Q1' 2026 RX IB & RX Co. Rankings (Octus)

RX IB:

RX Consulting:

RX IB:

RX Consulting:

| +186 | UBS Accused of Favoring H-1B Workers While Cutting U.S.-Born Employees | 46 | 4h |

| +83 | IB Energy Drink Tier List / Ranking | 57 | 5h |

| +76 | PJT M&A Group Selection 2026 | 13 | 17h |

| +55 | ONLY THESE BANKS OR YOU STRUCK OUT | 15 | 3m |

| +36 | Quick Thoughts on CVC AI Sale Process | 7 | 3d |

| +34 | Feedback for internship first desk at IBD BB - personal fit, "don't be too confident" | 23 | 1d |

| +28 | Does BofA still pay its associates rat pellets? | 14 | 7h |

| +18 | What happened to Greenhill | 8 | 3d |

| +18 | Updated JPM Group Rankings | 30 | 8h |

| +18 | VP Deal Origination Credit | 2 | 15h |

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

Bump

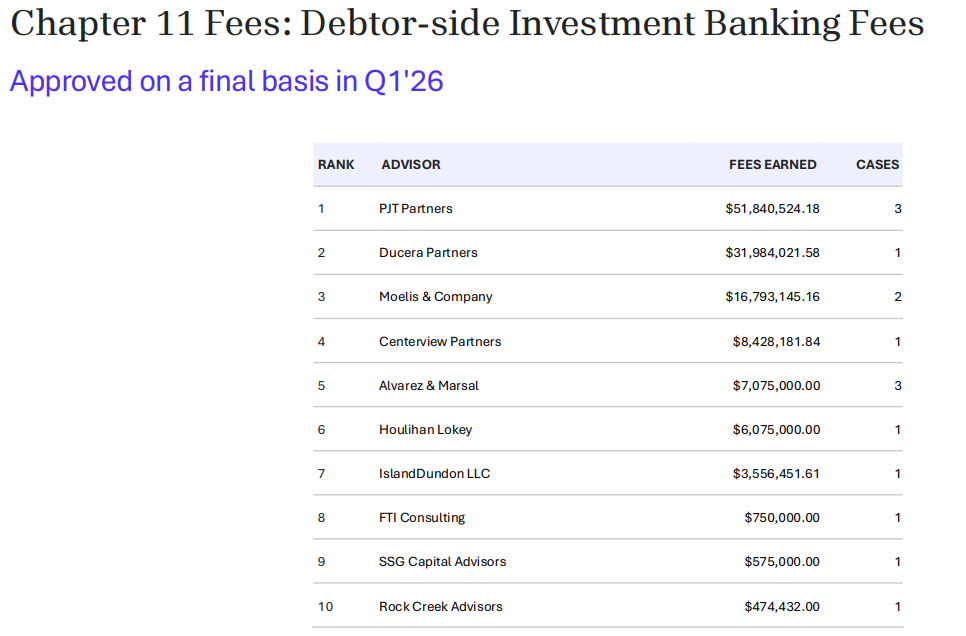

Wait A&M and FTI have IB groups?

Yes, small teams that work on mandates they receive from the CO work

But they’re top 5 in the tables attached atleast, are they big mandates?

Haha where is Evercore, Gugg and PWP. All in the mud

This is just chpt 11, not the bread and butter rx work that is out of court. Very few filings in Q1'26 so all these chpt 11 fees are off of n=1 or n=2 cases for these firms

For some reason OP put debtor fees too which is one of the least useful metrics. Most useful to look at total engagements and what LMEs each group has been on (lots of Moelis, PJT, HL, and Evercore)

Op did post total fees somewhere on this thread. Would argue fees is a very helpful metric though, gives an idea as to scale. It’s not the end all be all metric but still

1. Why are A&M and FTI IB arms so high up?

2. Who tf is IslandDundon?

3. How is BRG not on here when they’ve been Debtor side advisor on 3 of the top 10 largest deals this year? Are they doing pro bono work lol

4. Where is PWP?

4. Who paid Ducera 31M in advisory fees over a 3 month period? Damn

Ok that makes alot more sense. IG final approval of fees are a bit slower than vanilla transaction fees due to slower moving court processes, but I’m still curious how IBs are compensated in a Ch 11 RX - I thought their primary source of Revenue still came from gross transaction %. Do these fees include that form of compensation, or are these solely “advisory” fees for Cap structure management? Bc if Ducera is making that much off of one deal (even over a 4-5 month period) excluding their transaction/divestiture % proceeds then dam this is extremely lucrative. And are banks mostly hired in ch 11 for liability management, even when there’s no sale of assets? If so, why couldn’t say the consultants team with lawyers regarding liability/cap structure management, and save the company tons of money in fees?

