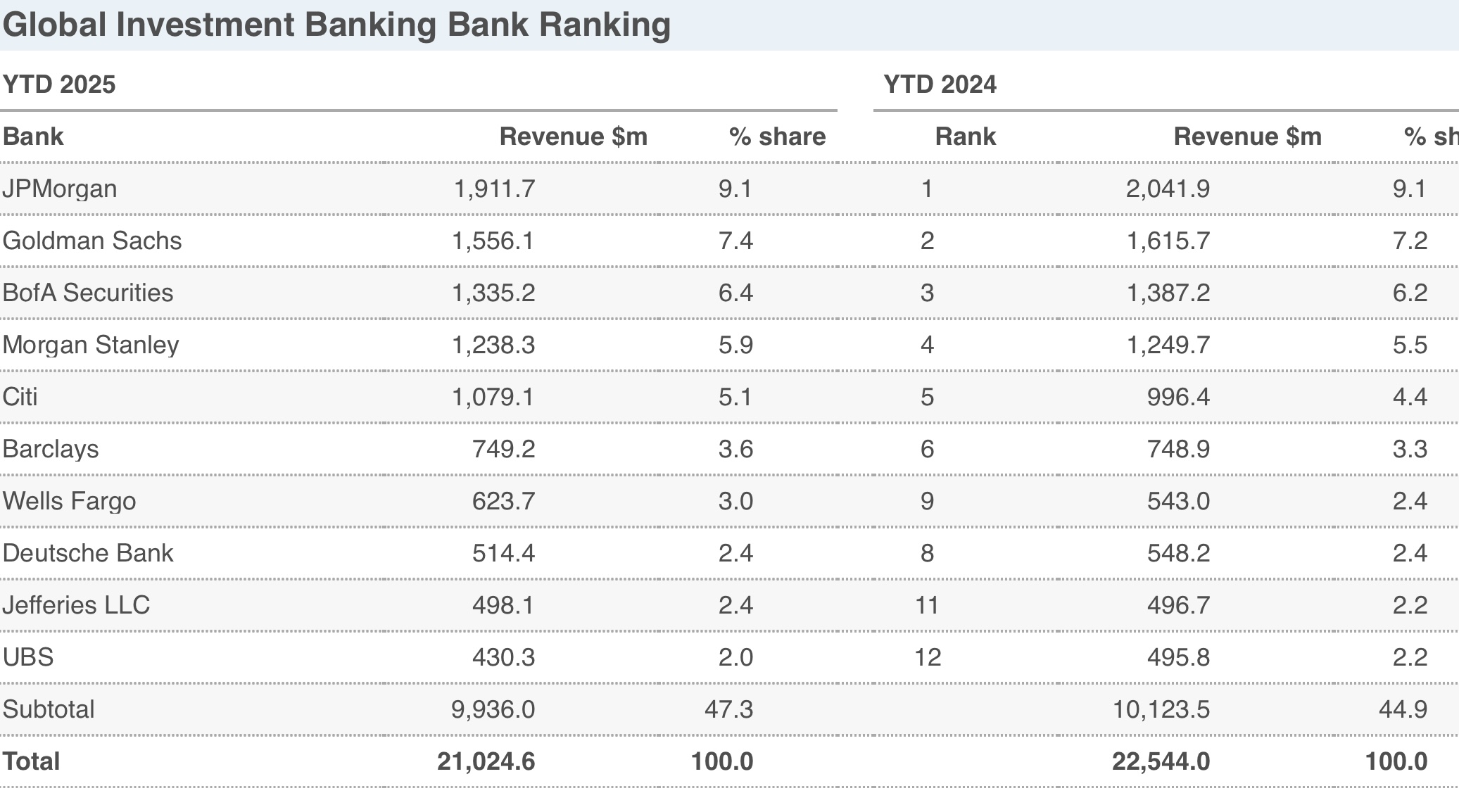

UBS IB Collapse Imminent? Global IB Rev. -13% YTD, Global IB M&A Rev -39% YTD

Quite shocking stats, what in the world is going on? These seem pretty bleak based on the market

https://dealogic.com/investment-banking-scorecard/

Quite shocking stats, what in the world is going on? These seem pretty bleak based on the market

