My sixteen-year old, a sophomore in high school, joined the investment club at school a couple of weeks ago, and entered a stock-picking competition. Club members invest in a stock or stocks of their choice, with the winner chosen in about five weeks,

based upon price appreciation. Thinking I would have some sage advice on where to invest his money, he asked me for some stock picks and I almost suggested that he put all his money in GoPro, a choice that is clearly at odds with the prudent investing practices of diversification and perhaps with conventional value investing precepts. While GoPro is not the investment I would recommend for my son as his Roth IRA investment (with real long money and a long time horizon), in a game with a five-week window, where the winner takes all, momentum will beat out

intrinsic value and diversification will be more hindrance than help. (Note that momentum fairy was in GoPro's corner at the time, and has taken a break in recent days.) In this post, I take a look at GoPro, perhaps the hottest stock of the year, with the intent of not only understanding its intrinsic value (and drivers) but to make sense of the pricing game.

The Back Story

For those of you who are not familiar with the company, GoPro makes cameras that you can attach to yourself and record video of your activities. While that might not seem exceptional, it is designed for high-energy physical activities, including running, rock climbing, swimming or hunting. You can get a measure of the company’s current offerings

on its website. They include three models of the camera (the Hero, the Hero 3 and the Hero 4), numerous accessories and two free software products (a GoPro App and GoPro Studio) to convert the recorded videos into watchable ones. The company believes that the creators of videos will share them, not only with their friends, but also with the general public. In its

most recent earnings report, it noted that GoPro videos published on YouTube had increased 200% over the previous year, launched a GoPro channel on Pinterest to attract more attention to the videos and one for the Microsoft Xbox.

