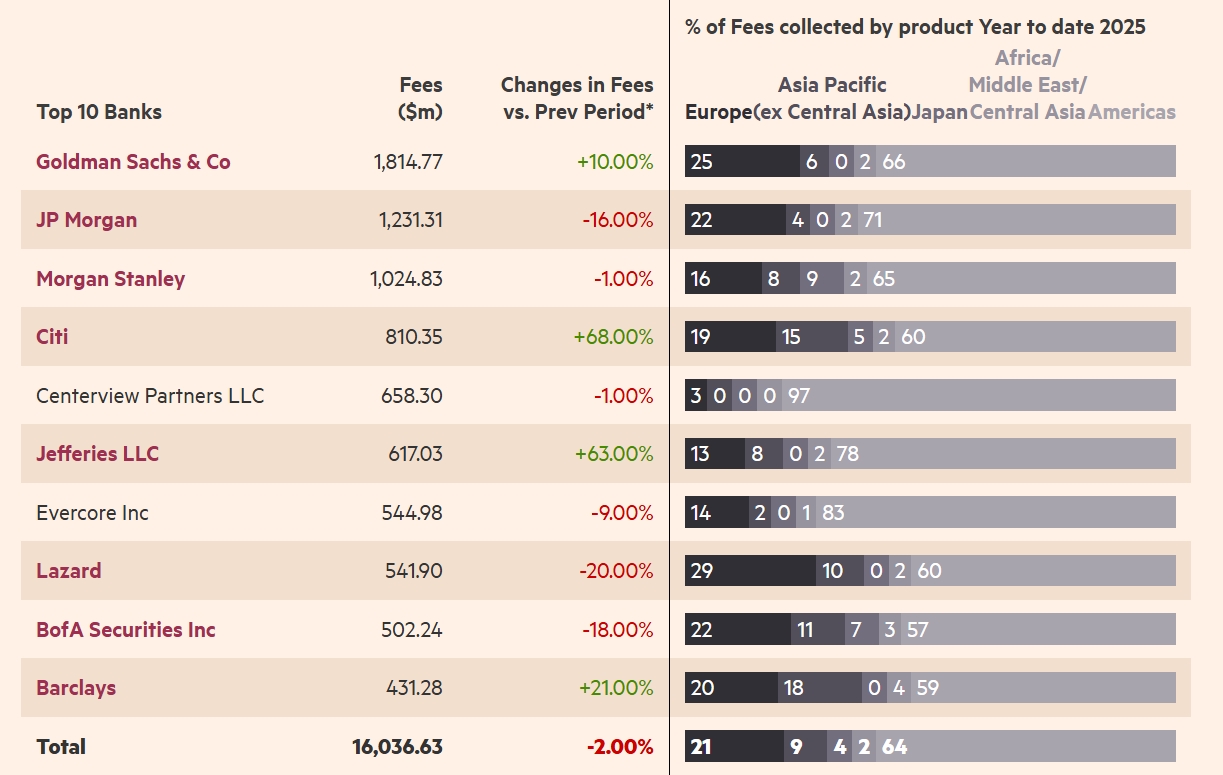

The Comeback of Citi and Rise of EBs

Thoughts?

Based off of M&A and looking at the last two quarters, seems like we can see the results.

Thoughts?

Based off of M&A and looking at the last two quarters, seems like we can see the results.

| +148 | ONLY THESE BANKS OR YOU STRUCK OUT | 38 | 13h |

| +111 | IB Energy Drink Tier List / Ranking | 73 | 1d |

| +61 | Firm Thinks I'm Lying About Offer | 19 | 16h |

| +53 | Indiana University Fraternity Pipelines | 32 | 13h |

| +51 | Feedback for internship first desk at IBD BB - personal fit, "don't be too confident" | 29 | 2d |

| +39 | Stay at Weak Dealflow Team or Lateral? | 12 | 21h |

| +36 | Rogo AI | 14 | 11h |

| +34 | Elite Boutique interview questions | 8 | 1d |

| +30 | Suspended for a Year | 11 | 14h |

| +23 | 1st Half 2026 (1H26) RX IB & RX Co. Rankings | 14 | 1d |

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

Where is UBS?!?!

They Died.

in 2018

JEF on a generational run

Interesting because they're not in the top 10 for deal value per Financial Times, but are #6 in fees. Do middle market deals have higher fee percentages or something?

Usually they do.

A big $10bn deal maybe has 0.5% fee for $50mm fees

A $2bn deal maybe has 1% fee for $20mm fees

A $100mm deal may have 3% fee for $3mm fees

All can vary quite a bit but that’s more of less the idea with rough estimates

Yes - I've worked on (during sellside) $150M deals with 3-4% fees and $1B+ deals with 1% fees.

Anyone know why their stock is down 30% YTD?

taking a very cursory look at it as an incoming fig analyst- all IBs grew after the election in anticipation of more dealflow then dropped after tariffs, with rebounds happening recently.

Jeff doesnt have the other divisions that BBs have to support IB flow or as strong a rx group as some of the public EBs to battle the cyclicality. Feff ballooned in price after election much more than other banks like pjt, evr, laz; with around 30% growth from early nov to peak in dec/jan compared to 10% in other boutiques. Not sure what drove this but im guessing jeff's unique levfin capability was judged as a potential hot market with interest rate cut forecasts which hasn't materialized. Jeff is also selling off their MBD divisions, leaving them even more reliant on ib cycles than previously, so any market volatility will hurt firm earnings even more. while their m&a fees look good above, their equity underwriting fees were cut in half in q2 which is much steeper dropoff than BBs

their current stock price is basically around their stock price from last year, so it could be argued this is more a normalization for them in 1Y stock price than a drop YTD, which was inflated post election more than other banks. their most similar looking comp is moelis which is also flat 1Y. not sure why other banks have rebounded but jeff/moe haven't; but my guess is their reliance on levfin type work for jeff and sponsor backed deals for moelis are not areas the market deems hot currently

Rerum cumque numquam officiis architecto molestiae illum ea ex. Voluptatem aliquid voluptatem molestias tempore modi maxime.

Distinctio molestiae voluptas et quidem voluptatem sed. Temporibus consequatur laudantium quis tempore impedit nam voluptatem. Distinctio ut et in neque sint in consequatur. Quia similique corporis mollitia voluptatem omnis quos deleniti quasi.

Occaecati dolore voluptas repellendus sed. Dolores aliquid explicabo in. Provident architecto illum molestiae rerum.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...