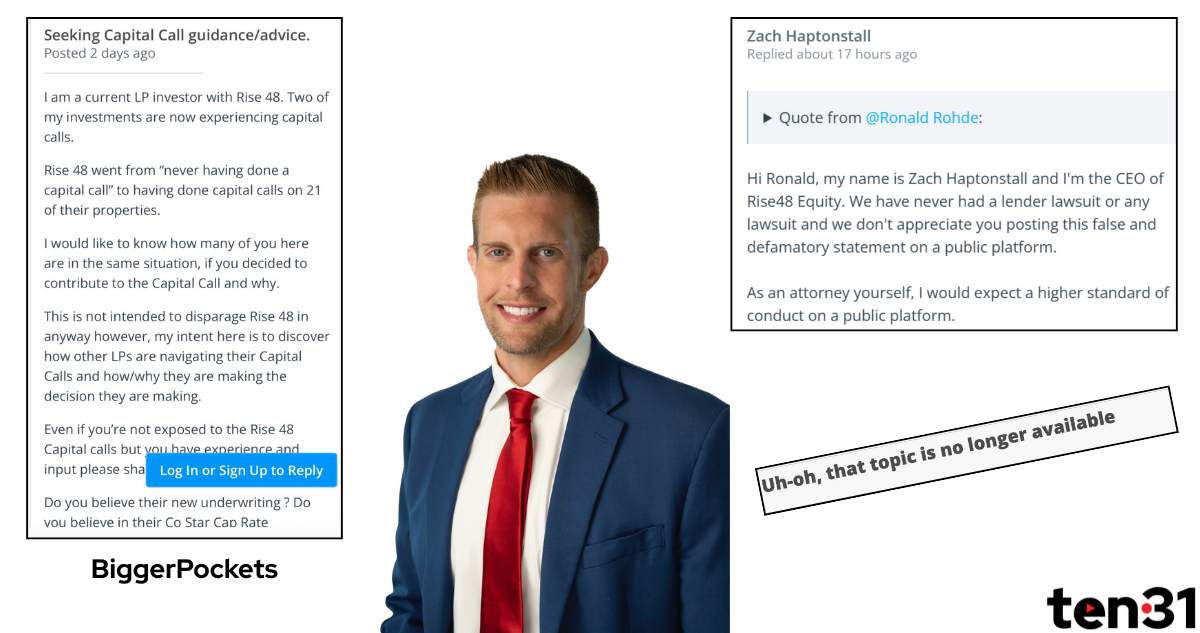

Anyone been following the soap op going on at BP with Haptonstall and the Rise48 crew?

Someone who described themself as an LP of syndicator Rise48 hit up BiggerPockets last week. “Two of my investments are now experiencing capital calls ☎ ,” the user wrote, seeking guidance about Rise48’s underwriting and whether or not others had met the capital calls. He shared investor comms in which Rise48 said “we funded the debt service shortfalls and did distributions to investors out of cash reserves as we thought we had plenty of runway for rates to come down. We thought we could outrun the market by renovating the interiors and pushing NOI.”

Things moved fast & furious, w/ Haptonstall (or at least someone w/ his username) stepping in to respond to a flurry of commenters and warning them that false statements would be met w/ legal action 💼 The thread was unavailable for a time yesterday, but looks like it’s now back.

The BiggerPockets drama surrounding Rise48 and Zach Haptonstall has certainly caught attention. An LP (limited partner) raised concerns about capital calls on two of their investments with Rise48, questioning the underwriting and seeking advice from the community. The LP shared communications from Rise48, which revealed that the company had been funding debt service shortfalls and even distributing to investors from cash reserves, under the assumption that interest rates would drop and their strategy of renovating interiors to push NOI (Net Operating Income) would work.

The situation escalated when Haptonstall (or someone using his username) entered the discussion, warning commenters about making false statements and threatening legal action. The thread was temporarily unavailable but has since been restored. This incident highlights the growing scrutiny and challenges faced by syndicators like Rise48, especially in a volatile market environment.