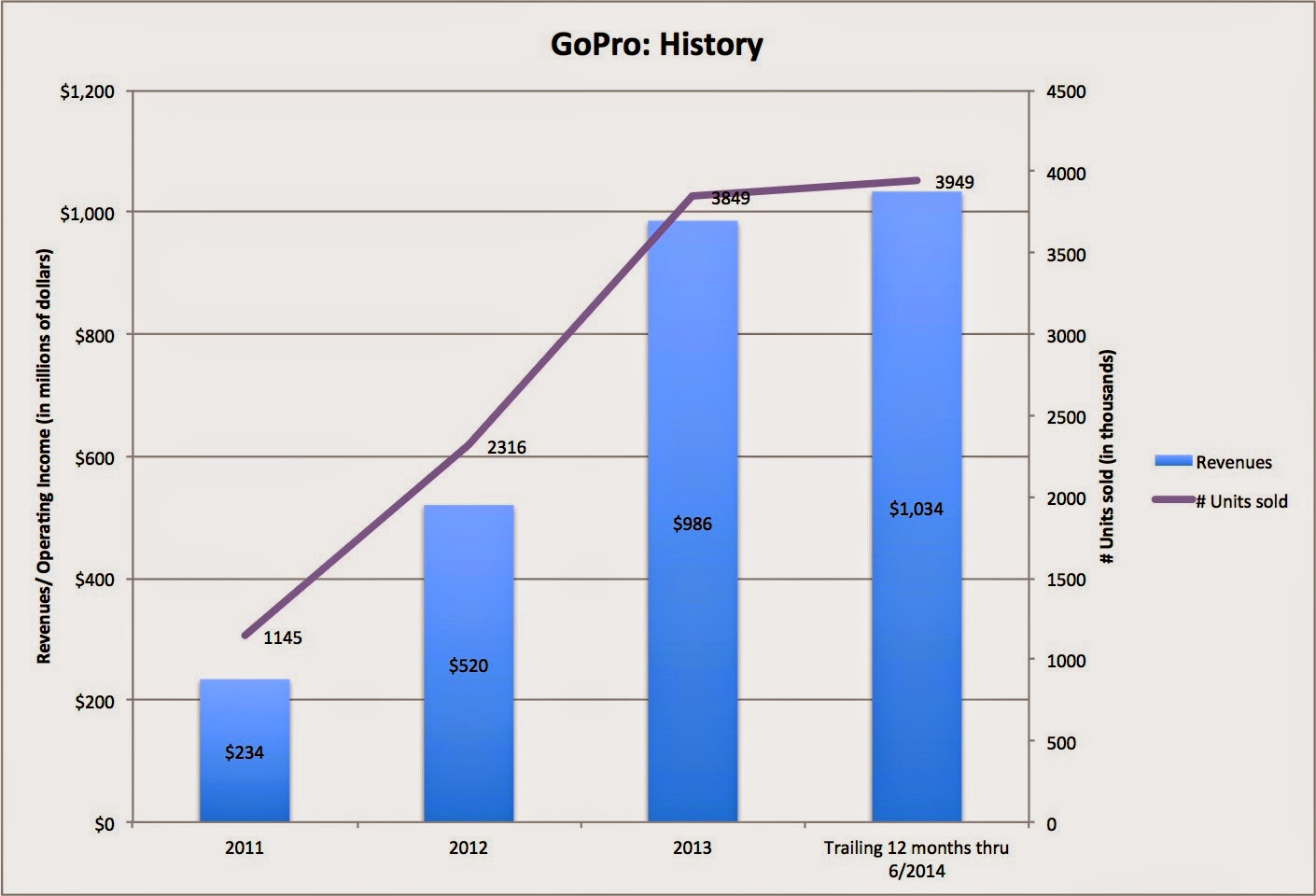

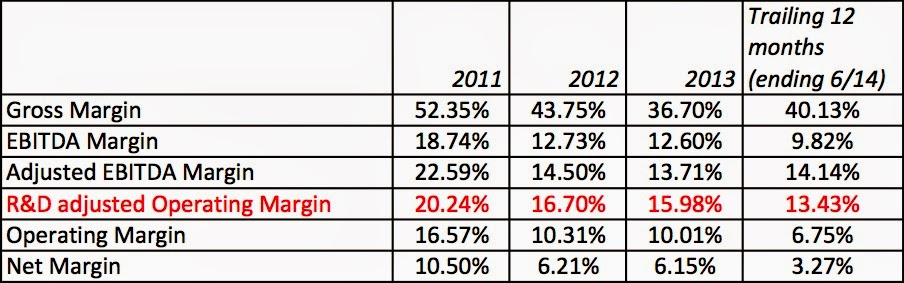

The company’s cameras have found a ready market, with revenues hitting $986 million in 2013 and increasing to $1,033 million in the twelve months ending in June 2014. In spite of large investments in R&D ($108 million in the trailing twelve months), the company still managed to be profitable, with

operating income of $70 million in that period. Capitalizing R&D increases their pre-tax

operating margin to 13.43%, impressive for a young company. The figure below looks at the evolution of revenues and units sold over the history of the company. (You can download the company's

prospectus and its

only 10Q.)

An Intrinsic Valuation

In valuing GoPro, we face all of the typical challenges associated with valuing a company, with growth possibilities, early in its life cycle, in determining the market potential and imminent competition.

1. Potential Market

GoPro is nominally a camera company but I will argue that it caters to a different market. To get a measure of the potential market for GoPro's products, I will make my argument in three steps:

