Keynesian Economic Theory

A macroeconomic theory that has recently impacted economic thought, named after the economist John Maynard Keynes.

What Is Keynesian Economic Theory?

Keynesian economics theory is a macroeconomic theory that has recently impacted economic thought. It is named after the economist John Maynard Keynes. It underlines the significance of aggregate demand in deciding economic activity and works in an economy.

The 1930s Great Depression was a period of massive economic downturn. The depression was marked by elevated joblessness, low economic activity, and boundless poverty.

The conventional economic theory of the time, known as classical economics, held that markets would normally change by reestablishing economic harmony over the long haul. It also held that government intervention would just cause shortcomings.

In any case, Keynes tested this view and contended that markets might not necessarily change rapidly to the point of reestablishing economic harmony, especially during times of economic recession.

It states that government intervention, especially through fiscal and monetary policy, can assist with balancing out the economy and lessen joblessness. One of the critical commitments of this theory is the idea of the Keynesian multiplier.

The multiplier alludes to the possibility that a government spending or investment change can largely affect aggregate demand and economic activity more than the initial change in spending or investment.

This is because the initial expansion in spending or investment can prompt a chain response of expanded spending and pay as the beneficiaries of the initial spending or investment increment their spending.

In this article, we will check out some of its important principles, like the significance of aggregate demand. Also discussed is the role of government intervention and the Keynesian multiplier.

We will likewise look at a portion of the critiques of this theory and its application in practice, especially during economic recession and crisis seasons.

- Keynesian Economic Theory is named after the British economist John Maynard Keynes, who revolutionized economic thought during the Great Depression with his book "The General Theory of Employment, Interest, and Money," published in 1936.

- Keynesian economics emphasizes the role of aggregate demand in influencing economic output and employment. It posits that insufficient demand leads to unemployment and unused capacity.

- The theory advocates for active government intervention to stabilize the economy, suggesting that fiscal and monetary policies are essential tools to manage economic cycles.

- Keynesian theory supports the use of monetary policy to influence interest rates and the money supply. Lowering interest rates can stimulate borrowing and investment while raising them can help control inflation.

Aggregate Demand and Aggregate Supply

Demand and supply have always been an important part of an economy. But in this theory, they may play a slightly different role.

Aggregate Demand

Aggregate demand in this theory alludes to the aggregate sum of items and services that all areas of the economy, including individuals, companies, and the government, are willing and prepared to buy at a specific price level.

Aggregate demand is affected by different variables, including consumer confidence, loan fees, and government policies.

The aggregate demand curve, which depicts the relationship between the general level of prices and the total quantity of products and services that will be demanded at that price level, addresses aggregate demand.

The aggregate demand curve slopes downward, demonstrating that the quantity of goods and services demanded decreases as the price increases.

Aggregate Supply

On the other hand, aggregate supply refers to the aggregate amount of products and services that every region of the financial system, including families, agencies, and the authorities, is inclined and organized to supply at a given price stage.

Different variables, like technology, input prices, and government guidelines, impact aggregate supply.

Aggregate supply is tended to by the aggregate supply curve, which shows the relationship between the general level of prices and the outright quantity of goods and services that will be given at that price level.

The aggregate supply curve can be divided into two parts. They are short-run aggregate supply and long-run aggregate supply.

The short-run aggregate supply curve slopes upward, demonstrating that the quantity of goods and services provided increases as the price level increases.

In any case, the long-run aggregate supply curve is upward, demonstrating that modifications within the price level don't impact the number of goods and offerings furnished over the long haul.

Aggregate Demand And Supply in Keynesian Theory

In this theoretical framework, the equilibrium output level is partially set in stone by the intersection of the aggregate demand curve and the short-run aggregate supply curve.

Assuming the economy is working beneath full employment, the intersection of the two curves might happen at the output level and employment underneath the full employment level.

In this situation, this theory contends that government intervention, especially through fiscal and monetary policy, can assist with expanding aggregate demand and stimulating economic activity.

The Keynesian Multiplier

The Keynesian multiplier is a focal idea in this theory. It alludes to the possibility that an underlying change in government spending or investment can largely affect aggregate demand and economic activity more than the underlying change in spending or investment itself.

The multiplier arises from the idea that the initial increase in spending or investment can lead to a chain reaction of increased spending and income as the initial spending or investment recipients increase their spending.

For instance, assume the government increases spending on infrastructure projects like roadways or bridges. This initial increase in spending will create new jobs and increase the income of those involved in construction projects.

As these workers and contractors earn more money, they will likely increase their spending on goods and services. This increased spending, in turn, will generate further income and spending as the recipients increase their spending.

The MPC alludes to the proportion of extra income spent on utilization, while the marginal tax rate alludes to the proportion of extra income to be taxed. High MPC and low marginal tax rates increase the multiplier effect.

The Keynesian Multiplier formula is given by:

Multiplier = 1 / (1 - MPC)

Where,

- Multiplier: This represents the multiplier effect, indicating the total increase in GDP.

- MPC: Marginal Propensity to Consume is the fraction of each additional dollar of income spent on consumption. It measures the change in consumption resulting from a change in income.

