How to Read a Balance Sheet

It shows what your business owns and owes and the money left to the owner at the reporting date

What Is A Balance Sheet?

A balance sheet is one of the financial statements. It shows what your business owns and owes and the money left to the owner at the reporting date. The information is shown in three parts in B|S, including Asset, Liability, and Owner’s Equity.

The Balance Sheet, also known as the statement of financial position, is the primary accounting statement that represents the financial position (i.e., the status of assets, liabilities, and shareholders' equity) of an enterprise at a certain date (usually the end of each accounting period).

The balance sheet uses the principle of accounting balance to divide assets, liabilities, and shareholders' equity into two main blocks:

- Assets

- Liabilities and shareholders’ equity.

After accounting procedures such as

- Journal entries

- Transfers

- Ledgers

- Trial balances

- Adjustments

After making entries, transfers, ledgers, trial balances, adjustments, and other accounting procedures, the report is condensed into a single statement based on the static corporate situation at a specific date.

The report's purpose is to remove errors within the company, manage the direction, prevent fraud, and let all readers understand the business situation quickly.

What does the balance sheet help to decide?

It is possible to see the distribution of the company's assets and the composition of its liabilities and owner's equity with the help of the information in the balance sheet. These can be used to evaluate whether the company's operations and financial structure are reasonable.

1. Invest in a company or not (Investor)

E.g.,Investors might look at the value of net income or loss to see the ability of a company to sell its products.

2. Develop the firm’s strategy (Manager)

E.g., The current ratio helps determine the ability to pay the debt, which is important for managers. Based on the ratio, they can deploy the borrowing strategy for the next year. The current ratio only depends on the current asset and current liability.

3. Adjust their process (Employee)

E.g., Employees need to optimize their working process if they have too much inventory left at the end. Inventory will appear on the current asset. Whether it is an investor, manager, or employee, understanding B|S is a key skill to compete with others.

Note

B|S provides a brief financial status of a company at the end of the fiscal year.

The purpose of the balance sheet

Purpose can vary depending on the positions of the persons to review them.

There are three main purposes.

- The reason for people from the company to review the B|S is to understand whether a company has succeeded or not.

B|S not only reveals the company’s financial condition but also shows the sales performance of the company. Thus, they can change the company's strategy and working process to improve their next year's B|S. - When it is reviewed externally by people from outside the company, such as potential investors, its purpose is to let the audiences learn about the company's resources and how they are raised. Based on this, investors can decide whether it is wise to invest in this firm.

- If B|S is used for audit, external auditors may use it to ensure that the company complies with any reporting laws it complies with.

How to read a balance sheet

A balance sheet generally has two parts: the header and the main statement. The statement's header outlines the statement's name, the unit of preparation, the date of practice, the statement number, the currency name, the unit of measurement, etc.

The main statement is the main body of the balance sheet, which presents the items used to illustrate the enterprise's financial position. There are two general formats for the main balance sheet: the reporting balance sheet and the account balance sheet.

The reporting balance sheet is a top-and-bottom structure, with the top half showing assets and the bottom half showing liabilities and owners' equity.

There are two types of arrangement: one is according to the principle of "assets=liabilities+owner's equity"; the other is according to the principle of "assets-liabilities=owner's equity."

The account-based balance sheet is a left-right structure, with assets on the left and liabilities and owners' equity on the right. Regardless of the format, the equation that the total of each item of assets equals the sum of each item of liabilities and owners' equity remains the same.

What financial statements should be prepared before constructing a balance?

Adequate preparation must be done before preparing accounting statements. Generally, there is a verification of assets, liquidation of debts, review of costs, internal reconciliation, trial balance, and closing of accounts.

The formula is as follows:

Revenue - Cost of Goods Sold - Expenses = Net Income/Loss

Gross Income - Expenses = Net Income/Loss

The accounts that include revenues and expenses will be summarized into account Net income. All accounts in the income statement will not appear in B|S, and we will use Net Income/Loss in the Statement of Retained Earnings.

2. Statement of retained earning

Formula:

Beginning Retained Earnings + Net income/Loss - Dividends = Retained Earning

In the statement of retained earnings, we summarize the Net income/loss that will appear in the Owner’s Equity in B|S.

Balance Sheet Structure

The balance sheet structure is divided into two major parts. The basic part is divided into left and right sides, with the left side reflecting the composition of the enterprise's assets.

The right side is further divided into upper and lower sections, with the upper section reflecting the composition of the enterprise's liabilities. The lower section reflects the composition of the owner's equity.

The sum of the upper and lower sections on the right side equals the sum on the left side. This follows the basic balance principle of "Assets = Liabilities + Owner's Equity."