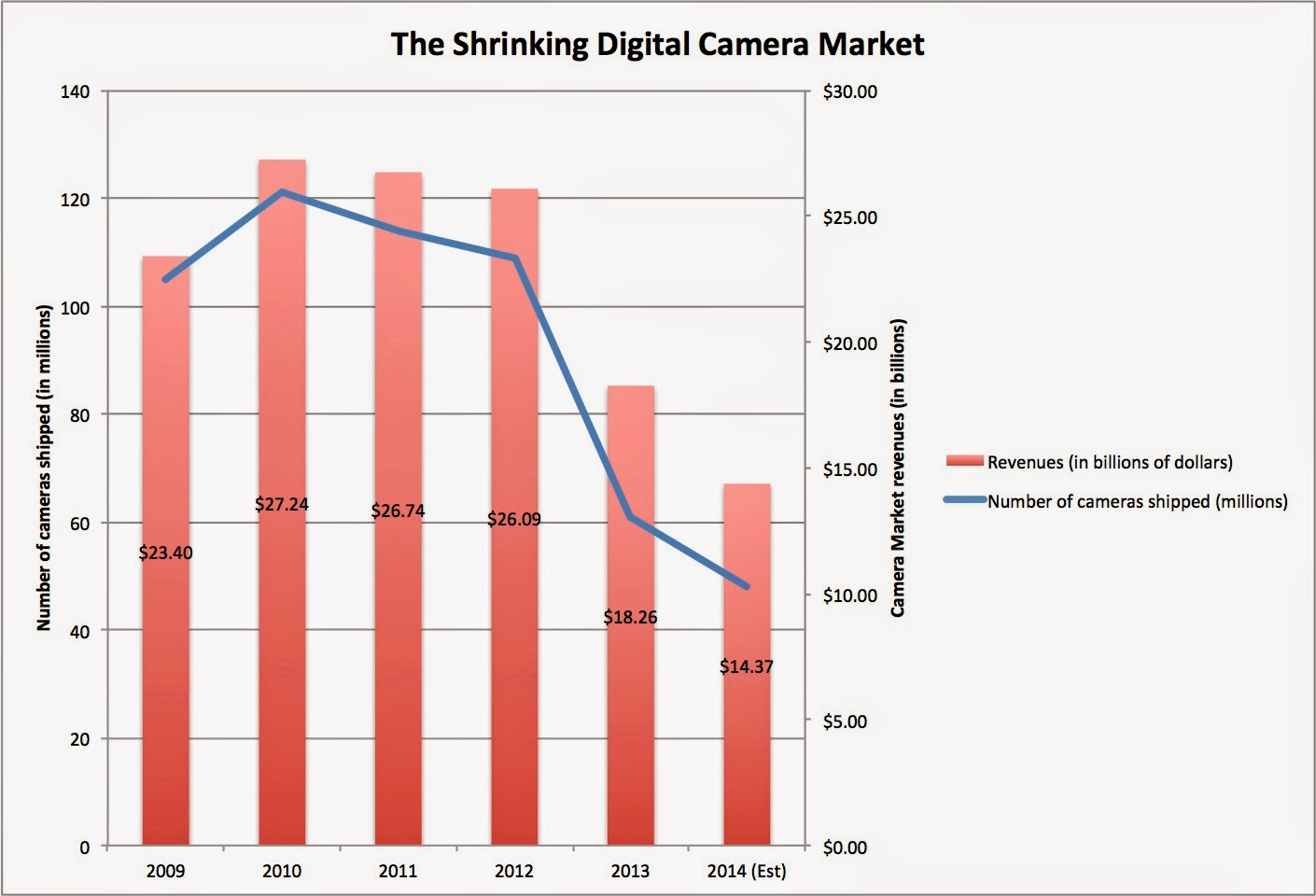

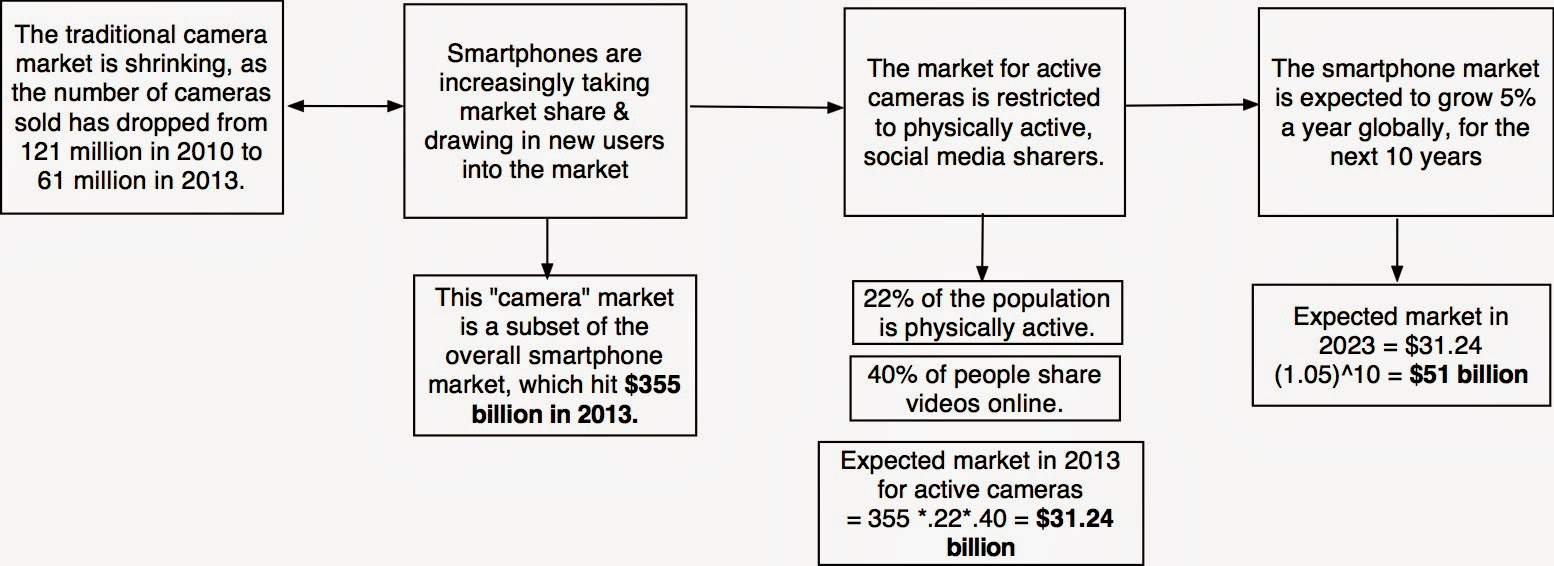

- The conventional camera market is under threat from smart phones, and its share of the camera market has been shrinking over the last few years and there is little hope that it will stop doing so in the future.

