Why does my property project remain negative NPV even with high leverage and 20-year horizon? (WACC 14–15%) – looking for professional insight

In my financial model, I’ve estimated Free Cash Flows to Firm (FCFF) over 20 years and tested multiple capital structures and exit horizons, but all NPVs remain negative despite improving leverage.

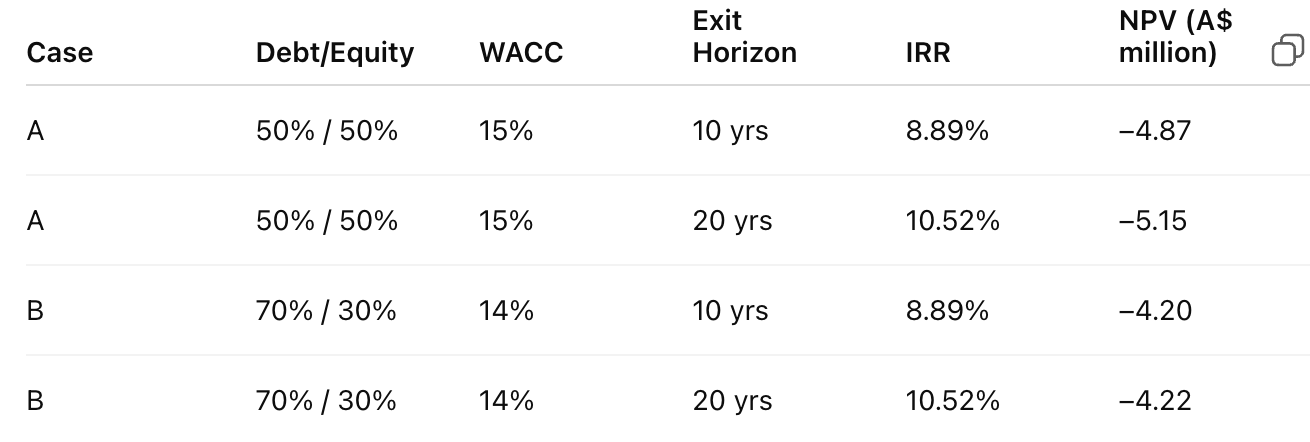

Here’s the summary of my findings:

Case

Assumptions:

- Initial investment: A$15 million

- Cost of debt: 8%, tax rate: 30%

- Rent growth: 5% p.a.

- Steady occupancy rate after Year 3

- Terminal value based on a 7% capitalization rate at exit

Despite adjusting the capital mix and extending the project life, the IRR never exceeds the WACC, and NPV stays negative.

What I’m trying to understand:

- Strategic justification:

In real-world settings, would property developers or infrastructure investors still proceed with a slightly negative NPV if the project delivers other forms of value (e.g., strategic land holding, brand, social impact, or long-term capital gains)? - Modelling practice:

Should I try to reflect this through real options (e.g., option to sell early, refinance, or redevelop later) instead of treating it as a fixed-term DCF? - Capital structure insight:

My analysis shows NPV improves slightly as leverage rises (due to a lower WACC), but even at 70–90% debt it doesn’t turn positive. In professional practice, how do analysts balance the tax-shield benefit with the rising financial distress risk when deciding the “optimal” debt level?

Based on the most helpful WSO content, here are some insights into your situation:

1. Strategic Justification for Proceeding with Negative NPV Projects

2. Incorporating Real Options into Your Model

3. Balancing Leverage and Financial Distress Risk

4. Why Your NPV Remains Negative

Recommendations:

By addressing these areas, you can refine your analysis and better understand whether the project is worth pursuing.

Sources: Trying to understand the concept of IRR, https://www.wallstreetoasis.com/forum/investment-banking/modeling-in-hf-vs-pe-vs-ib?customgpt=1, Real Estate Development Modeling, https://www.wallstreetoasis.com/forum/real-estate/using-100-equity-for-a-project-does-it-ever-make-sense?customgpt=1, PE professional, what's your process while judging an investment?

Starting rent?

Something isn't making sense. What is the discount rate you are using in the NPV formula.

You have too much negative leverage. Only an OZ deal would make it work.

Your IRR is less than your WACC, your NPV will always be negative.

A quick dummy model based on what you are describing, matching the IRR on the first scenario, I am getting an unlevered, after tax IRR of like 7.4%, while your after tax cost of debt is 5.6%, so you should be able to push it to some absurd leverage level to get a 15% equity IRR and positive NPV.

Et sed omnis consequatur occaecati neque. Dolores omnis ab velit asperiores blanditiis ut a. Voluptatem enim ut aperiam possimus molestiae et libero. Facere accusamus ut quidem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...