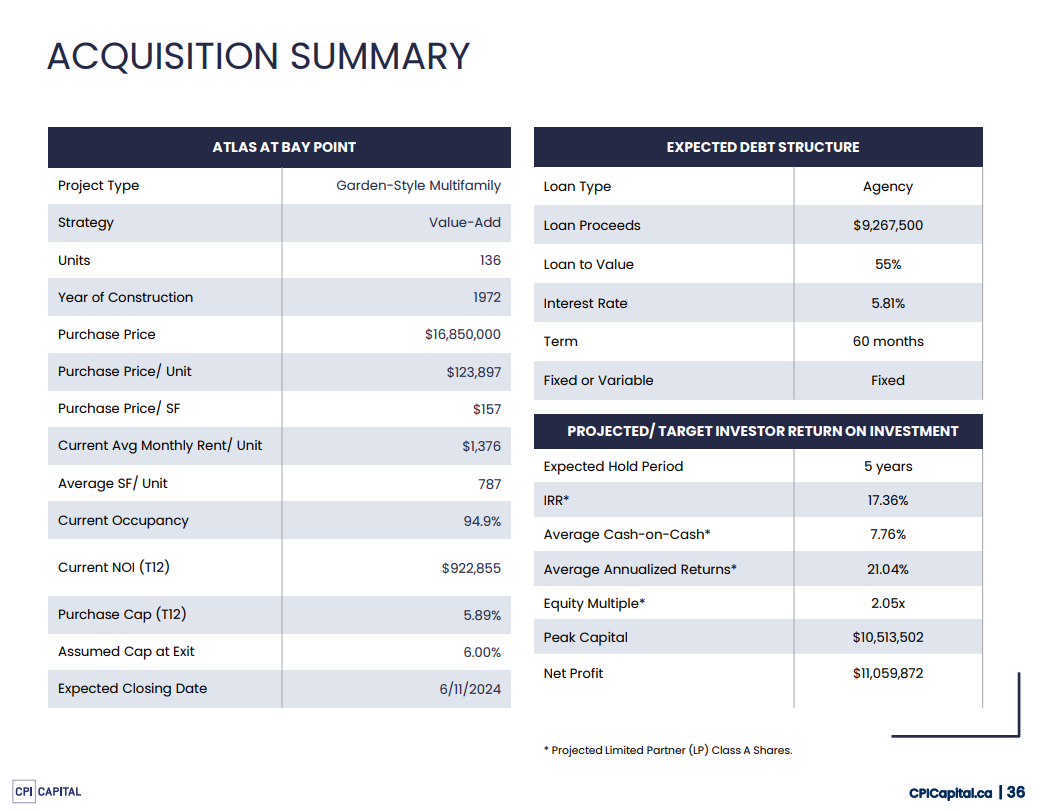

Atlay at Bay Point 136 units purchased for $12.34M, 1972 Build. https://stpeterising.com/home/done-deals-st-pete-apartments-undergo-rebrand-new-york-company-relocates-hq-to-pinellas-indian-rocks-beach-restaurant-sells

Here is another website backing up the purchase price. https://traded.co/deals/florida/multifamily/sale/2150-62nd-terrace-south/

Sale Price $12.34M and they took out a loan of $9.267M

But according to their website, it's a completely different story. https://cpicapital.cpicapital.ca/atlas-at-bay-point

Financial Analysis: http://8021107.fs1.hubspotusercontent-na1.net/hubfs/8021107/2%20Atlas%20at%20Bay%20Point%20Apartments/Financial%20Analysis.pdf

Purchase price of $16,850,000. Then a financing fee of $92,675. Then an acquisition fee of $337,000. Closing costs of $421,250.

So they potentially walked away with $5,360,925 before even executing a game plan.

They raised LP equity of $9,462,152 and "$1,051,350" of GP Equity. and if they executed and performed, a 2.05 Equity multiple would yield the investors $19,397,411. Using the debt yield of 19.2% shows a loan amount of $9,181,291 leftover. So exit cap rate 6.0% on $1,762,808 yields a valuation of $29,380,133 - $9,181,291 yields $20,198,841 of proceeds of which $19,397,411 went to the investors and $801,430 went to the GP, yielding a "loss" of about $250,000.

And some investor is thinking, "Wow, these guys gave us all the profit!"

Check my math. Did I miss anything? I was never the best analyst at my old company.

I'm having a little trouble following. First off, these numbers are all over the place. You say the asset traded for 12.34mm, but then that the syndicator claims 16.85mm. These are not irreconciliable, since the asset price and the transaction price can vary (as you say, closing costs, maybe they're doing some work, etc). That does not mean they "walked away with $5.63mm". Assuming these guys are honest (which we obviously shouldn't) then they've disclosed their fee load, which is about $430,000.

I'm also not sure why you're assuming a "loss" of $250,000? Where is that coming from? I also don't know why you aren't giving the 2.05x return to the GP dollars... usually all money is treated pari passu until the hurdles get hit and that's when promotes kick in.

All of the technical questions aside, the thing to remember about these syndicators is that they're running a scam. They'll promise anything as long as it's short of securities fraud and that's that. I mean, look at these assumptions! 63 bps of cap rate compression? These guys are probably feeing the hell out of this thing, even beyond what they're showing, and my guess is a lot of the money that is meant to go to CapEx is going straight in their pockets.

My notes aren't easy to follow, I admit, but here's what we do know according to the financial analysis page.