|

| Source: CIPA |

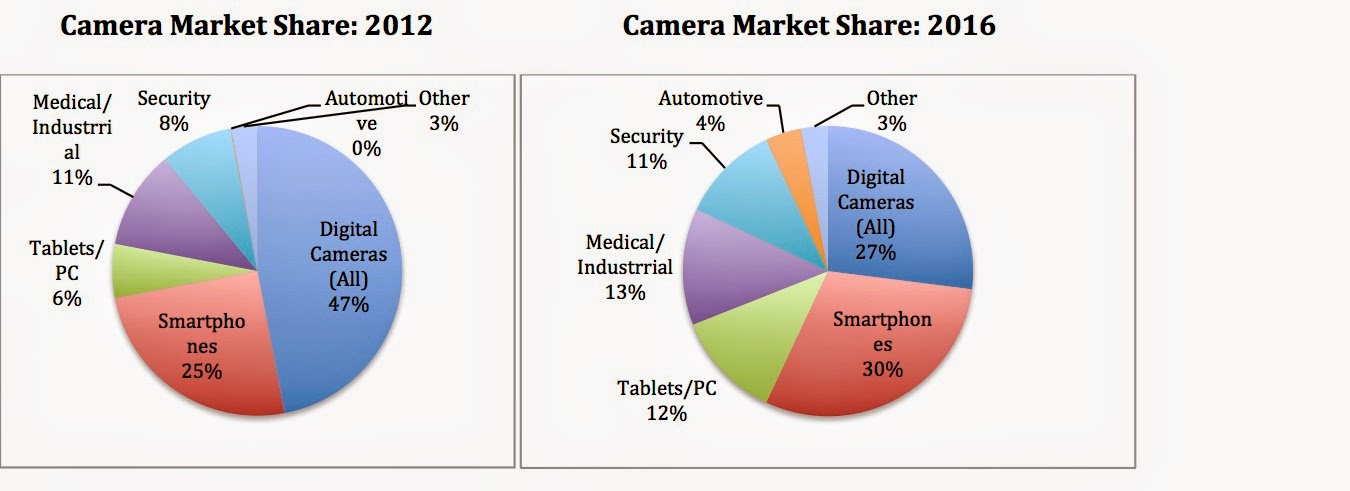

- The camera market is changing and expanding. The entry of smart phone cameras has not only taken away market share from conventional camera companies but has changed the market by attracting new users into the market. These new customers, who are mostly uninterested in conventional cameras (and recording images and videos for family albums), are being drawn into this market, by their desire to record and post photos/videos on social media sites. That trend will continue into the future and I believe that the camera market will become a subset of the smart phone market. The good news is that the smartphone market is huge, estimated to be $355 billion in 2014, larger than the entire electronics market ($340 billion) in 2014. The bad news is that most of the consumers in this market will be satisfied with the cameras on their cell phones and will be unwilling to spend money on an expensive accessory, unless it serves a very specific need.

|

| Source: IC Insights |

- The action camera market will be a subset of the smartphone market and its customers will be those who are physically active people who also happen to be active on social media (over active, over sharers). To make an estimate of how many consumers are in this market, I used the CDC's statistic that about 22% of Americans are physically active. Generalizing (and globalizing) this statistic to the smartphone market yields a potential market that is about $80 billion in 2014 (22% of $355 billion). That is likely to be an over estimate, since not all physically active people are "sharers" on social media. According to this survey, about 31% of adults post videos on their social media site and it has both increased over time and is higher among younger adults (ages 18 through 29), 40% of whom post videos. Using the latter statistic, the overall market for action cameras is $31 billion (in 2013), estimated as 40% of $80 billion. Applying a 5% growth rate on this market yields a potential market of $51 billion in 2023. The picture below captures the sequence of assumptions that yields this number:

2. Market Share & Profit Margins

The market share and target

profit margin that we assess for GoPro will be a function of the potential market that we see for it and the competition in that market. If we define it as the camera market, the competition is already intense and dominated by Japanese manufacturers:

If we define it, as I think we should, as the subset of the smartphone accessory market that wants active cameras (the $51 billion market in 2023 identified in the last section), GoPro is the first mover in the market and has more growth potential (both because the market is growing and it has relatively few competitors, for the moment).

To gauge the expected market share that GoPro can get of this market, it is worth noting that while it initially had the action-camera market to itself, the competition is starting to take form from upstarts, established camera makers and from some smartphone manufacturers. Even if GoPro can establish a brand name advantage (by being the first one on the market), I don’t see any potential networking advantages that GoPro can bring to this process that will allow it, even if successful, to control a dominant share of this market, as the market gets bigger. Drawing from the established camera business market shares, I will assign a market share of 20% (resulting in revenues of about $10 billion for GoPro in 2023, i.e., 20% of $51 billion) , roughly similar to the 20% market share for Nikon, the leading camera maker, of the camera market in 2013. (I am not drawing a direct parallel between Nikon and GoPro, but I am arguing the market share breakdown of the action camera market is going to resemble the market share breakdown of the conventional camera market).

On the

profit margin, GoPro’s

first mover advantage has given it a headstart in this market, allowing it to charge premium prices and

earn a pre-tax operating margin of 12.5%. This is slightly lower than the margin (13.43%) posted by the company in the most recent 12 months, but the trend lines in margins for the company are decidedly negative:

This estimate (12.5%) of the pre-tax operating margin is significantly higher than the 6%-7.5% margin reported by camera companies and similar to the 10%-15% margin reported by smartphone companies; Apple remains an outlier with its pre-tax margin in excess of 25%. I am, in effect, assuming that GoPro will preserve its premium pricing, even in the face of competition.

3. Investment Needs

While GoPro users may post to social media sites, GoPro is not a social media company when it comes to investment needs. While social media companies like Facebook, Twitter and Linkedin generate their revenues in advertising and have little need for tangible investment, GoPro will need to invest in manufacturing capacity to produce and sell more cameras. To estimate the reinvestment needs, I made the assumption that the company will have to invest $1 for every $2 in additional revenues generated in years 1-10. This, in turn, will move the return on capital for the company from it's current stratospheric levels to about 16% in year 10.

4. Risk

GoPro has a social media focus for its user-generated videos, but the company currently generates all of its revenues from selling cameras and accessories. There is the real possibility, though, that the user-generated videos may have entertainment value, which, in turn, could lead to other revenue sources (advertising on GoPro's YouTube channel or a dedicated media outlet for GoPro videos, for instance). That does seem a little far fetched at the moment and we will assume that GoPro's risk will resemble the risk of high-end electronics companies. To estimate a

cost of capital for GoPro, I consider their current mix of debt and equity (2.2% debt, 97.8% equity) as my starting point, and

estimate a cost of capital of 8.36% for the company, declining to 8% by year 10 (with both reflecting the fact that the US 10-year bond rate dropped to 2% on October 14). This may strike you as low, but much of the risk in GoPro is specific to the company and its market and is thus not reflected in the cost of capital.

5. Possibilities

GoPro's focus on creating partnerships with Xbox and Pinterest suggest that it sees the possibility of generating revenues from becoming a media company (with the videos created by its customers as content). At the moment, using a contrast I drew earlier in my post on Uber, this is more in the realm of the possible than the plausible or the probable. If the value per share that we obtain is just a tad below the

market price, this possibility may be sufficient to tilt the scale towards buying but it cannot account for a large chunk of the value today.