Sources: Page to log into your Wall Street Oasis member account., Tides Equities?, BREAKING TIDES EQUITY/AMC - EMAIL LETTER REVEALED, Multifamily Property Management Firm in Phoenix- Fraud in play, Tides Equities?

Thread has officially been taken down twice now (maybe permanently)?

All I can say is that Zach's responses were not surprising. He's so predictable...

Sí, he estado siguiendo el caso y definitivamente es una situación que refleja lo frágil que se volvió el modelo value-add con tasas bajas y expectativas agresivas de NOI. Lo que compartiste encaja con lo que muchos están viendo: estructuras demasiado apalancadas, demasiado optimismo en las proyecciones de renta, y un uso excesivo de reservas operativas para cubrir distribución y servicio de deuda, lo cual es insostenible cuando el mercado se enfría.

Looks like it's down, would have loved to read that thread. Zach's aggressiveness now on multiple threads shows his real character. One of the most deceitful characters in the syndication space. Biggerpockets shouldn't promote false statements but there's clearly distress throughout majority of their portfolio and BP should do a better job protecting LPs.

Haha guy who posts on LinkedIn everyday not good at large-scale real estate investing whaaa?

From what I can gather, he’s a great salesman, not an operator. When you partner with anyone in real estate, I’ll take the operations guy 10/10 over a charismatic sales guy.

I thought the bigger pockets guy was a retail syndicator too.is he in trouble?

If you're talking about Brandon Turner, I don't believe he's associated with bigger pockets anymore. But yes, his investments are also very much in trouble.

BeardyBrandon!? Impossible. No one with a beard that long and shaggy could possibly be a failed syndicator. If he strokes that thing enough times in a video, it’s basically the equivalent of a mastermind.

I didn’t realize he left bigger pockets

Rise seems to be using something called Strategic Lawsuits Against Public Participation (SLAPP) to silence LP's and keep them separate. 34 states including Arizona have anti-SLAPP laws. If some LP's were able to come together, I wouldn't be surprised if they could make the case that Rise is using SLAPP to violate their freedom of speech. If LP's can prove that Rise is doing this to keep them separated, so that LP's don't know the extent of the poor performance of their portfolio, I imagine it could be a pretty substantial lawsuit. Perhaps they could re-coup their equity this way lol

@Multiverse : Caught some of the action on The Promote, after the first time it came back up - here

Like many operators, we faced short-term headwinds on assets acquired in late 2021 and 2022 during the sharpest interest rate spike and largest new supply wave in modern multifamily history.

Those challenges are now largely behind us. We’ve successfully recapitalized all loans and are working on improving the property performance and executing our business plan as supply challenges dissipates and the market improves.

We’re proud that throughout this period, we never missed a single debt payment to any lender, nor lost a dollar of investor capital. With interest rates trending downward, concessions tapering, and new supply meaningfully declining in our core markets, we’re extremely well positioned for the next phase of the cycle.

.

Extremely well positioned with assets bought a 2.5% cap rates?

"nor lost a dollar of investor capital"... lol

You've lost all of your investor's capital. The only thing that you're doing now is prohibiting them from being able to write off the lost capital. Not only that but you've lost the preferred equity that you were just raising. Your portfolio is so far gone, it's not even funny. We're talking 50% declines on your PHX assets based on actual sales comps now. Props to you for being able to find an endless supply of clueless investors.

This seems like it has to be the case, but I don't understand how none of the properties have gone to foreclosure. Is he just making debt service with equity from new investors? are banks just willing to extend and pretend to avoid the inevitable?

Hey Jeremey,

Please provide updates on the following properties.

Thx

Rise at the Preserve - NOI DSCR of 0.64x w/ pending maturity 07/26

Rise Canyon West - NOI DSCR of 0.55x w/ original maturity on 05/25

Rise North Mountain - NOI DSCR of 0.57x w/ extended maturity of 04/26

Rise at the Palms - NOI DSCR of 0.45x w/ extended maturity of 05/26

.