It's actually not that surprising. RX IBs get paid on a success fee basis. If you put the monthly fees for the Rx IB, Rx consultants, and Rx lawyers into a spreadsheet side by side, the IB looks almost irrelevant, maybe $250K/month, while the consultants and lawyers are running at $750K+ per month. But at the back end of the deal, the IB collects a massive success fee in the millions, contingent on the transaction actually closing. The consultants and lawyers, by contrast, get a smaller back-end fee or none at all, they just keep running up the tab at a much higher monthly rate throughout.

But, in order for that to happen, there must be something that justifies hiring an IB. Usually this is an asset sale, and cases that involve that therefore tend to earn the RX IB a lot of money. I'm willing to bet that this was what this Ducera fee is for.

This could go wrong though. A good example is the very recent first brands case. Lazard stood to make around $16.5M on the DIP loan, plus a couple million off of retainer fees, plus around $33 million in a asset sale fee. But, the sale process basically collapsed, and they ended up with around $25-50 million all in, but missed out on the transaction fee.

The real winners of the restructuring process , almost every time, are the consultants and the lawyers. It's actually embarrassingly clear when you see the numbers. In the First Brands case, A&M billed $43.4 million in the first three months alone, court-approved, while the case is still grinding on with projections pointing toward fees in the high hundreds of millions by the time it wraps. In FTX, A&M earned roughly $120 million in 2023 and somewhere between $300–400 million over the full three-year case. PWP, the IB, earned a fraction of that over the same period, virtually nothing. The bankers made peanuts by comparison.

At the end of the day, the consultant and lawyers aren't betting on a deal closing, they just show up everyday and bill lol.

Because BRG isn’t a top rx firm… lol

I looked it up. Looks like its from Yellow's restructuring

Where is EVR??

Would suspect EVR will show up in the H1 or Q2+ rankings. It's still early in the year

If anyone has any experience, is it harder on average to get into M&A IB or RX consulting, at a junior level?

I came to Rx Co from the undergrad level, and I’d still say likely Rx IB simply due to supply. Across all the T1s, there’s maybe ~40 internship spots per year and most analyst classes are filed from internship conversions. The other Rx Co firms are also ramping up undergraduate hiring.

Not sure what the number of seats for RX IB are, but likely lower than ~40 across the reputable banks. The banks also likely have a more competitive pool of applicants (M&A bankers, PE analysts, etc.) than Rx Co.

Interested to hear others perspective on this though

No I’m talking about M&A IB not RX IB

Architecto sunt officia ab qui doloribus dolore. Et odit consectetur dolorum. Velit tempora beatae officia accusantium quo excepturi eum est.

Quaerat eius consectetur iste aut qui rem. Ut ipsum accusantium et omnis iusto et eligendi et. Ut ducimus animi voluptatem porro voluptatem veritatis. Eaque qui nulla tenetur dicta ab ea doloribus. Expedita veniam eaque voluptate voluptas. Consequatur suscipit accusantium excepturi dolor laboriosam voluptatum possimus.

Possimus possimus eum quod cum autem et alias. Harum est dolores repudiandae repellat sed temporibus et. Nobis maxime sit facilis veritatis dignissimos voluptate delectus. Iste nesciunt est sed eum nostrum.

Omnis rerum necessitatibus quas distinctio dignissimos qui fugiat nihil. Possimus adipisci qui dolorem omnis doloremque. Vel autem ea est.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Labore eaque amet sed qui sint repellat. Architecto voluptates et placeat suscipit et illo aut. Tempora sed dolorem possimus inventore qui.

Excepturi voluptatem fugit exercitationem id iste. Culpa et ea fugit officiis iure. Qui cupiditate id voluptatum dolor impedit aut. Dolorem vel eveniet qui exercitationem et odit sed. Officiis rerum omnis consequatur nostrum hic dolores dolore.