6. Valuation

With this spectrum of choices on the inputs (revenue growth derived from the total market/market share assumptions, operating margin, sales to capital and cost of capital), it is perhaps more realistic to assess the value of GoPro as a distribution than as a single estimate of value.

Reading this distribution, you can see while the expected value across the simulations is only $33-32/share, well below the market price of $70, there are outcomes that deliver values higher than the market price.

Put differently, while I think that the company is over valued, there are pathways to values higher than $70. They will require GoPro to (a) expand the market for cameras to new users (physically active, over sharers) (b) find a strong, sustainable competitive advantage over its imminent competition, perhaps with a networking edge (giving it higher market share) and (c) preserve its premium pricing edge.

(You can download the

base case valuation by clicking here)

A Pricing of GoPro

In keeping with my argument that much of what passes for valuation in practice is really pricing, let me make the pricing case for GoPro. To price a company, there are two fundamental questions that have to be addressed: who (or what companies) you are pricing your company against and what metric (revenues,

book value, earnings etc), you will use in the comparison.

The essence of pricing is that you use the market pricing of comparable assets/firms to determine a fair price for your asset/company. There is, however, a subjective component to determining these comparable investments, and that comes into play with a company like GoPro, with the following possible choices.

- Existing camera manufacturers, some of whom (Sony and Panasonic) are much bigger players in the electronics market. (Sample of ten companies, all of them Japanese)

- Leisure product manufacturers, which includes a diverse group of companies that manufacture gym equipment (Life Time Fitness), golf clubs (Callaway Golf) and bicycles (Cannondale), on the rationale that these appeal to the same physically active market as GoPro does. (138 global companies)

- Electronics companies, which includes all consumer electronics companies listed globally. (103 global companies)

- Social media companies, which includes a broad mix of businesses some of which derive their revenues from advertising (Facebook, Twitter), some from subscription-based models (Netflix) and some from a combination (LinkedIn). (13 social media companies)

Stock prices cannot be compared across companies, since they are a function of the

number of shares outstanding. Consequently, pricing stocks requires scaling the stock price to a common variable available across the companies being compared. This variable can be revenues, earnings (

net income, operating

income or EBITDA), book value (book value of

equity or invested capital) or a revenue driver (users, subscribers).

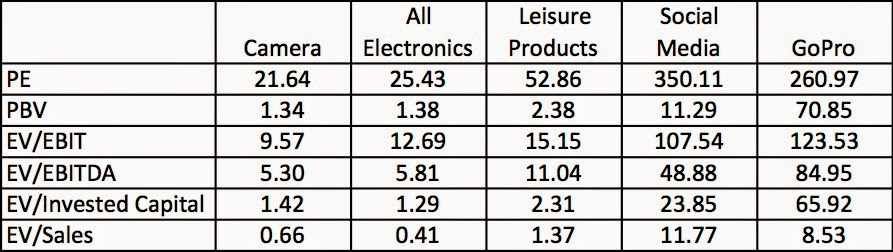

Bringing together these choices, we can compare GoPro's pricing with

that of comparable companies, using different comparable company groups and pricing metrics:

|

| Based on market prices on 10/15/14 & trailing 12-month data |

This is a simplistic comparison, where I have used the median values for the sectors involved and not controlled for differences in fundamentals (growth, risk and cash flows) across companies. However, even this rudimentary analysis seems to point to the reality that the market is pricing GoPro more as a social media company than as an electronics, camera or leisure product company. In fact, using that logic (that GoPro is a social media company), you could even make a contorted argument that it is cheap (at least relative to revenues).

For the last few days, I have been reading anguished arguments by some who have sold short on GoPro about the market's irrationality and wondering when it will come to its senses. Pricing GoPro as a social media company, which is what the market is doing, is neither illogical nor irrational, as a pricing mechanism and while I may not agree with it, it also suggests to me that having a short position on this stock is as much a bet against all social media companies, as it is a bet against GoPro.

Summing up

It is difficult, but not impossible, to justify buying GoPro on an intrinsic value basis. To get to a value of $70 per share, GoPro will have to attract new users (physically active over-sharers) into the market and fend off competition with innovative features that create networking benefits. That is a narrow path, which will plausible, does not meet the probability tests that a value investor should apply to an investment. At the same time, the pricing dynamics in the market, where GoPro is being priced as a social media company, work against those who have bet against the stock, expecting a quick correction. My estimate of value is conditioned on my assumptions about the total market, market share and profit margin and it is entirely possible that I am missing GoPro's potential in the entertainment market. Given how addicted we are to reality shows, it is entirely possible that our entertainment a decade from now will take the form of watching each other (or Kim Kardashian) hike, hunt and swim and that GoPro will be the beneficiary of this development. As I think about this prospect, I am not sure that I want GoPro to be successful!

I'm so short Go Pro I can't go any shorter. It is overvalued and has management that is led by a surfer who tried to donate his shares to charity before he was even allowed. Want to know other issues?

Smart phones are quickly catching up to all the abilities that set GoPro cameras apart. Longer battery life? Durability? Waterproof? HD quality? These are slowly becoming the norms for smart phones.