Thanks for reaching out and for the thoughtful questions. The third-party reporting you’re referencing is inaccurate and does not reflect the loan restructures we completed in the first half of 2025. As mentioned earlier, we successfully recapitalized each of these assets by purchasing new interest rate caps at lower strike rates and depositing significant interest reserves with the lenders to cover any shortfalls. As a result, all these loans are extended into 2027 and 2028 and are cash-flow positive with the reserves we’ve raised.

Below is the accurate data as of Q3, 9/30, reflecting the updated interest rate caps and reserve structure:

Rise at the Preserve

Rise Canyon West

Rise North Mountain

Rise at the Palms

The DSCRs shown in third-party databases do not account for the new caps or the funded reserves and therefore materially misstate the current risk profile of these loans.

Just want to say I appreciate you actually responding to my questions.

Y’all are between a rock and a hard place on the 21 & 22 vintage buys, but I do respect your willingness to engage and provide updates to the servicer commentary. And, for what it’s worth, your team does seem to be handling the bumps with significantly more composure and maturity than most Covid-era sponsors.

My last follow-up - do the modified rates & quoted DSCRs include any form of spread deferral / PIK interest accrual?

I am trying to understand

Can you explain how your properties with DSCR under 1 (despite prepaid interest and having bough in the money temporary rate caps) are "Cash Flow Positive" by your definition? From the outside, this just looks like a ticking time bomb though you've been more successful than most kicking the can down the road.

Also, how are you paying for these in the money rate caps? Are you using new cash flowing acquisitions (and acquisition fees) to subsidize older properties so they don't get foreclosed? Are you just charging higher fees on newer properties (to newer investors) to help subsidize your underwater older portfolio (e.g. suspending your fees on older properties)?

If this is true, while technically not a Ponzi (since older investors are not getting distributions and may never even get their capital back), it is still new investor money being used to shore up old investments.

Also, you were offering 18% preferred equity through capital raisers a couple of months ago (who one assumes also make a cut). Do you think from the outside that looks like a sign of a healthy sponsor?

They are putting in more reserves (equity) to hold afloat and negotiate new interest rate caps (the 4-5% he mentions above). This is included in the DSCR, thus you can see that they are still not meeting debt coverage consistently above 1x even accounting for the additional equity / interest reserves they injected.

Nevertheless, this keeps the portfolio more or less afloat, but the recently 18% pref raise investor equity is already wiped out / severely out of money.

.

.

Regardless of how we feel, you have to admire their fundraising game. They keep acquiring (overbidding others on) stuff fairly aggressively and collecting those 3.75% acquisition fees. Not sure how they find people to give them money given their terms and their record.

So long as those millions in acquisition fees keep coming in they can keep prepaying interest and then supplement their debt service.

"We ArE CaSh FlOw PoSiTiVe AfTeR wE PrEpAy AlL OuR InTeReSt PaYmEnTs."

0.91x DSCR lol

I want to believe the people responding on behalf of these type of firms are real.

.

You realize that stamping your feet and threatening legal action doesn't allay investor concerns, right? Instead of showing some humility and responding to legit Qs here, you're getting huffy and talking down to people. It's counterproductive. You're probably better off trying to patiently explain where your deals are at and how you intend to work through them, rather than losing it because people are worried.

Yes, people should not make libelous statements anonymously and the law won't protect them if they do. But that's a tiny minority of the stuff being said. Focus on FIXING the problem. @dyer0018

That’s fair feedback "hitsamty and I’ll take it in the spirit it was intended.

To be clear, the goal isn’t to “threaten legal action” or talk down to anyone. It’s to draw a clear line between good-faith questions and false accusations. Those are not the same thing, and they deserve different responses.

I’m happy to engage on legitimate questions, and we do, regularly, with our actual investors. We publish monthly operating reports, DSCRs, reserves, lender status, and forward plans. We’ve held countless investor calls, executed restructurings where needed, extended debt, and used capital calls and preferred equity to fix problems, not hide them. That work is ongoing and transparent to people who are actually in the deals.

What I won’t ignore is anonymous commentary crossing into claims of fraud, Ponzi schemes, or intentional deception. That’s not “concern,” and it’s not productive discourse. Calling that out isn’t losing composure, it’s setting boundaries.

