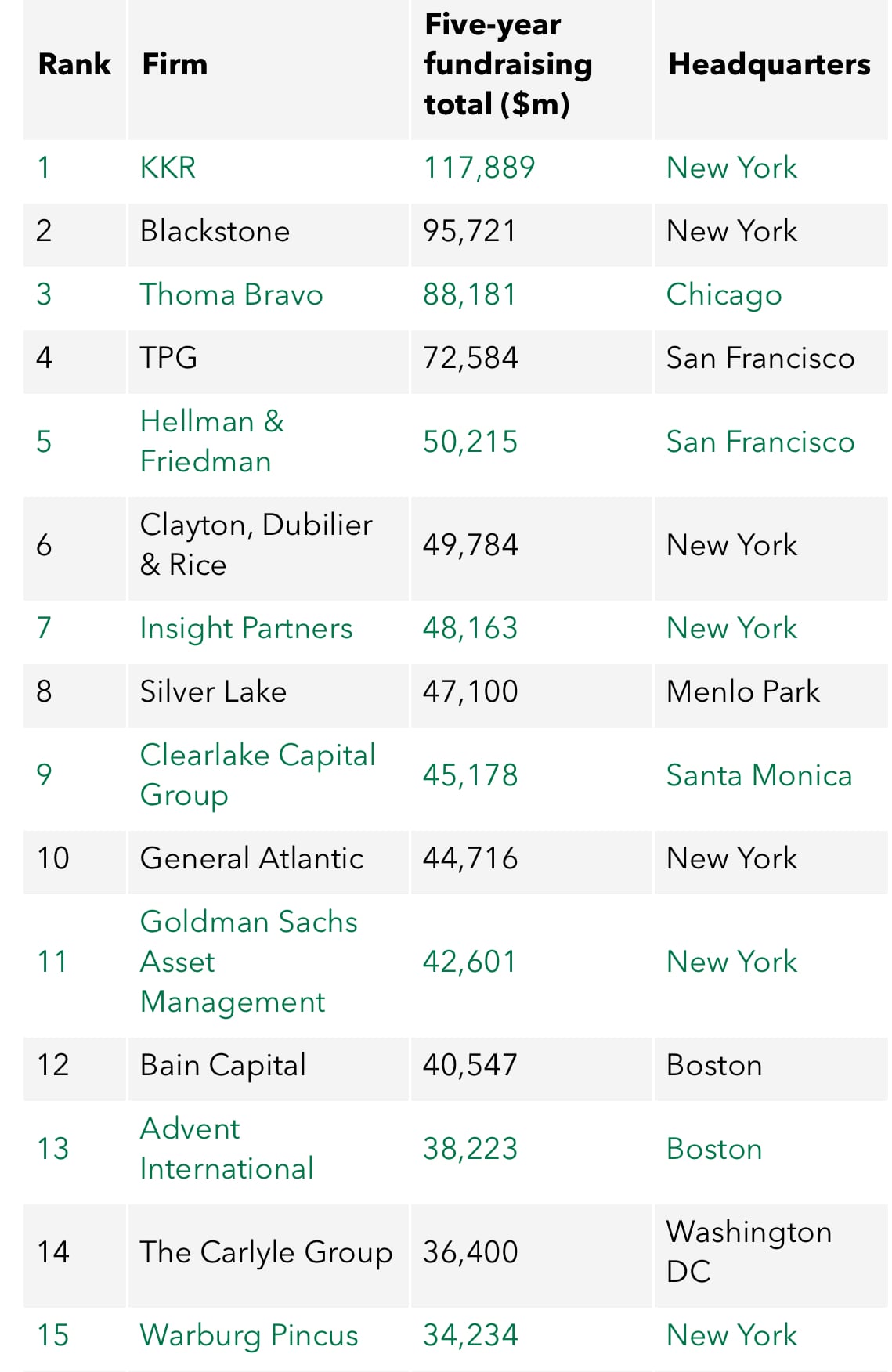

2025 Buyouts 100 List: Top 15 PE Firms

A few aspects of the list which were surprising:

- Not surprised to see top legacy MFs (BX / KKR / TPG) and big tech names (TB / SL), but did not expect to see Insight, GSAM, or Clearlake

- This forum loves to make fun of Clearlake, yet they have a better 5 year fundraising track record than half the megafunds?

- Carlyle has fallen off hard compared to their competitors of earlier decades (KKR / Blackstone 3x, TPG 2x their fundraising)

Feel like there’s a sentiment that Advent > Bain, but Bain has raised more in the last 5 years? Guess you can argue the returns aspect gives a slight edge to Advent

Advent is PE only, Bain has more stragies

The list is PE fundraising only, it already separates their credit, RE, other strategies. Advent raises one fund at a time, but Bain has multiple funds to do buyouts from. Not sure how this affects carry or headcount for each firm, but nonetheless surprised at how Bain is seen as a diminishing brand similar to Carlyle, yet are still outperforming their biggest competitor w/ same HQ

Which of these firms gives you the best mix of future fundraising and chances of promotion?

The firms that are 100+ that will be 50 in 2030

TPG and TB probably, KRR promotion is hard AF these days

Is this true?