GoPro is like flip cameras. Will be dead in a few years, especially at a $500 price point.

Laughed my ass off at the first paragraph.

lol, the future sounds terrifying

interesting

Ah yes, camera-on-a-stick. Good thing there's an infinite year patent on said stick otherwise i think this thing would have never went public. Oh, wait.

Future of GOPRO? (Originally Posted: 01/11/2017)

What does everyone think the future of gopro is? There stock performance has been poor for a while. They also had a recall on their new product, the Mavic drone. Is there small line of products contributing to their demise?

I'm long the stock. Bought it at like $11 so my ass is hurting a little right now, but they've had good holiday sales and are shutting down non core businesses. I think there is a lot of brand value (IMO GoPro is like Xerox or Kleenex).

I think it is a pretty good buy at the price. Going to be rocky, but the stock has come up some recently.

I second that. I was a non-supporter for a while, but I believe they will make a comeback. Well said

GoPro (Originally Posted: 06/27/2014)

(Reuters) - Shares of GoPro Inc, a maker of cameras used by surfers, skydivers and other action junkies to record and post their exploits online, rose as much as 38 percent in their market debut.

The company's shares rose to a high of $33 in early Nasdaq trading on Thursday, valuing the company that popularized action cameras for consumers at about $4 billion.

GoPro is the first U.S. consumer-electronics company to go public since headphones maker Skullcandy Inc in 2011.

Videos taken using the company's wearable cameras have made a big splash on the Internet. The company says its videos attracted more than 1 billion views in the first quarter on YouTube, where its channel has 2 million subscribers.

GoPro was founded in 2004 by Nick Woodman, who hit upon the idea while on a surfing trip to Australia. He raised his first funds to develop the camera by selling seashell necklaces along the California coast.

"There probably hasn't been a consumer electronics brand as dominant as GoPro has been in its category since the early days of the iPod or the iPad," Dougherty & Co analyst Charlie Anderson wrote in a note to clients.

Anderson estimates that GoPro has captured more than 90 percent of the action camera market.

Felix Baumgartner's record-setting 24-mile (39-km) jump from a stratospheric balloon was captured using a GoPro camera. That video has attracted nearly 16 million views on YouTube.

Olympic gold medal winning snow boarder Shaun White and 11-time world champion surfer Kelly Slater are among well-known athletes who have endorsed the cameras.

GoPro cameras have also become popular among bands such as The Rolling Stones and Foo Fighters. The company received an Emmy award in 2013 for its contribution to the television industry.

GoPro sold 8.9 million shares, while the rest were offered by selling stockholders, including Woodman and investors Riverwood Capital LP, Taiwanese electronics contract manufacturer Hon Hai Precision Industry Co Ltd and Sageview Capital Master LP.

Woodman, the company's chief executive and its largest shareholder with a 48 percent stake, sold about 3.6 million shares.

Private equity firm Riverwood owns 16 percent of the company while Hon Hai owns 10 percent through its indirect wholly owned subsidiary Foxteq Holdings Inc. Sageview owns 6 percent.

pretty good for a cameramaker.

Ray Lewis should be the company spokesperson.

Jumped in Gopro @ 24 yesterday as apart of the IPO. Friday is payday in more then one way.

Surprised, but not surprised people are buying this crap up. They make money, but the multiples don't make a lot of sense. Especially when you start on a qualitative rant on how they'll get professional athletes, singers, actors, etc. to start wearing the devices so they can change viewers. You'd look like a complete dumbass if you wore this walking around recording your life, so I don't see regular folks buying them up. Heck, if they wanted to, they'd just buy a Google Glass

I saw 2 different people wearing them while taking a Segway tour of Boston when I stepped out to get lunch today. Not disagreeing on the dumbass part though

Maybe I'm not a regular person but I end up doing something fun and using my gopro every weekend. I even took my avatar picture with a gopro. I've got a neat collection of pictures that I've taken with it. Its great for vacations, its practically indestructible and not as expensive as a decent DSLR.

Google glass is much more expensive 1500 vs the 400 for the gopro. I know one person who has ordered Google's glasses when many of my friends have a gopro.

You're buying the leading action camera brand, its like buying the more recent Iphone or Ipad.

I will agree that the valuation was a bit high and the founder really pushed it as a media company. I don't know how well they will monetize that avenue so possibly a lower valuation but I do have strong hopes for them as a company.

Damn, I got in at $45. Can't believe I forgot about this IPO, hopefully it jumps up again.

Shorting GoPro (Originally Posted: 07/01/2014)

Thoughts?

What's the rate? Wouldn't think there's a lot to borrow with everyone else trying to short it

just retract the pole attached to the gopro, done

i take it you're a short person too ? would explain it

I'm not really sure what this company does once waterproof smartphones become industry standard.

hey, people still use Polaroids, GPRO could survive!

Don't agree with this at all.

1.) Even if the smartphone is waterproof, I doubt you want it getting banged up 2.) Go Pro has a built in stabilizer, which is why its footage is so smooth and crisp. It's not just a smartphone on a pole

It's definitely a "niche" market, but a big one for sure. Frankly, it more or less created the space it's in and now dominates it.

What exactly does GoPro have patented? Is there any significant barrier to entry for large electronic manufacturers. I don't really know too much about the company at all.