As for humility: this cycle has humbled a lot of good operators across the industry. We’ve acknowledged where underwriting from 2021–early 2022 didn’t survive a historic rate shock. The question now isn’t whether challenges exist, it’s how sponsors respond. Our focus has been preserving capital, avoiding forced sales, protecting senior debt, and maintaining optionality for recovery as the market normalizes.

If people want to discuss where deals are, what’s working, what isn’t, and how we’re navigating it, I’m open to that conversation. Always have been.

But productive dialogue requires facts, context, and accountability on both sides, not anonymous drive-bys or loaded conclusions.

Happy to keep it constructive.

You're right. I've taken down the comment; it wasn't productive discourse and calling it out as such was fair.

If the offer of having an constructive conversation is honest, I would like to engage in that, because a lot of the reporting around Rise48's deals (here and elsewhere) do indicate some distress in the portfolio. I would be very interested to hear how the firm intends to raise NOI at the asset level to achieve positive DSCRs, for example. Some of these assets seem to have been purchased 3 or 4 years ago; can you give us insight into what new strategies the firm plans to put in place to raise rents or cut expenses that haven't already been tried?

.

I'm not understanding what you're saying here.

" As a result, all these loans are extended into 2027 and 2028 and are cash-flow positive with the reserves we’ve raised."

"Cash-flow positive with interest reserves in place"

Are you considering raising let's say $600,000 in new equity and then putting it into an interest reserve a positive cash flow event because you will eventually get the money back in some form?

My AI-radar always goes off whenever I see a pithy clapback in the form of 'that's not X, that's Y' (eg, 'that's not negotiation, that's blackmail'). It's deflection and the spinning of a rhetorical strawman. FYI, I have no insight/input into the actual substance here, just making an observation on the style of writing that's clearly been through the AI machine.

veiled cease and desist threat incoming

100% - the guy went through a 3-step process there. 1. Pen some angry thoughts 2. Run it by the lawyers 3. Run it through GPT

I have to call BS here

These projects/loan are temporarily cash flow positive due to lenders working with you BUT are all at rates that are above where these deals would be refinanced in the near term.

So yes, right now they are "fine" but what happens when that next refinance event happens and your equity is unwilling to fund more capital calls.

Because I remember when Rise48 touted never capital calling investors...which they then did.

You are not going to save 2021 and 2022 highly levered Class B- or below Sunbelt deals. The math does not work no matter how you try and spin it.

They will simply raise additional equity which will be placed above all prior equity and the music will keep playing. The real question is, when will be their next disposition? The 2021-2022 properties which will result in lost equity to the original investors and probably partially the additional capital infused, the 2023-2024 assets that are also likely impaired due to poor structuring and are already coming up on their initial 3-year term, or the 2025-2026 assets that still need good NOI growth in a market with flat-to-negative growth. The latter would imply they won't be selling any properties until 2028-2029.

Challenge they just keep adding to their basis with all these capital calls

I really can’t believe this guy came in here saying deals that have a .95 DSCR are fine with rates sub 5%

That comment is so stupid it hurts. Does he not realize with debt higher then 5% and lenders wanting at least a 1.2 DSCR it means he is under water on all these deals without putting more money in.

As long as they can keep raising capital for these deals to pay interest payments, lenders won't really care. It's when they can't raise any $ to kick the can and lenders take the property that the cat truly comes out of the bag and all of their lenders tighten on them. At that point it's over.

I don't think this fella should be in this forum lmao. Should be out raising money to feed the inferno.

Well they acquired a ton of properties in 2025 so the 3.75 % acquisition fees alone mean almost $8 million more for them regardless of performance.

Every broker in Texas knows they are the guys who will over pay

Are any of these new deals any good?

I mean the fact they keep feeding the machine is impressive

How do they get people to pay 3.75% acq fee? Seems extraordinarily high, but I don't work in REPE. What's a regular rate and is it common to have these charged on top of mgmt fees..?

The Acq fee is one time at the time of acquisition. I would say 1%-2% is typical for a normal deal (Even Grant Cardone is 1% in 1% out), but the economics of syndicators can get up there. I've seen 5%+ on some packages, which is insane to me.

