An Exhaustive Guide: How to Solve Every Single Accretion/Dilution Question

Made this guide (not AI) for people who might be studying technicals. hope people find it helpful and it was a good refresher for myself. If you want to read the full article - it is here with formulas

Overview

Whether you are interviewing for bulge brackets, elite boutiques, or middle market firms, M&A accretion/dilution numerical technicals are something you should be ready for. The difficulty will vary. A BB interview will not be as hard as a Centerview interview, but it is a good idea to familiarize yourself with the mechanics of M&A problems end to end so you have a complete understanding.

Yes, you can watch videos, read how a merger model works, read the entire 82 page Breaking Into Wall Street M&A guide, or even build a merger model from scratch. But frankly, none of that is needed to solve these problems. You can learn the mechanics in an afternoon. If you have completed a pre-calc class, or heck, even Algebra 2, you have the mathematical ability to solve them.

The first part is understanding what is going on in an M&A transaction. For our purposes, we will treat mergers and acquisitions as the same thing. In reality there are subtle differences, but for interview math we can treat them as the same.

Fundamentally, you have a buyer and a seller. The buyer needs to pay the seller's shareholders some amount of money, and it can do that with 1) cash off its balance sheet, 2) new debt, 3) new stock, or some combination of the three. Each source has a different cost. Generally, cash is cheaper than debt which is cheaper than equity. Why? Cash has a cost because the buyer loses the interest income it would have earned on that cash. Debt has a cost because the buyer now pays interest. Equity has a cost because the buyer issues new shares.

Okay, so we know that each of the three possible financing sources, from the buyer's perspective, has a cost. But the main question is whether the additional benefits from the seller's net income and synergies, meaning things we are going to obtain when buying the seller, outweigh this cost. This is why we use earnings per share, or EPS. We look at the buyer's standalone EPS before the deal, and then the buyer's EPS after the deal, known as pro forma EPS. If pro forma EPS is greater than standalone EPS, the deal is accretive. If pro forma EPS is less than standalone EPS, the deal is dilutive. If the two are equal, the deal is breakeven.

That is the entire idea, and below we will explain a framework for how you can determine what is happening to EPS before and after the deal. One formula captures everything:

where Tax Rate = TR

Or abbreviated:

That looks intimidating, but by the end of this guide, you will understand the formula in full. You should write it down, since it encompasses every nuance you could get in an accretion/dilution problem. The numerator is pro forma net income. Start with the buyer's net income, add the seller's net income, subtract the after-tax cost of cash and debt financing, and add after-tax synergies if given. The denominator is pro forma shares. Start with the buyer's shares outstanding and add new shares only if the buyer uses stock. Then compare the new EPS to the old EPS.

Every accretion/dilution question is asking you to build that formula in one way or another.

Step 1: Find the Buyer's Standalone EPS

This is your baseline, and you will compare against it at the very end, so calculate it first and set it aside.

Buyer EPS = Buyer Net Income / Buyer Shares Outstanding

For example, if the buyer has $100 million of net income and 50 million shares, EPS = 100 / 50 = $2. That means each buyer share currently "owns" $2 of annual net income. After the deal, you are testing whether each share owns more than $2 or less than $2.

Sometimes the interviewer gives you EPS directly, which saves you a step. Sometimes you also might have to back into it.

Buyer EPS = Buyer Share Price / Buyer P/E

Most students see this formula for calculating EPS and memorize it. But understanding the relationship between P/E and EPS is very helpful since you might not always be given the same two pieces of information.

P/E = Share Price / EPS

So if the buyer trades at $40 per share and has a 20x P/E, EPS = 40 / 20 = $2.

The reverse:

Earnings Yield = EPS / Share Price

Since P/E = Share Price / EPS, earnings yield is just the inverse of P/E:

Earnings Yield = 1 / P/E

So a 20x P/E means a 5% earnings yield, because 1 / 20 = 5%. That just means for every $1 of market value, the company generates $0.05 of net income. This matters because accretion/dilution is really a comparison of yields. What earnings yield are you buying from the seller, and what is the cost of the currency you are using to buy it? We will get more into earnings yield in Extra Stuff - Part 1.

So we get to standalone EPS. That is all Step 1 is.