A) Asset

The asset represents anything owned by a company with inherent and quantifiable value, which can be converted to money if necessary. It has two types:

Assets that can be converted to cash within one year.

- Cash

- Cash Equivalent

- Account Receivable

- Note Receivable( less than 1 year)

- Office Supply

- Inventory

- Prepaid Asset/Expense

2. Non-current asset

Assets that can not be converted to cash in the short term.

In the Asset part, we need to list these accounts in order of their liquidity, that is, how easily they can be converted into cash, sold, or consumed.

The more easily liquidated assets will be listed first, so cash always comes first, and current assets are more accessible to convert than non-current assets.

B) Liability

Liability represents anything that a firm owes others, which is the legal obligation of a firm to pay for it.

Just like assets, liability is also divided into current and non-current.

1. Current Liability

Liabilities due to the debtor for one year

- Account Payable

- Notes Payable

- Salary Payable

- Trade Payable

- Interest Payable

- Utility Payable

- Other accrued expenses

2. Non-current liability

Liabilities due to the debtor for more than one year

- Loan

- Bond Payable

- Long-term Note Payable

- Deferred tax liabilities

- Provisions for pensions

C) Owner’s equity (shareholder’s equity)

Owner’s equity or shareholder’s equity refers to all income, excluding liabilities belonging to the company's owner.

It mainly comes from two sources. One is that investors provide money for the company through investment, and the company issues stocks to investors as an exchange. The second is the wealth accumulated by the company over time.

- Capital: Capital is the total amount of money the owners invested.

- Private or public stock: Private or public stock is the common shares or preferred shares that a company issues.

- Retained earnings: Retained earnings refer to the profit remaining after deducting all expenses and dividends from the total income.

The balance sheet equation is as follows:

Asset = Liability + Owner's Equity

Example of the Balance sheet’s structure

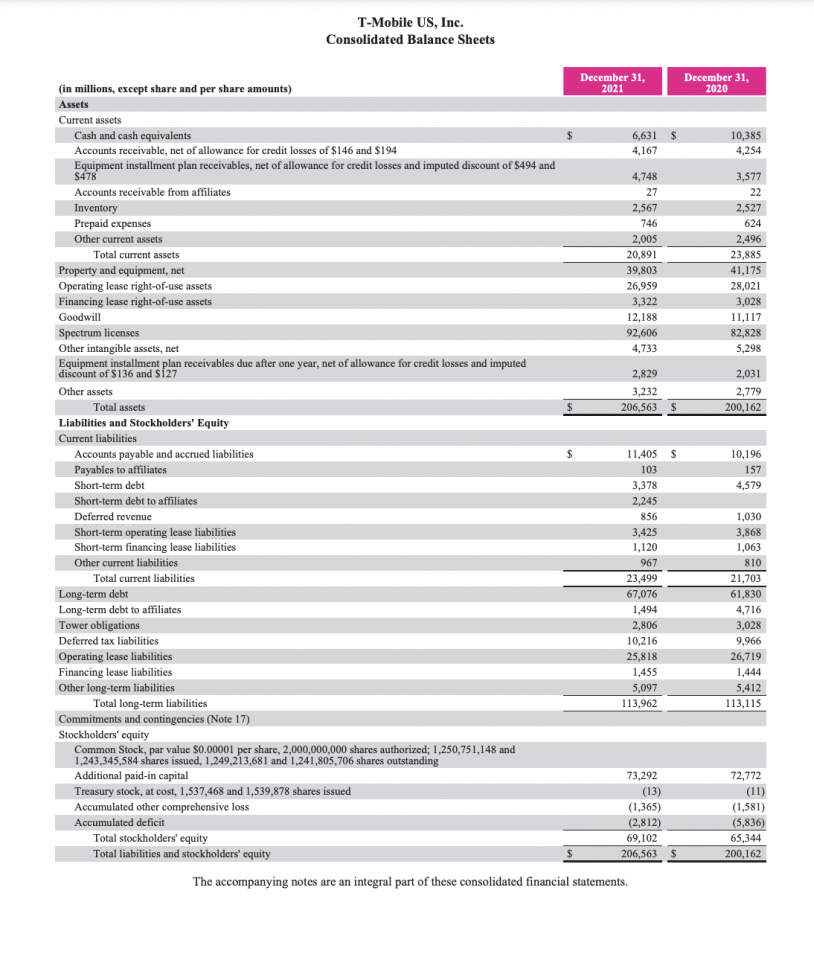

Let’s look at an example. We will explain an example of a B|S from T-Mobile US, Inc. - Annual Reports 2021-2022.

This example gives a standard structure of a B|S. It included three main parts, i.e., Asset, Liability, and Stockholders’ equity.