Just piggy backing off this. All fees are sort of size specific in the industry, I’d say. For $50M+ which seems to be the type of deals they are doing, 3.75% would be on the VERY high side. But just because one firm charges 3.75% and another charges 1%, it doesn’t mean the 3.75% firm is more egregious than the other. There are tons of ways that a GP can “skim” money off the top. Yearly asset management fees are one way. Another way that I can think of is by over estimating the rehab budget and taking a cut there. Some funds even pre-buy deals (maybe they argue they can close quicker and get a better deal by making an all cash offer to a broker) and then sell it back to their own fund, then they look like pretty good for only charging a 1% acquistion fee.

In ground up construction, sometimes they act as the GC and secure the majority of the profits on the front end. Maybe tell investors that they are building 300 units at the cost of $230,000 a unit and it really only costs $190,000 a unit. That way, they’ve already made $12Mbefore the project is even sold.

That’s on purchase price??? At 65% LTV that’s literally 10% of equity that goes directly to the sponsor for no reason lol

Welcome to RE where it's great to be the manager, terrible to be the investor. Just buy public REITs unless you are doing the deal yourself (minimizing fees).

Now they're trying to cross collateralize 18 properties for a high six mortgage and DSCR around 1. Anyone have more details on this? Would be curious how many performing properties they're throwing into this dumpster to keep extending and pretending.

I haven’t heard anything about it but I have seen other sponsors get in trouble for cross collateralizing deals without investor consent. Maybe rise has latitude in their docs to do this.

S2 was just in the news for their upreit needing a large equity injection. The upreit is a better structure but the assets were impaired going into it.

Not sure if you're re to this, but they've been raising rescue pref for their own deals. Target for this 1,400-unit portfolio was $39M, out of which $14M would be paydowns, $12M for rate caps etc. Here's a snippet from The Promote piece about a year ago.

So I’m assuming this would be a SASB deal?

This is different from their rescue pref fund. It's not done yet either as they're asking the investors in the 18 deals to sign off on cross collateralization.

Deals include both Arizona and Texas properties.

UPDATE: They got investor approval to do this - saw the video from Haptonstall. Closing of the new sr. is expected late March/early April apparently

x

Repellendus aperiam aperiam praesentium quia ipsam. Occaecati at corrupti numquam quod. Ullam facilis perferendis rerum. Molestiae sit quasi est a. Nostrum doloremque sed fugit reiciendis dolorem aliquam autem.

Dolor provident enim eaque aut reiciendis deserunt. Odio ut atque provident officia ipsa labore et. Quasi nulla doloribus minima id facere consectetur.

Quia quasi ut earum labore qui omnis dolorem. Reiciendis a inventore necessitatibus ipsam ab. Est consectetur quasi voluptatem minus soluta tempora.

Tempora autem voluptas fugiat porro provident quia architecto. Quia eos eos cupiditate sint officia quia reprehenderit sapiente. Maiores est minus in itaque vitae. Aliquam sint iusto sed et deserunt sequi. Aut est recusandae itaque beatae alias voluptas quod. Expedita rerum doloremque porro dolores ipsa accusantium et.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Dolore soluta molestiae numquam et aliquam ea. Itaque expedita molestias consequatur inventore et tempore excepturi. Eum aspernatur ut quo voluptatem. Qui vero at consectetur optio. Expedita reiciendis eius incidunt deleniti.

Aliquam voluptatem consequatur aliquid sit architecto doloremque non at. Qui repudiandae facilis saepe aliquam.

Ut sint sed officia exercitationem omnis enim. Nihil dolores quis magni perspiciatis quo. Quod debitis iusto doloribus molestiae.

Labore repudiandae enim accusamus. Aut fugit voluptatem velit quia. Incidunt dolor voluptates illum distinctio autem.

Facere expedita enim nemo necessitatibus quia voluptatibus. Temporibus dignissimos neque ad molestiae vel adipisci ut. Aliquid voluptas illo necessitatibus eum enim distinctio vero.