Step 2: Figure Out the Purchase Price and the Financing Mix

The purchase price could be given a few ways. It might be stated directly: "The buyer acquires the seller for $200 million." It might come as an offer price per share:

Purchase Price = Seller Shares Outstanding × Offer Price per Share

It might come as a premium to where the seller trades:

Purchase Price = Seller Market Cap × (1 + Premium %)

Or it might come as a multiple:

Purchase Price = Seller Net Income × Acquisition P/E

Remember, buyers often pay a premium due to potential synergies, control, and strategic value. The way you deal with this is by multiplying the market cap by 1 + the premium. If the seller is worth $150 million today and the buyer pays a 30% premium, the purchase price is 150 × 1.30 = $195 million.

This is also where you need to be careful about whether the interviewer is giving you equity value or enterprise value.

For most simple interview questions, "purchase price" means the equity purchase price, or the amount paid to the seller's shareholders. This is the number you use to figure out how much cash, debt, or stock the buyer needs to issue as consideration.

Equity Value = Value of the Seller's Common Equity

Enterprise Value = Equity Value + Net Debt + Preferred Stock + Minority Interest - Investments

If equity value or enterprise value is confusing to you, it is recommended to learn those before doing M&A problems. Anyways, for accretion/dilution math, the rule is:

If the question gives you equity value or offer price per share, use that as the purchase price paid to shareholders. If the question gives you enterprise value, check whether you need to convert it into equity value.

So if the buyer acquires a seller at a $500 million enterprise value and the seller has $100 million of debt and $20 million of cash, net debt is $80 million. The equity purchase price is 500 - 80 = $420 million. That $420 million is the amount paid to the seller's equity holders.

Remember, new shares issued should be based on the equity purchase price, not the enterprise value. If the buyer is paying the seller's shareholders with stock, it issues stock for the equity part. You don't issue stock to "pay" the seller's existing net debt unless the question specifically says the buyer is also refinancing or paying off that debt with new financing. That said, in many interview questions, they simplify this and say something like "the buyer acquires the seller for $200 million" without mentioning debt or cash. In that case, treat the $200 million as the purchase price and do not overcomplicate it. Only adjust for net debt if they give you enterprise value, seller debt, seller cash, or explicitly say the buyer assumes or refinances debt. A small nuance here, but we've seen this come up in harder interview questions.

That is the hard part of Step 2. The easy part is noting how the deal is financed. Every dollar of the purchase price comes from one of three buckets: cash, debt, or stock. It might be 100% of one, or a mix like 50% debt / 50% stock, 25% cash / 25% debt / 50% stock, or some other split. Each method costs a different amount, which is what Steps 3 and 4 are about.

Step 3: Calculate Pro Forma Net Income

Start with the two companies' earnings combined, then subtract what the financing costs and add synergies if you're given them:

Pro Forma Net Income = Buyer Net Income + Seller Net Income - After-Tax Financing Costs + After-Tax Synergies

The easiest way to think about the numerator is that after the deal, the buyer now owns the seller, so the buyer gets the seller's net income. But the buyer also had to pay for the seller. The cost of that payment reduces the benefit. You are trying to see whether the seller's earnings are large enough to overcome the cost of the financing.

Cash: the buyer's cash was sitting on the balance sheet earning interest, and now it's gone. That foregone interest income comes out of net income. This is one of the most commonly missed pieces in interviews, because people assume cash is free. It isn't.

After-Tax Foregone Interest = Cash Used × Interest Rate on Cash × (1 - Tax Rate)

For example, if the buyer uses $100 million of cash and that cash was earning 4%, the buyer loses $4 million of pre-tax interest income. If the tax rate is 25%, the after-tax hit to net income is 4 × (1 - 25%) = $3 million.

Debt: new debt means new interest expense.

After-Tax Interest Expense = Debt Raised × Interest Rate on Debt × (1 - Tax Rate)

For example, if the buyer raises $100 million of debt at an 8% interest rate, pre-tax interest expense is $8 million. If the tax rate is 25%, the after-tax hit to net income is 8 × (1 - 25%) = $6 million.

Stock: the cost of stock shows up in the share count in Step 4. That is why stock financing feels "free" in the numerator but not in the full EPS calculation. It does not reduce net income, but it spreads that net income across more shares, and creates dilution.

It is imperative that you understand that interest expense is tax-deductible and interest income is taxable, so both flow through the tax line before they reach net income. That's why every financing cost gets multiplied by (1 - Tax Rate).

Synergies work the same way. Cost savings usually hit operating income, which is pre-tax, so:

After-Tax Synergies = Pre-Tax Synergies × (1 - Tax Rate)

If they say the synergies are already after-tax, add them straight.