https://dealogic.com/investment-banking-scorecard/

| +258 | Why UBS Is the Worst Place to Start Your IB Career | 40 | 10h |

| +213 | UBS 2nd Year Analyst Q&A (2026) | 38 | 17h |

| +83 | What's your craziest "hardo" story? | 13 | 1h |

| +70 | Firm Thinks I'm Lying About Offer | 20 | 2d |

| +62 | Indiana University Fraternity Pipelines | 36 | 1d |

| +51 | Rogo AI | 21 | 18h |

| +49 | Elite Boutique interview questions | 17 | 14h |

| +48 | Suspended for a Year | 19 | 2d |

| +40 | Stay at Weak Dealflow Team or Lateral? | 12 | 3d |

| +28 | Wolf of Wall Street vs. Reality: Anyone else feel scammed by the movies? | 10 | 8h |

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

Also noticed that average deal sizes collapsed from $2.4bn to $1.5bn. This means due to probably a couple outliers, most deals likely sub $1bn

Most of those deals are outside the US. As per the numbers for the US below: 56 Bn/16 deals = average 3.5 Bn deals. I think the exact opposite problem is happening in the US: UBS is going whale hunting and not trying to win or get any deals in the MM space. Also, explain why some groups struggle so much; they are probably just continuously pitching for large-cap deals but never winning because they aren't competitive for those deals due to a lack of notable creds. Whale hunting for a bank only works if you have good enough creds to focus on large-cap deals, it seems pretty clear that a lot of these UBS groups don't.

Going whale hunting is what MDs on guaranteed contracts say they’re doing as an excuse for their lack of actual deals

Yep. Looking at actual advisory revenue shows why even Centerview will happily run a $.4bn sell-side, because they actually pay pretty well.