Current Assets: Cash and cash equivalent, Account receivable, Equipment installment plan receivable, Inventory, Prepaid expense, and other current assets are listed in order of their liquidity in the present asset part.

- Property and equipment accounts in other assets are non-current assets.

- The account payable to other current liabilities is a current liability.

- The account from long-term debt to other long-term liabilities is non-current.

This example also satisfied the balance sheet equation. Its total asset equals total liability plus the whole stakeholders’ equity.

From the example above, when we read a balance sheet, we should know several key points:

- Look at company names and the balance sheet date.

- Check if total asset = total liability + owner’s equity.

- Check the amount of the total asset, total liability, and complete owner’s equity.

- E.g., if the total asset amount equals the sum of the total current and non-current assets.

- Check if all accounts are placed in the right section and if they are listed in the order of their liquidity.

- Understanding special accounts

- Accumulated depreciation

- Prepaid expenses and accrued income

- Unearned revenue

- Net income/Net loss(From income statement)

- Retained earnings (From the view of retained earnings)

Analyzing a Balance Sheet with Ratios

Balance sheet financial ratio analysis is the process of taking different financial numbers and forming a meaningful ratio to examine a company's financial health. Balance sheet ratios are the most basic and easy-to-calculate numbers but are often overlooked for this reason.

The working capital cycle measures a company's time to turn its current asset and current liability into cash.

The goal for a company is to reduce working capital by collecting their receivables like accounts receivable and notes receivable as soon as possible.

A company with good financial health should have enough working capital to pay its liabilities.

Working capital = Current Asset - Current Liability

From this formula, a positive working capital suggests that after paying all debts, the company still has money to invest, upgrade equipment, etc.

If the working capital is negative, the company is not sufficiently liquid to pay its current liability, which implies this company might face the risk of bankruptcy.

2. Current Ratio

Like working capital, the current ratio is a liquidity ratio to measure whether a company has enough resources to pay its short-term liabilities.

Current ratio = Current asset / Current Liability

A company with a higher current ratio is more likely to pay its short-term liabilities than other companies with lower current ratios.

Specifically, if the current ratio for a company is less than 1, it will have problems meeting its short-term obligation. Otherwise, the company might avoid bankruptcy in a short time.

However, an unusually large current ratio is not always a good thing for a company to attract investors since this indicates the company did not use its current assets well to run its business. In this case, wastage of resources might be observed.

There are two limitations to using the current ratio to measure different companies.

- This ratio is only helpful in comparing two companies within the same industry because different industries might have various operating forms.

- It is unreliable to measure liquidity when we only have a current ratio.

3. Acid-test Ratio (Quick Ratio)

Inventory and prepaid expenses are not easily converted to cash as other current assets. In other words, these two accounts have poorer liquidity.

We remove these two accounts from current assets in the Acid-test ratio and recalculate the current balance. We will get an acid-test ratio.

Acid-test ratio is a more reliable index for investors to measure a company's liquidity than the current ratio since it indicates if the highly liquid assets are enough to cover the short-term liability.

Quick Ratio = (Current Asset -Inventory -Prepaid Expenses ) / Current Liability.

Similar to the current ratio, a higher quick ratio shows the greater liquidity of the company. Also, the fast ratios are usually greater or equal to 1.

4. Debt Ratio

Debt Ratio, as one of the solvency ratios, measures the financial leverage of a company and its ability to pay off its total liabilities using its total assets.

Debt Ratio = Total liability / Total asset

The higher debt ratio reveals the higher risk of the lenders. The company’s lenders are likely not to recover their debts.

A low debt ratio means a company has the potential for sustainable development because its total debt will also be relatively low.

0.5 is generally considered a reasonable ratio. The debt ratio of 0.5 means that the company is less risky because its assets are twice as much as its debt.

The debt ratio of 1 means that the total liabilities are equal to the total assets, and the company needs to sell all its assets to repay its debts. If the company’s assets are sold, it will face the risk of bankruptcy.

How to Read a Balance Sheet FAQs

Almost every financial crisis can be traced back to weak balance sheet fundamentals, which cracked under the pressure of excessive debt.

Companies, households, and governments borrow heavily in good times but then struggle to service that debt when economic conditions turn nasty.

A healthy balance sheet is a sign of a strong business. It tells a story about the business's past, today, and how it prepares for the future.

When securing financing for your business, a healthy balance sheet is a crucial financial report that underscores the strength of your business and its ability to weather any economic storms.

Given the uncertainty about the future and detailed pandemic contingency plans, it has never been more important.

A balance sheet is a financial snapshot document of a business's assets, liabilities, and equity at the end of an accounting period.

Business owners and investors often use balance sheets to measure the overall financial position of their organizations.

or Want to Sign up with your social account?