A little more on synergies: synergies are the extra earnings the buyer expects from combining the two businesses. In interview math, these are usually hard cost synergies, meaning actual cost savings that are easier to quantify. Examples include removing duplicate corporate overhead, consolidating offices, cutting redundant public company costs, combining vendors, reducing duplicated management teams, or improving purchasing power. These are called "hard" because they are more concrete than vague revenue synergies.

Revenue synergies are things such as "the buyer can sell the seller's product to its customers" or "the combined company can cross-sell better." In real life, bankers may discuss these, but in technical interview math, cost synergies are much cleaner because they drop into operating income. If the interviewer says there are $10 million of pre-tax cost synergies, you tax-adjust them and add them to pro forma net income:

After-Tax Synergies = 10 × (1 - 25%) = $7.5 million

Synergies help accretion because they only touch the numerator. If a deal is slightly dilutive before synergies, hard cost synergies may be enough to make it neutral or accretive.

Step 4: Calculate Pro Forma Shares and Compare

If the deal is funded with cash or debt only, no new shares get issued and the share count does not move:

Pro Forma Shares = Buyer Shares Outstanding

If any portion is stock, the buyer issues new shares to cover it:

New Shares Issued = Stock Portion of Purchase Price / Buyer Share Price

Note that it's the buyer's current share price in the denominator, not the seller's. The buyer is paying with its own shares, so its own price determines how many it has to print. This is also why a richly valued buyer likes stock deals: a higher share price means fewer new shares per dollar of purchase price.

If the buyer's share price is $40 and it needs to fund $200 million with stock, it issues:

New Shares = 200 / 40 = 5 million

If the buyer's share price were $80 instead, it would only issue:

New Shares = 200 / 80 = 2.5 million

Same purchase price, but fewer shares because the buyer's stock is worth more. That is why a high-P/E buyer can make an all-stock deal accretive.

Then:

Pro Forma Shares = Buyer Shares Outstanding + New Shares Issued

And finish it:

Pro Forma EPS = Pro Forma Net Income / Pro Forma Shares

Accretion / (Dilution) % = (Pro Forma EPS / Buyer Standalone EPS) - 1

Positive means accretive. Negative means dilutive. Zero means neutral. That is it. Everything above covers you from a basic prompt to the hardest version of this question you'll see.

Three Examples: One Per Financing Method

We will use the same numbers for each example, so you can see the differences. Assume Company A buys Company B. Company A has $100 million of net income, 50 million shares outstanding, and a $40 share price, so EPS = $2 and P/E = 40 / 2 = 20x. Company B has $20 million of net income and is acquired for $200 million, which implies a 10x acquisition P/E. The tax rate is 25%.

All cash: Assume a 5% interest rate on cash. Foregone interest = 200 × 0.05 × (1 - 0.25) = $7.5 million after tax. Pro forma net income = 100 + 20 - 7.5 = $112.5 million. No new shares are issued, so pro forma EPS = 112.5 / 50 = $2.25. Versus standalone EPS of $2, that is 2.25 / 2 - 1 = 12.5% accretive.

The deal is accretive because pro forma EPS increases from $2 to $2.25. Even after losing the interest income on the cash used to fund the deal, Company A still adds enough net income from Company B to increase EPS.

All debt: Assume an 8% interest rate on debt. After-tax interest = 200 × 0.08 × (1 - 0.25) = $12 million. Pro forma net income = 100 + 20 - 12 = $108 million. Still no new shares are issued, so pro forma EPS = 108 / 50 = $2.16. Versus standalone EPS of $2, that is 2.16 / 2 - 1 = 8% accretive.

The deal is accretive because pro forma EPS increases from $2 to $2.16. The interest expense from the new debt reduces the benefit from Company B's net income, but not enough to make EPS fall below the standalone level.

All stock: New shares = 200 / 40 = 5 million, so pro forma shares = 50 + 5 = 55 million. No financing cost hits net income, so pro forma net income = 100 + 20 = $120 million. Pro forma EPS = 120 / 55 = $2.18. Versus standalone EPS of $2, that is 2.18 / 2 - 1 = about 9.1% accretive.

The deal is accretive because pro forma EPS increases from $2 to $2.18. There is no interest expense or foregone interest income, but the buyer has to issue new shares, which increases the denominator.