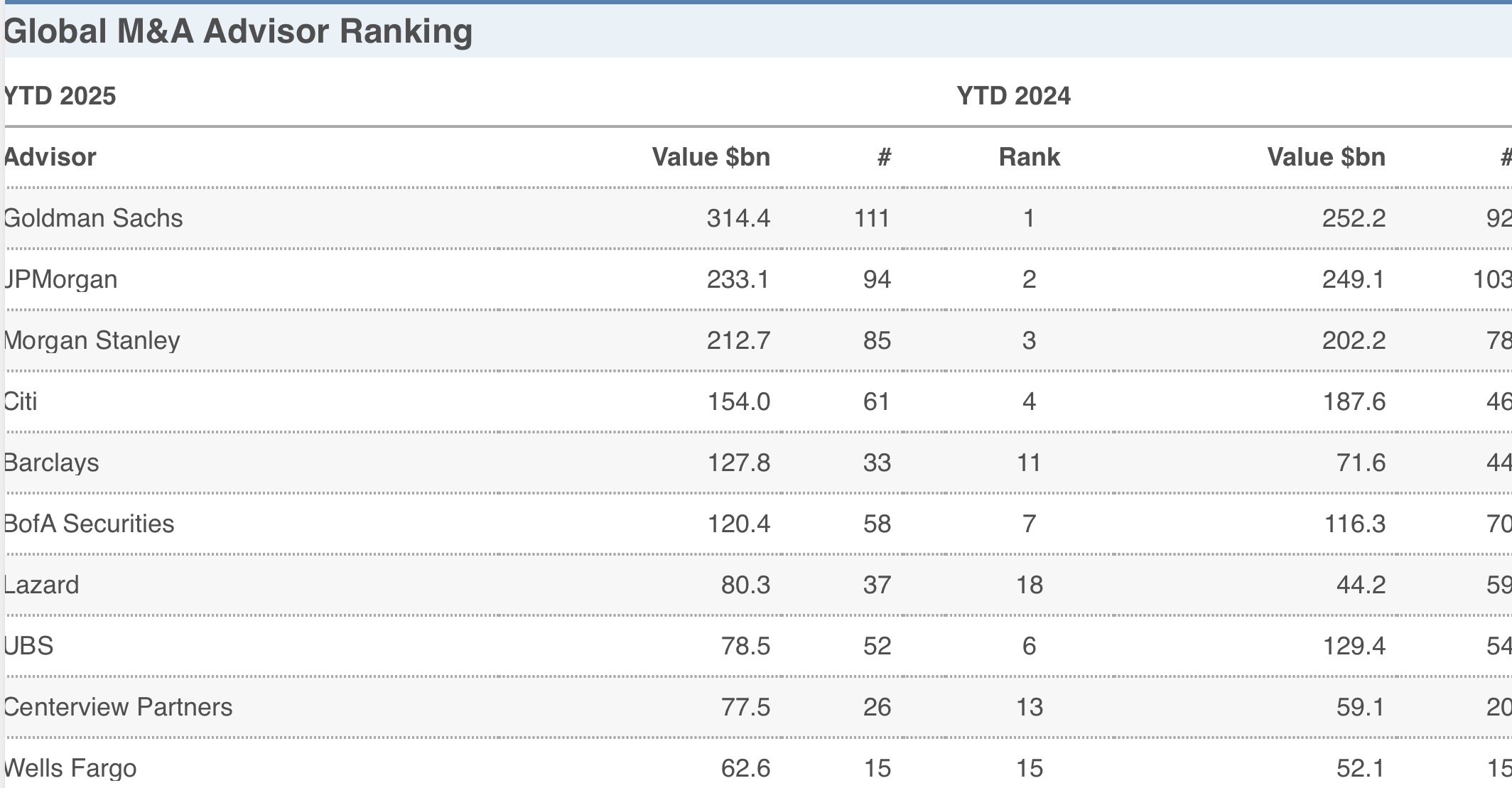

If you look at league tables, USA UBS has had its strongest quarter in years, if you check Bloomberg it's top 10 and on the merger market, not sure why lower on deal logic by so much with deal attribution. The UBS platform is doing worse compared to last year in the other regions. UBS is traditionally stronger in Europe and Asia but those franchises have lagged. With all that said, it's one quarter: a strong US quarter doesn't mean the US franchise is strong, and weak European and Asian quarters don't mean the European and Asian franchises are weaker. LTM data is more helpful, and shows correctly that America's is the weakest by far franchise.

Super interesting quarter from UBS for sure though; lots of worrying signs in the Americas too since the flow came from only 3 or 4 coverage groups (consumer in particular had a great quarter with Celsius and Walgreens deals and drove a lot of the banks flow for the quarter) having any notable deals, but worrying signs in Europe + Asia.

For basic data points from Bloomberg, unarguably the gold standard of all financial tracking in the finance industry:

Global M&A LTM: UBS is 7th with an EV of 81 Bn across 47 deals, just behind CVP and above Lazard in EV

US M&A LTM: UBS is 8th with an EV of 56 Bn across 16 deals, just behind WF and above Lazard

The numbers for revenues are all estimates at this stage, revenue numbers can only truly be known once banks report quarter-end data. Would treat it as absolutely useless/not worth noting. As mentioned, the strongest quarter in a very long time for UBS M&A in the US, much more worrying signs elsewhere (UBS is usually t10 globally or close to it globally, despite being outside the top 10 in the USA for context).

To summarize: UBS has had the strongest Q1 in USA M&A in a long while, and certainly since the merger, the performance in other places has been less than stellar.

Reporting is different for every source it’s not universal.

TMT franchise is essentially irrelevant and seems heads of IB prefer getting fired than making meaningful changes on the team

MV has clearly failed in his goal of making UBS a top 6 USA franchise and he isn't willing to adapt. He's probably getting fired and someone new will come in to get to that goal and/or that goal will be abandoned. I think realistically next guy will probably scale down goals; the Americas remain the main region UBS can grow the most in both in IB and WM + will help them truly become global as they don't have a truly elite IB or WM franchise in the region.

I think the advancements in certain groups (particularly Industrials, Consumer, and LevFin) have happened which is a good positive, and the next person will have to fix the problematic groups in TMT and FIG in particular which should solidify UBS as around a bottom of around top 10 franchise in USA IB.

Why is FIG problematic?

Damm - aren't these IB revenues in generally very low? Calibrated with the figures I know from my MBB (extrapolated to yearly figures) and always thought bankers would clip much much more fees.

