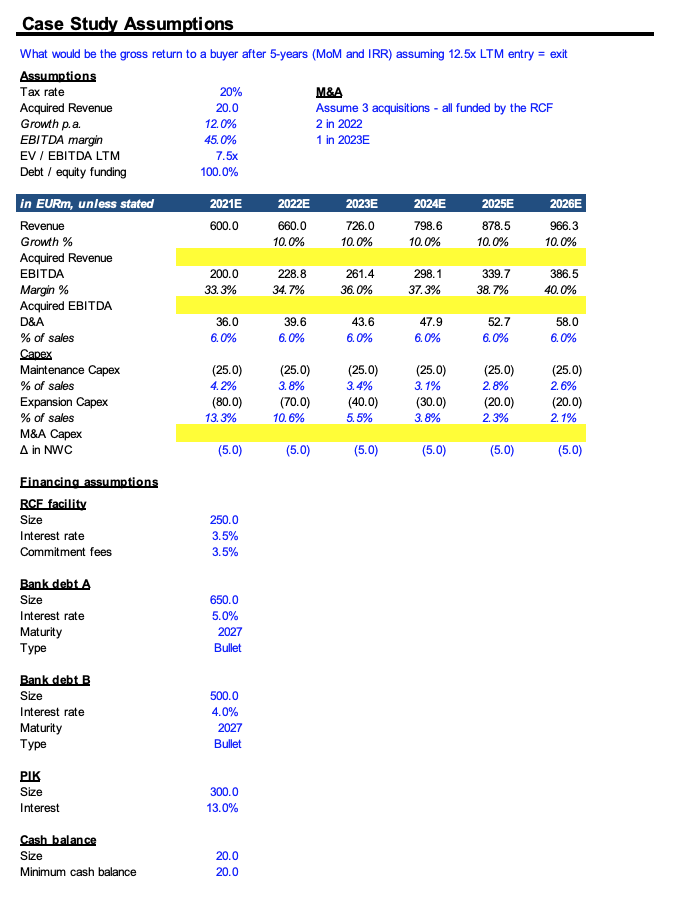

What would be the gross return to a buyer after 5-years (MoM and IRR) assuming 12.5x LTM entry = exit

Anyone know how to go about this? I have the below as a starting point for this question. Many thanks!

Anyone know how to go about this? I have the below as a starting point for this question. Many thanks!

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

Solve for LFCF, then calculate equity value at exit: MOIC: 2.85×, IRR: 23.3% per annum over 5 years

thanks! do you mind if i dm you my version

wait how can you have 2.85x and 23.3% IRR in 5 yrs, that doesn't mesh?

Doesn’t it? 25 is 3

Ebitda*multiple - Net debt - mgmt options proceeds = equity value to common

That times sponsor % = sponsor equity value

That divided by initial check = moic

Net debt = net debt at close - total cumulative levered FCF which you’ll have to calculate + any new debt raised during hold

Took brief glance looks like you have pik which will accrue at 13% to the BS include that in net debt

thanks!

yea i was just confused if the assumptions were for the m&a or enty multiples for the company. confusing how to read them. also debt not paid off if exiting in 2026 but bullet payment 2027

no options proceeds etc in this example but see what you mean

how come the numbers don't match any of the assumptions? were the numbers given to you and you need to just fill in the yellow rows? curious what your final model/summary looks like!

these were provided

I did this as a practice and ended with 32% IRR / 4.0x MoIC. For M&A Capex I just used % of acquisition sales that equaled the sum % of maintenance and expansion capex from core revenue. Curious to see what others do, 2026 EBITDA is 386.5 + 41.0 acquired.

386.5+41 is also MS M&A VP1 all in comp last yr

?

Earum atque dignissimos voluptatem deleniti quod rerum. Reprehenderit at libero molestiae inventore iusto. Cupiditate omnis voluptatum harum omnis ducimus et eligendi. Dolorem error dicta recusandae unde tempora magnam et. Atque molestiae optio facere aspernatur placeat est amet esse.

Consequuntur sint non voluptatem ipsam et. Rerum voluptas animi ducimus quisquam ducimus autem natus. Nam adipisci optio pariatur perspiciatis voluptates velit. Quo officia ullam excepturi consequatur laudantium.

Ex quam ullam voluptatem quas quia deserunt aut sed. Magnam unde harum quas non exercitationem. Nihil molestiae sequi ut laudantium ea. Odit suscipit in expedita iste modi voluptatibus aperiam. Ut eligendi illo eaque aut. Omnis autem ut accusantium quod.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...