Looks like they're using $1.6M+ to fund renovations through GP and LP fund raising.

Then here's the Summary.

Equity multiple of 2.05x is what the GP is advertising so that's how I got $19,397,141. No idea what the splits are to get to the 2.05x.

My math could absolutely be wrong on the GP calcs, because that doesn't make sense. How I got there was backing out the exit valuation ($29,380,133) - the remaining loan balance accroding to the debt yield ($9,181,291) which is $20,198,841 of proceeds, of which $19,397,141 of that would go to the investors. This could be wrong because of the estimation on the loan balance amount, among others.

The important thing to note is from the first picture. $16.850M purchase price, when they actually bought it for $12.34M according to two different websites. That's the part we should probably most focus on, rather than my math.

There is a tax strategy (prevalent in FL) that can obfuscate the purchase price and may explain the lower publicly disclosed price. If that’s it, and they are publicly disclosing the actual price in a deck readily available online, then that strategy probably isn’t going to work and goes against the recommended advice of those that help implement it.

Are you referring to Cost Segregation or something else? I don't know the Florida market, but being able to reduce the purchase price by ~$6 million for tax purposes is pretty wild.

It's really unfortunate that interest rates were so low for so long it brought these type of people into the business.

There's maybe a 5% chance this business plan works out. T12 NOI of 992k and they proforma a 1.76m NOI at exit 5 years later, which is an average of 12% annual growth. Just insane stuff. Feel bad for the for the sucker LPs they swindled into investing into this.

Please don't try to replicate this.

Are pitch decks like this usually public? If so where could I find more?

what is complicated?

LPs invest in a projected MOIC or IRR.

the path to acheiving the return is in essence the diversification that a EM equities fund of fund uses when investing in different strategies.

equity creation via asset/biz performance, price, capital stack optimization.

LPs look at risk of new dev revolving around the capital stack and plan execution. better returns in new dev if I am not mistaken but a lot of the value creation comes from plan execution and conservative budgeting around early costs and mainly securing materials. 6 months can impact costs put the model at risk with a lender and financing that isnt accomadtive for such a scenario.

LPs look at value add execution as hard to fuck up and if it does happen that cpital is lost its typically because LPs made poor decisions in their underwritng duty and cut corners when red flags were clear. likely drinking same koolaid the gp was sipping. manage leverage and underwrite conservatively and its hard to lose capital.

you chose new dev as the vehicle for capital to appreciate and avoid taxes.

others choose new dev active 55 or senior living acquisition core+/value add

a lot choose value add MF historical because the predictability of a range of returns. there is no reward for complexity and bucking the crowd if opportunity cost and risk/reward profile of new dev vs. light re dev or value add doesn't support your choice.

if your LPs are typically all HNW fam office guys nearing retirements vs. new class of early 40s upperclass, then your ability to raise capital for a certain profile of deal will be driven by your access to capital.

a belief that an incremental buyer will pay a higher price than you paid for the asset.

Again, I am not totally certain what you are even asking. You are a bit all over the place.

How do syndicators make money:

Fees and carried interest. Acq fees, asset management fees, dispo fees, loan fees, affiliated entity fees. And in this case, someone mentioned a 25% carry over a pref.

Now, the equity multiple is not just backend profit from sale, but also any distributions along the way. So, without knowing the deal, if there is $10mm equity in the deal, they are paying out 8% per year, for 5 years, before a sale, the deal is already at a 0.40x EM. So, assuming the deal sells for break even, in this scenario, the LPs are at 1.4x EM in the deal. So the remaining profit would add to that.

As for reported sales price vs deck: this is extremely common. Most publications pull from title searches for transaction value. But when a buyer is buying the property, they are buying the land, improvements, branding of the apartment complex, computer systems, furniture, etc. They are buying a full scale business. As such, the most common reporting I see is about 80% of the purchase price is allocated to actual real estate, with the other 20% being allocated to non-real estate items, like goodwill. This allows the buyer to mitigate the real estate tax bill post sale.

The question I am asking: Did these guys really just pay $12.34M for a property and sell it back to themselves for $16.85M?

As for reported sales price, I get what you are saying. But do you really think CBRE only published 73.2% of the sales price ($12.34M vs $16.85M)?

I don't see anywhere in the two articles you shared that CBRE reported anything. Traded simply stated that CBRE was the broker of record on the transaction. But my experiences with Traded is: they take public information, do a little bit of research to determine the underlying buyer (since more of these deals are random LLC to other random LLC) and publish it.

Knowing nothing about the deal or the buyers, I can't really say whether the deal was closed at one price and resold internally at another price. While I have heard rumors of that happening with some groups, I have never seen any proof of that. As such, my assumption is the actual transaction price between CPI and Mainline (the listed buyer and seller per Traded), was 16.85mm. And the allocated price of the real estate, within that transaction, was recorded at 12.34mm. In my experience with real estate tax consultants, the recorded price of a transaction which impacts the real estate tax bill, is between 75% and 80% of the "actual" purchase price. This one, as you note, is a little more aggressive than typical, but within breathing room.

Natus perspiciatis velit libero excepturi deserunt. Ipsum sed placeat quo numquam voluptates qui aut. Et distinctio voluptatibus temporibus rerum dolorem eligendi.

Id optio praesentium assumenda repellat. Quibusdam adipisci vel possimus eligendi suscipit consequatur.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...