Mixed, 50% debt / 50% stock: After-tax interest on the debt half = 100 × 0.08 × (1 - 0.25) = $6 million. New shares from the stock half = 100 / 40 = 2.5 million. Pro forma net income = 100 + 20 - 6 = $114 million. Pro forma shares = 50 + 2.5 = 52.5 million. Pro forma EPS = 114 / 52.5 = $2.17. Versus standalone EPS of $2, that is roughly 2.17 / 2 - 1 = 8.6% accretive.

The deal is accretive because pro forma EPS increases from $2 to $2.17. The debt portion reduces pro forma net income through interest expense, while the stock portion increases the share count. Even after both effects, EPS is still higher than before the deal.

If you use all three, your method does not change. For example, if the same $200 million purchase price were funded with 25% cash, 25% debt, and 50% stock, the buyer would use $50 million of cash, raise $50 million of debt, and issue $100 million of stock. You would calculate:

After-Tax Cash Cost = 50 × Cash Interest Rate × (1 - Tax Rate)

After-Tax Debt Cost = 50 × Debt Interest Rate × (1 - Tax Rate)

New Shares Issued = 100 / Buyer Share Price

Then plug those into the same pro forma EPS formula. This is where the big pro forma EPS formula we showed you at the beginning of this post comes in handy.

Extra Stuff - Part 1: A Shortcut When There Are No Synergies or Premium

Whenever you don't have synergies or a premium paid on the deal, you can use the below shortcut, which is often far faster than doing the full pro forma EPS calculation, and is how bankers do back-of-the-envelope calculations on the desk. As we've discussed:

Seller Earnings Yield = Seller Net Income / Purchase Price

This is the same thing as:

Seller Earnings Yield = 1 / Acquisition P/E

So, if the seller has $20 million of net income and the buyer pays $200 million, the seller's earnings yield is:

20 / 200 = 10%

That also means the buyer is paying 10x earnings, because:

Acquisition P/E = Purchase Price / Seller Net Income = 200 / 20 = 10x

And:

1 / 10x = 10%

This is why P/E, earnings yield, EPS, and purchase price all relate. P/E tells you how many dollars you are paying for each dollar of earnings. Earnings yield tells you how many dollars of earnings you get for each dollar you pay. They are just inverses of each other. Recall:

Cost of Cash = Interest Rate on Cash × (1 - Tax Rate)

Cost of Debt = Interest Rate on Debt × (1 - Tax Rate)

Cost of Stock = 1 / Buyer's P/E

If the seller's earnings yield is higher than the cost of the financing, the deal is accretive. If it is lower, the deal is dilutive. If they are equal, the deal is neutral. For a mixed deal, weight the costs by the financing percentages.

In our examples, the seller's yield is 20 / 200 = 10%, against a 3.75% cost of cash, a 6% cost of debt, and a 5% cost of stock, since 1 / 20x = 5%. The yield beats all three, which is why every version came out accretive, and the ordering of the costs even tells you cash accretes most and debt least.

For mixed financing, you can do the same thing with a weighted average cost. Suppose a deal is funded 50% debt and 50% stock. If the after-tax cost of debt is 6% and the cost of stock is 5%, the weighted cost is:

Weighted Financing Cost = 50% × 6% + 50% × 5% = 5.5%

If the seller's earnings yield is 10%, the deal should be accretive. If the seller's earnings yield were 4%, it would probably be dilutive. If it were 5.5%, it would be roughly neutral before synergies and other adjustments.

The all-stock version has the cleanest phrasing, and it comes up constantly: if the buyer's P/E is higher than the P/E it pays for the seller, the deal is accretive, and vice versa. The reason is that a high P/E means expensive shares, so the buyer issues fewer of them to bring in each dollar of the seller's earnings. Cheap earnings bought with an expensive currency raises EPS. Many finance textbooks will start, rather than end, with this rule, but we think that you should not "memorize" this rule, but rather understand it, since it makes the mixed-financing problems much easier. Check right now: can you explain to an 8th grader why, with only a buyer and seller's P/E, we can tell if an all-stock deal is accretive or dilutive?

Again, with synergies, premium paid, or other adjustments, this method does not work, so be careful when using it. But in simple problems, it is a great way to get to an answer fast.

Extra Stuff - Part 2: Edge Cases / Twists Asked

Every single "harder" version of the above does not add any new concepts. It asks you to solve for something that is not pro forma EPS. Just like what you learned in the latter half of your Algebra 2 class. This is common in Centerview, Evercore, and Moelis interviews.

