Qualitative business analysis before valuation - looking for feedback on my structured framework (IB / M&A context)

Hey WSO,

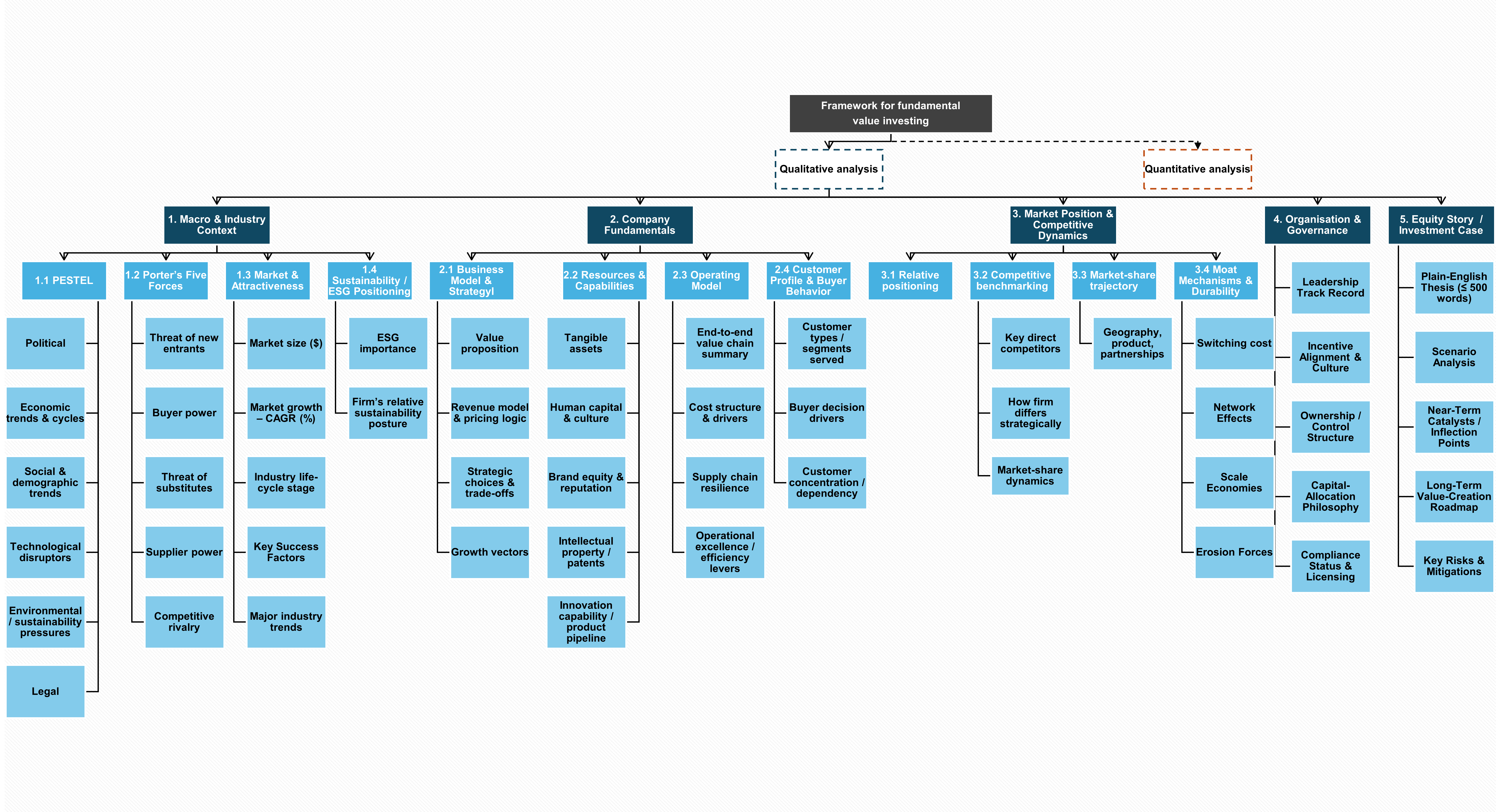

I’m refining a structured framework I use to break down businesses before I build any valuation model (DCF, comps, precedent transactions) or contribute to deal strategy.

I’m a big believer that any model is only as solid as the qualitative foundation behind it — and that understanding a company’s business model, market, and risks is what separates good work from great work.

Why I’m posting

👉 I’d appreciate feedback from the WSO community:

- How do you structure your qualitative business understanding before valuation or advising on deals?

- Are there angles I’m missing that are especially critical in M&A / IB contexts?

- What frameworks or tools have helped you bridge qualitative insights into valuation assumptions?

Recusandae perspiciatis unde veritatis quisquam optio nesciunt quae. Rerum et vero esse maxime inventore. Rerum labore sed totam cupiditate. Nihil quaerat quidem cum corporis accusamus sed. Sit ab error rerum a est porro debitis.

Et rerum temporibus quia velit. Nemo pariatur dolorem tenetur et. Soluta et repellat porro. Expedita officiis aliquam at mollitia repellat reprehenderit.

Rerum eum maiores dignissimos laudantium autem. Ea omnis voluptatum sint maiores. Facere voluptas voluptatem voluptatibus et.

Dolor distinctio molestiae quod. Esse et incidunt alias sit possimus. Repellat maxime aliquam enim. Perspiciatis rerum a placeat perspiciatis sunt aliquid nihil expedita. Aut ut nam et et. Perspiciatis consequatur ut voluptas asperiores molestias dignissimos. Tempore voluptate provident illo et quia.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...