For example, if the MPC is 70% of the additional income. Then the multiplier would be:

1 / (1 - 0.7)

1 / 0.3 = $3.33

This means that for every dollar the government spends, there is additional spending of $3.33.

The Keynesian multiplier has profound implications for economic policy. It suggests that government spending and investment can increment economic activity and diminish unemployment during economic downturns or recessions.

Note

By increasing government spending or investment, the government can generate a multiplier effect that stimulates additional spending and economic activity. Similarly, reducing taxes or increasing transfer payments can also raise disposable income and generate a multiplier effect.

Be that as it may, the utilization of fiscal policy to boost the economy can likewise have downsides, like inflation and budget deficits. Thus, the suitable utilization of fiscal policy relies upon the particular economic circumstances and the general goals of economic policy.

Critiques of Keynesian Economics Theory

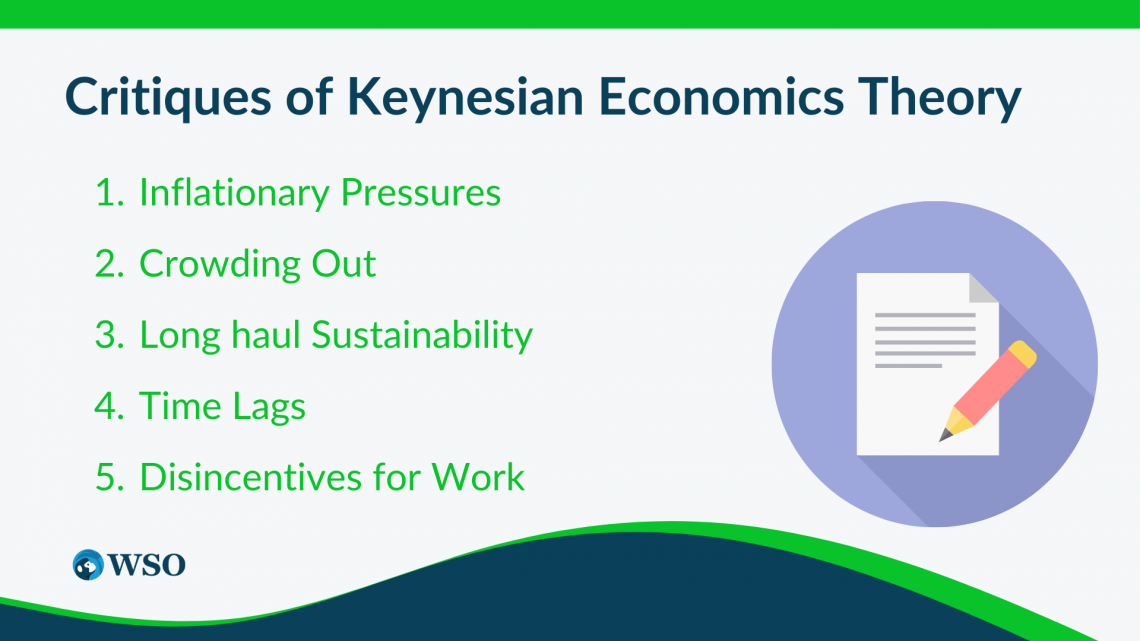

Despite its boundless use and ubiquity, this theory has been subject to a few investigations and challenges from economists and policymakers throughout the long term. A portion of the critical investigations of the theory includes the following:

- Inflationary Pressures: Critics contend that Keynesian policies, such as government spending and low interest rates, can prompt economic inflationary pressures.

- If the government increases spending without a comparable increase in efficiency, it can prompt a lot of money to pursue a couple of goods, which can drive up prices.

- Crowding Out: Another investigation is the crowding-out impact, which happens when increased government spending and borrowing prompt higher interest rates and decreased private investment. This can lessen Keynesian policies' viability and reduce their capacity to invigorate economic growth.

- Long-haul Sustainability: A few critics contend that its policies, such as deficit spending, are not sustainable in the long haul and can prompt the development of debt and fiscal imbalances. This can subvert the economy's stability and lead to higher interest rates and inflation.

- Time Lags: Its policies can also lead to lags, which implies that the impacts of policy changes may not be felt right away and may require a while or even a long time to affect the economy.

- This can make it hard for policymakers to calibrate economic policy and respond to changing economic circumstances.

- Disincentives for Work: A few critics contend that Keynesian policies, such as unemployment benefits and different types of welfare, can make disincentives for work and lessen labor efficiency. This can prompt lower economic growth and diminish motivation for people to enter the labor market.

- Notwithstanding these investigations, this theory remains a widely used and compelling economic theory.

Note

Many reactions to Keynesian economics have prompted refinements and transformations of the theory over the long run, including improving existing models and policy devices to address its constraints.

Keynesian economics continues to be a subject of ongoing conversation among economists and policymakers.

Keynesian Economic Theory in Practice

It has been tried in different nations and under various economic conditions, with shifting levels of progress.

In practice, this theory has been utilized essentially to oversee macroeconomic instability and advance economic growth.