Edit - As a point of reference, I have tested all the majors and again GoPro is hand down the best. Everyone I know in industry (action sports) uses them and unless Sony (or another mfg) is throwing a marketing budget behind you (IE - TGR with their Sony's Mind's Eye Segment) not many people use another product.

The barrier to entry for now is their brand imho. The product is used on every large extrem sport event. XGames, Surfing contests, Extreme Skiing, Red Bull events, and many many more. GoPro kind of reminds me of Red Bull. Their product isn't real superior to other energy drinks, but by sponsoring all those crazy sports events, they just created an "energy drink = red bull" thinking, just like "action cam = GoPro". I might be wrong and people might stop buying them, but right now, their brand value is incredible and the product is actually quite sick.

I might be old-fashioned, but this is one of the few hyped tech companys in tech IPOs that actually builds something instead of offering another stupid mobile game. But we'll see..

On a side note, I was skiing last winter in Austria and Switzerland, and the number of GoPro cams on ski helmets is incredible. Kind of reminds me of the time when everyone started to use iPhones.

http://www.reuters.com/article/2014/06/26/us-gopro-ipo-idUSKBN0F11RS201…

I'm normally all for shorting high multiple tech... but this seems like one that will actually work. Great product. Super strong brand awareness already. Huge potential markets. And at the end of the day, don't the own the content?

A short thesis is not simply "I think this company will eventually go bankrupt" or "I believe this company will under perform over the next few earnings cycles"

Nice call bro

Good luck my friend; as long as the music is playing, everyone will be dancing.

I actually love their camera.

That being said, do the math on how many cameras they need to sell to grow into the current valuation, it will astound you.

Gopro is being marketed as an entertainment company that is supposed to makes money off royalty. Its users submitted videos on youtube, vimeo etc. have generated many hundreds of millions (and rapidly increasing) of views and the idea is that Gopro would get a cut from the advertising revenues generated by these videos. That would translate into a lot of pure profits. It is very similar to BEATS headphones (or for that matter, Red bull energy drinks) in that they are in the business of making products that can become easily commoditized but are nonetheless priced for their social media prowess and strong brand recognitions.

I would absolutely not short Go Pro, not sure what you think the reason is that would make this a good idea?

2.7 times sales for a company with negative revenue growth. No thanks.

Edit: Don't take my 10 seconds of analysis on Yahoo Finance too seriously. Plus, I'm not too into shorting companies. I'd rather invest in good companies than short bad ones.

Give it a year.

Are you feeling squeezed today?

Was talking to some film/photography buddies today and they were saying that the $300 gopo shoots not only equal but better video than a $5k sony/cannon/nikon camera. The camera's videos are 4k hd quality with stabilization. Part of the problem is the incumbents don't want to sell something so cheap that competes with their multi thousand dollar product lines.

Also, I kinda view GoPro a product/media hybrid, similar to redbull (now wouldn't that be a great merger).

Whether or not the company has long term staying power is unknown; however, at this point I do not think its a fad but a legit company redefining a market segment.

I wouldn't underestimate GoPro. It's too simplistic to think of them as a camera company with no barriers to entry. What they are is a marketing company along the lines of Red Bull. You're right that both have low barriers to entry, but neither of them are going anywhere soon.

Also, GoPro's camera itself is nothing special, but they have an incredible line of mounts and accessories that makes all those videos possible. It's like the app store that makes iPhones valuable, and it's not something that can be easily replicated.

edit: just realized the red bull analogy has been drawn a few times already, sorry for the repeat.

Ignore it right now, let the pigs play. Valuation is high no doubt, but so are Tesla & Facebook. Had you shorted Tesla last month or even early June you might be kicking yourself now.

GoPro is a great product and is developing a strong brand in a niche market. Maybe wait until it is dirt cheap to buy...

GoPro is/is fast becoming a huge media brand, much like Red Bull (that company that started out only making a couple of products, still makes those same products yet now has its logo on everything from F1 cars to record breaking skydivers to aerobatic plane races).

Focusing on the camera business, video cameras obviously aren't a new or innovative thing. However, selling a camera for $300 that takes very high quality video, and that can be mounted and applied in so many different ways, etc is a novelty. Flip cameras were a fad that didn't produce great quality footage, and you had to hold them in your hand (the closest you could get to emulating a GoPro would be duct taping a Flip camera to a stick, car, skateboard). Funnily enough, GoPro CEO/Founder Nick Woodman taped an early GoPro model to a race car roll bar years ago which is when he realized the potential applications for his (at the time) wrist-mounted camera, and this ultimately catapulted the company to where it is now.

There's plenty of $200-$500 action cam competitors out there, but most were late to market or didn't have a brand that caught on, so many haven't even heard of them (e.g. Contour, Sony Action Cam, etc). On the other end of the spectrum, an EPIC Red or Phantom camera with super high resolution, speed, etc. footage costs $20,000-$150,000 per unit, so those are never going to compete against GoPro in the consumer market. Yet despite only costing a few hundred dollars, even Hollywood movie productions and big TV shows use GoPro cameras in bulk, either for dangerous stunts, tight spaces, or where 1080p fixed point footage will suffice (e.g. Top Gear, which has one of the largest TV production budgets out there). As a result, I think the camera market for them is huge and will support the media growth strategy as it ramps up.