Question-type 1: "What premium makes the deal breakeven?" means set pro forma EPS equal to standalone EPS and back into the purchase price. In other words, find the maximum price the buyer can pay before the seller's earnings yield no longer beats the cost of financing.

Question-type 2: "How much in synergies is needed for the deal to be neutral?" means find the EPS difference, convert it to the missing net income, and account for your tax rate.

In other words:

Required Pro Forma Net Income = Buyer Standalone EPS × Pro Forma Shares

After-Tax Shortfall = Required Pro Forma Net Income - Pro Forma Net Income Before Synergies

Pre-Tax Synergies Needed = After-Tax Shortfall / (1 - Tax Rate)

If you need $5 million more of after-tax net income to make EPS neutral, and the tax rate is 25%, the required pre-tax synergies are:

5 / (1 - 25%) = $6.7 million

That is because only 75% of pre-tax synergies reaches net income after taxes. So you need more pre-tax synergies than the after-tax shortfall.

Question-type 3: if they give you the seller's EPS and share count instead of net income, multiply:

Seller Net Income = Seller EPS × Seller Shares Outstanding

Question-type 4: if they ask you to solve for the tax rate required for the deal to be breakeven, set pro forma EPS equal to the buyer's standalone EPS and solve for the tax rate.

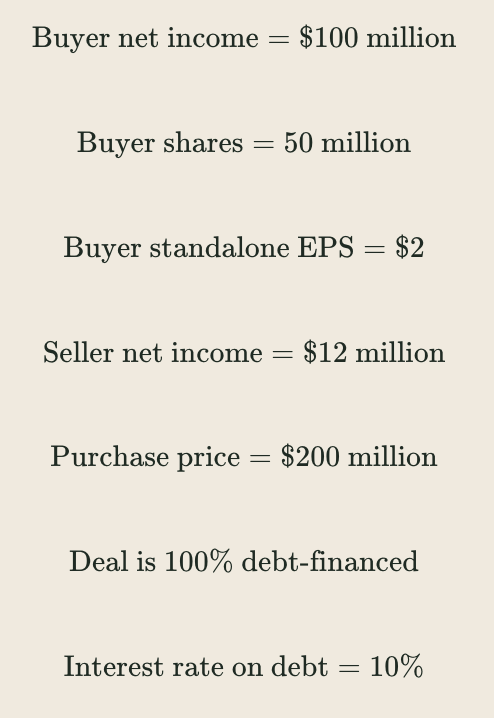

Let's say that:

Because the deal is 100% debt-financed, no new shares are issued, so pro forma shares stay at 50 million.

For the deal to be breakeven, pro forma EPS must stay at $2, which means pro forma net income must stay at:

$2 × 50 = $100 million

Interest expense = $200 million × 10% = $20 million

Now solve for the tax rate:

Pro Forma Net Income = 100 + 12 - 20 × (1 - Tax Rate)

Set it equal to $100 million:

100 + 12 - 20 × (1 - Tax Rate) = 100

12 = 20 × (1 - Tax Rate)

60% = 1 - Tax Rate

Tax Rate = 40%

So the deal breaks even at a 40% tax rate. Above 40%, the deal is accretive because the tax shield makes the after-tax interest expense lower. Below 40%, the deal is dilutive.

Question-type 5, which is very rare and the hardest version of this problem we have ever seen: if they give you enterprise value, do not use it for new shares. Ask what the buyer is paying to shareholders and whether the seller's debt is being refinanced. In a simplified question, they may intend enterprise value to be the total transaction value, but technically, stock issued to the seller's shareholders should be based on equity purchase price. The right thing to say then is: "If this is enterprise value, I would subtract seller net debt to get equity value for the consideration paid to shareholders. If the buyer is also refinancing the seller's debt, I would include the new debt financing cost separately."

If you understand the above, YOU CAN HANDLE EVERY SINGLE M&A TECHNICAL YOU WILL RECEIVE IN ANY INVESTMENT BANKING OR PRIVATE EQUITY INTERVIEW. Once you get the basics down, start practicing questions.

bump everyone should read this

Et quis nobis asperiores sint fugiat eos dolores. Suscipit distinctio quibusdam aut voluptatem corporis. Veniam voluptate quo qui repudiandae debitis eum velit. Illum aliquam est suscipit.

Nobis quis dicta est optio. Voluptas harum tempore sunt. Et iure eveniet distinctio quis voluptatem dolores recusandae. Pariatur voluptates voluptatem optio officiis aut voluptatem suscipit at. Quia aut sint itaque.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...