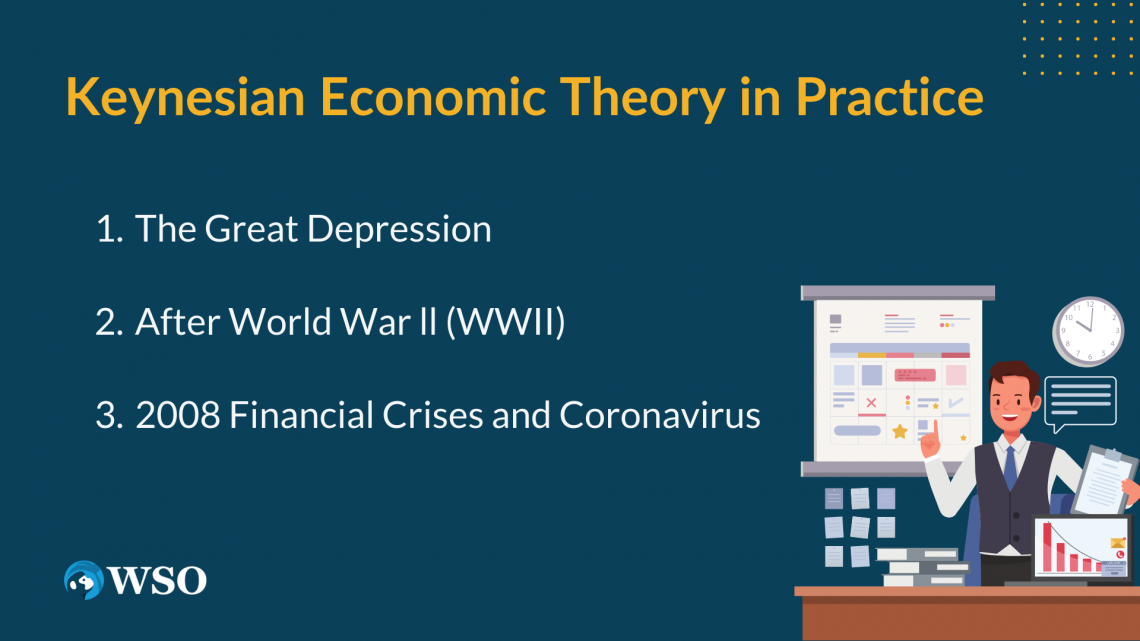

The Great Depression

It was put into practice during the Great Depression. It occurred in the United States in 1929-39. President Franklin D. Roosevelt implemented a series of Keynesian policies known as the New Deal in light of the extreme economic downturn.

These policies included government spending on infrastructure projects, social welfare programs, and endeavors to control and settle the financial system.

These policies assisted with balancing out the economy and advancing economic growth, albeit the recuperation was slow and lopsided.

After World War ll (WWII)

It was additionally applied in a few newly formed nations after WWII, including the United States, Western Europe, and Japan. During this period, governments embraced Keynesian policies to advance full employment and economic growth.

2008 Financial Crises and Coronavirus

As of late, it has been utilized in light of different economic emergencies and recessions, including the 2008 financial crisis and the Coronavirus pandemic.

In both cases, governments carried out Keynesian policies, including spending on upgrade programs, tax cuts, and monetary policy devices like low-interest rates and quantitative easing.

These policies assisted with settling the economy and advancing economic growth, albeit the recuperation has been slow and lopsided.

Note

As the worldwide economy keeps developing, the job and viability of Keynesian economics in practice will probably continue being a subject of discussion and conversation among economists and policymakers.

While it has been fruitful, it has its limitations and challenges. Keynesian policies can be challenging to implement and hampered by political and economic hindrances.

Moreover, there is a growing debate among economists and policymakers about the best ways of applying this theory in practice, especially regarding globalization and changing economic conditions.

It has been tried in different nations and under various economic conditions, with shifting levels of accomplishment.

While it has been effective in settling the economy and advancing economic growth, it has its limitations and challenges.

Keynesian Economic Theory FAQs

It is an economic theory that stresses government intervention's significance in settling economic fluctuations and advancing economic growth.

It tends to economic recessions by supporting government intervention through fiscal and monetary policies to invigorate demand and balance out economic activity.

In this specific circumstance, aggregate demand alludes to the general demand for goods and services in an economy. However, aggregate supply alludes to the entire supply of economic items and services.

The theory underlines the significance of adjusting aggregate demand and supply to advance economic stability and growth.

The monetary policy assumes a part in this theory by impacting the economy's money supply, interest rates, and credit availability.

The theory stresses using monetary policy to animate demand and balance out economic activity in tandem with fiscal policy interventions.

In this theory, expectations are a basic part of impacting consumer and investor conduct, influencing aggregate demand and economic growth.

Expectations about future economic conditions, government policies, and elements can impact spending and venture decisions and invigorate or dampen economic activity.

This theory has been applied in various nations and under various economic conditions, with fluctuating degrees of success.

Models remember the New Deal for the United States during the Great Depression, government reactions to economic crises like the 2008 financial emergency and the Coronavirus pandemic, and the utilization of fiscal and monetary policies to advance economic growth and stability in nations like Japan and Sweden.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?