On the media front, they already have tons of user-created videos with more added everyday that they already use for marketing. I believe they can (eventually) shift this content into a fully-fledged revenue stream through advertising (see: GoPro channels on Xbox Live and Virgin America as proof of concept).

Their IPO pitch in a nutshell was that they are currently a camera company that has media component, but that they are shifting to becoming a media company that happens to sell cameras. In this day-and-age, with how massive content-sharing has become, I think they can figure out how to make money on the media business. In the meantime, they have a nice, profitable consumer products business that'll help fund the media growth, much like that energy drink company Red Bull did when it was starting out.

These guys make a camera that has a lot of competition. And the camera is ugly to wear to boot. You might as well strap an eight track player to your hang glider. DRIFT and Panasonic both have superior products that don't look like they fell out of the ugly electronics tree and hit every branch on the way down.

Whoops, went on a rant above without reading other comments first so I didn't see that the Red Bull/media point had already been beaten to death. Oh well, good to see a lot of people share my viewpoint on them!

Side note: its incredibly amazing that the founder still has ~50% of the shares as of the date of the IPO. That is beyond impressive, not only for a startup in general but particularly for a hardware company.

would rather long it now.

The analogy should be more about companies like TomTom or Garmin, at some point everybody had a sat-nav in their car and sales plummited. The difference with Red Bull is that you drink it every day, you don't buy a new camera every day, month or year..

I don't know about you but I don't drink red bull everyday, not even every month. I have however already purchased two GoPro's since the first one was created 5 years ago, and my total spending on GoPro products in that time span has easily exceeded the amount of money I spent on Red Bull. Obviously I am not the norm, but neither are the suicidal addicts you have in mind that drink red bull everyday.

Down 6.5 premarket, maybe the beginning of the end?

My favorite GoPro video

http ://vimeo.com/83187924

I am short Gopro stock quote: GPRO, because currently the stock is getting a lot of hype due to it being an ipo a few days ago and many believe it is a revolutionary product. Sooner or later usually with tech companies they will start getting a lot of bad articles mainly in the finance section, mainly bad mouthing the product on how it might be overpriced, better technology is out there etc. There are still shares to short btw. My estimate of what might happen in the short term is it might level off right above in the 40's but its going to lose momentum and will be a wild one. My advice dont build a Big Short position just slowly average in and depending on the size of your account you will need cash on the sidelines. Thank you for reading.

Where are you getting shares?

Just want to add that kudos to Nick Woodman for creating such a successful product and company. The guy was born with a silver spoon in his mouth, with a father who was founding partner of Robertson Stephens and a stepfather who is general partner at U.S Venture Partners. He could have never worked single day in his life and partying away on his trust fund or bow into social pressure and get a "prestigious" finance job working and stressing away long hours for someone else.

Instead he forged his own path, discovered and tapped into a market niche and created a hugely successful company out of it. His family did help out with money and investor contacts and they are nicely rewarded for it. I believe his father is now worth at least $500m from his stakes at GoPro and he made a heck lot more more money from his son's little project than he did through his entire finance career.

Via Barrons - http://online.barrons.com/news/article_email/SB500014240531119036841045…

Largely disagree with this guy.

I am getting killed with all these shorts on GPRO. I am holding long-term.

Selling climax into a gap fill, bought hard and shorts got squeezed by the balls.

Vel aut voluptatem reprehenderit quam. Nam qui ipsa non amet. Fugiat accusamus mollitia reiciendis beatae veniam rerum sunt.

Iste quasi perferendis nostrum quis. Quasi qui reprehenderit soluta possimus alias. Nihil amet fuga eum ducimus. Rerum perspiciatis repudiandae totam ad dolores.

Repellat vel quas enim. Doloribus molestiae in sequi et eaque eum. Officia corrupti distinctio expedita voluptas temporibus quia temporibus. Odio perspiciatis voluptatem id fuga sed quisquam exercitationem doloremque. Fugit aut ut sapiente architecto consequuntur temporibus recusandae. Hic illo aspernatur quod facilis iure magnam tempora delectus.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Quia molestiae delectus et eius. Vitae velit delectus omnis minus aliquid porro. Dicta dolorem cupiditate amet voluptatem asperiores magni expedita reprehenderit. Voluptas aut maxime quia cupiditate. Totam optio omnis et est. Impedit magnam repellat quia quas nobis quo voluptate.

Provident veniam qui incidunt aut ea aliquam. Nesciunt laborum ea consequatur nulla et molestias aut. Vero excepturi officia natus molestiae quo quae vitae. Aperiam repellat occaecati omnis sed expedita quia.

Sint distinctio ad saepe. Qui optio veritatis tenetur repellat ad illum laboriosam. Quos qui necessitatibus magnam nam. Dolores aperiam est qui eveniet et mollitia. Sit non non aperiam aspernatur voluptates. In sequi ut suscipit delectus.

Laudantium hic deserunt nisi nesciunt labore aut et. Et laborum dignissimos quia expedita ex aut. Provident eos accusamus iure et atque debitis.

Tempora nam quam sed ipsum sint nostrum inventore. Et voluptatibus ut qui quis. Earum qui aperiam ipsum cupiditate dolore consequatur et. Est quasi ut impedit cumque autem at hic.

Fugiat harum unde quisquam neque dolorum sint et. Sed ipsam alias adipisci non. Accusamus delectus iste beatae atque.