What is TPG or TB chance of promotion?

For clarification I think it’s important to point out that its North America based firms.

Don’t think the list would change meaningfully but if it was global would assume some of the larger european MF/UMM (e.g., CVC, EQT, Hg) would make the cut and they do have pretty sizable US presence

Surprised Vista wasn’t top 15 either

Vista dropping to #20 per 2025 PEI 300 (fundraising 1/20-12/24)

No Apollo or Vista listed. Can see Apollo really more of a credit and insurance firm than a PE firm nowadays, but what’s causing Vista’s struggles?

Looking at the list, it’s tough to argue against the top five as the best places to start a career. If you’re optimizing for brand, long-term optionality, or exits, the most established firms like Blackstone/ KKR / TPG probably stand out the most. Maybe more of an emphasis on TB if you know you want tech investing

The rising UMM vs MF question gets more interesting when you look at some of the #10 to 20 firms on the list that have hit fundraising challenges. Would you rather be at a platform like Carlyle or Vista, which still have brand names and write large checks, but may be past their peak? Or take a chance on a smaller but faster-growing fund in the $5 to $8 billion range? There’s probably still more upside in being at the bigger name from a flexibility standpoint, but it’s not as clear-cut as it used to be, especially if the MF you choose ends up showing you the door at the end of the associate years

One last thought: the early joiners at Clearlake probably made out incredibly well. Even if future fund performance slips, they’re doing just fine off management fees alone. But for someone joining Clearlake today as a new associate, that story could look pretty different and might be worth avoiding if you have options at any other top-25 firm

How is that the conclusion you’ve arrived at? I’ve had a similar conversation with a MF PE partner who’s a close family friend about my future, and his view was the exact opposite. He told me that the legacy MFs aren’t the best long-term bets anymore, and the smart juniors are those targeting UMM/MM funds with real trajectory.

His view (and I agree with this) is that while the top MFs have great brand value, the percentage of people getting promoted post-associate is extremely low, and it’s not improving, even with fund sizes growing. The economics just aren’t in your favor. At most legacy MFs, the carry pool is getting split across a huge bench and public shareholders, while many UMM or fast-growing MM-to-UMM funds still offer real economics and faster promotion velocity for people who hit the ground running.

Additionally, he says lateral options aren't as open as people think. A lot of the top-performing UMM funds are heavily promoting from within. Even if you land a lateral role down-market after MF associate, you're competing with internal talent that already knows the firm’s culture, deal process, and strategy, and has internal political capital. That’s a hard gap to close from the outside.

With perfect information, if you knew you were joining a MM / UMM that was going to double or triple its fund size over successive raises, that would be the best plan.

In reality, no one knows which funds are going to be the ones to do so.

For every 1 person that joined a New Mountain or FP in the early days and are now seeing sizable carry allocations and clear promotion path, there were dozens who joined places like AmSec, AEA, Onex, Golden Gate, Siris, and Centerbridge. All of which have struggled immensely, had downraises, extended fund cycles, exodus of partners, etc. In fact, there was a time where all of the JAMMBOs just mentioned were all seen as a preferred seat over places like Clearlake or FP. It’s impossible to forecast what fundraising will look like a decade from now, and even most of those who may start at the next great fund won’t last long enough to see those benefits arise.

You take the MF offer if you’re lucky enough to get it, and sure the right tail outcome for someone who goes MM / UMM might be better. But the average MF aso will have more options to lateral, better exits, deal experience, and comp

While directionally helpful to see AUM raised as proxy into "health" of firm - this is the type of analysis that an IB A1 puts together and proceeds to get picked apart / discarded. This lacks importance nuance:

Needs proxy column to divide AUM raised by # of fundraises completed

Need to filter list (or insert column) for size of flagship buyout fund

Why does this feel like US News college ranking part 2 lol

Surprised at the number and length of comments discussing this when it's kinda dumb to use this ranking to draw many inferences. It's much less useful than the HEI performance rankings, which are also dumb given the 5-year timespan which, as some have noted, includes the pretty easy pre-2022 slowdown fundraising environment, overrates raises that started partly or wholly before industry-wide (and fund-specific) marks started taking nosedives, etc.

If you want to use Big and Dumb Fundraising Stats to rank-order PE firm, look at (a) latest flagship (and flagship only, unless for whatever reason it's a TPG HC situation where a separate fund really is part of the flagship conceptually if not literally or there was a strategy split in raises like with Charlesbank), (b) that fund's # of years after the last fund, (c) that fund's size comparison to the previous fund (or two), and (d) that fund's comparison to target, and maybe (e) how long that fund took to raise. These are all pretty brute-force, not sophisticated, ways to look at funds but will give you a better picture of what you're looking for than PEI's Big Bad Aggregator Stats rankings.

What about a fund like Permira? They do growth and buyout in one fund and do EU /US across one as well? Loved the TPG and CB examples!

Monster latest fund but whispers about the portfolio have been not great (I think?). I don't have a strong view but would diligence through contacts if possible

Assumenda suscipit a autem. Inventore eos quam repudiandae quia.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...