No because these numbers are only a estimate based on the small number of deals that they can even estimate this on/have disclosed fee numbers. Put in other words, these have almost no relevance. We will get actual IB revenue numbers when banks report and those numbers will more likely be more in line.

Based on firm size, Jefferies having more IB rev than UBs is wild

How is this shocking? Those firms have been in the same range in M&A transactional fees in a while and smaller deals pay higher percentages? again the actual numbers here are very likely off, but Jef should have slightly higher fees than UBS for this quarter both globally and in America given the difference in average deal size.

Isn't Jef one of the larger firms in the US, at least in terms of number of MDs, and unlike UBS actually covers all groups (UBS doesn't have energy)? They also do LevFin and ECM, they are almost a full-service bank. Idk if they do DCM, but UBS also basically doesn't do DCM anyways in the region.

I am just curious, not trying to be a narc on this dude since he seems to be a fairly reasonable person. I am not sure if this one ED, who usually comments on UBS, hates or loves it. Dude has posts that are clearly just UBS hate train comments like some teams are completely useless, a long ass thread about why WF is much better, but also regularly gives data on UBS that makes it look less shit than what some others on this forum claim. Also, almost every claim he makes includes some kind of random sneak diss on UBS leadership and the fact that he has those long threads against/random attacks against MV and some groups means no way it's HR controlled, so I'm curious what is happening here.

I am assuming the same guy, given the title, WSO ranking, and the fact that he said he was ex-UBS and on garden leave explains the depth of knowledge on UBS and also all the commenting specifically on UBS.

Weirdly negative about tech and FIG so probably from one of those two groups or from a product group supporting one of those two groups.

I think the truth with UBS is that it’s complicated. Some parts good some parts bad and a lot of infighting and turf wars to try to gain control and influence of new and evolving power structures.

Makes sense; I have also noticed that his commentary on LevFin specific things tends to be more technical/thorough than some of the coverage stuff, so maybe he is a LevFin or product guy that has worked with those sectors(?). Again not sure, definitely have noticed a dislike of tech and FIG as well, but not sure if that's just because the data he is citing shows that or because of an actual dislike. Also is possible he is only giving data that gives us negative perceptions of those groups, though on purpose. Just wanted to ask because I was curious as to what his actual deal is; I mean, I am pretty confident dude hates UBS but wanted to understand where specifically I should take his views as being correct vs. where I should perhaps be more wary of what he is saying in terms of bias.

Lmao Swiss regulators are gonna cap UBS IB so we’ll never be able to use balance sheet for deals

Lots of good culture legacy UBS people quitting post bonus. If the regulations go into effect there is a 0% UBS ever gets to top 6 in the Americas.

Plus will probably cause a lot of the senior LevFin bankers to leave. Everyone prepare for the 2026 rebuild phase!

Feel bad for all the incoming interns and FTs who are being misleadingly told that everything is going great and the future of the bank is bright

From my friends at UBS; afaik the ones in bad groups are telling the incoming how bad it is during placement. I feel really bad for any incoming SA's or FT's that end up at any of the bad groups, which tbf seems like most of the groups.

Rem facere ut dolores laboriosam quis aliquam perspiciatis. Ea veritatis labore voluptatem assumenda vero. Dolorem odit corporis explicabo velit quasi enim. A aliquid natus illum molestiae non.

Voluptatem enim dicta quaerat quisquam est ab ad doloremque. Consectetur tempora est iure. Quia voluptas veniam saepe aliquam aut exercitationem. Qui ad et et perferendis quo. Vel delectus voluptas voluptatem.

Aliquid error voluptatibus debitis vel ipsam a ea. Deserunt commodi est enim similique ipsam placeat quisquam. Sapiente qui ut veritatis quo quae deleniti. Ab ratione sunt eum voluptatem esse explicabo.

Quidem exercitationem eum eum voluptatem qui qui quia sed. Rerum eos sequi qui ut ipsum non modi. Voluptatibus ut deleniti quasi molestiae. Ullam neque dicta deserunt aperiam rerum rerum.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Quia error dolorem voluptate autem cum praesentium quae. Itaque eum labore quia consequatur a ea minima similique.