NEWBIE SEEKING FEEDBACK ON DCF MODEL

Hello all,

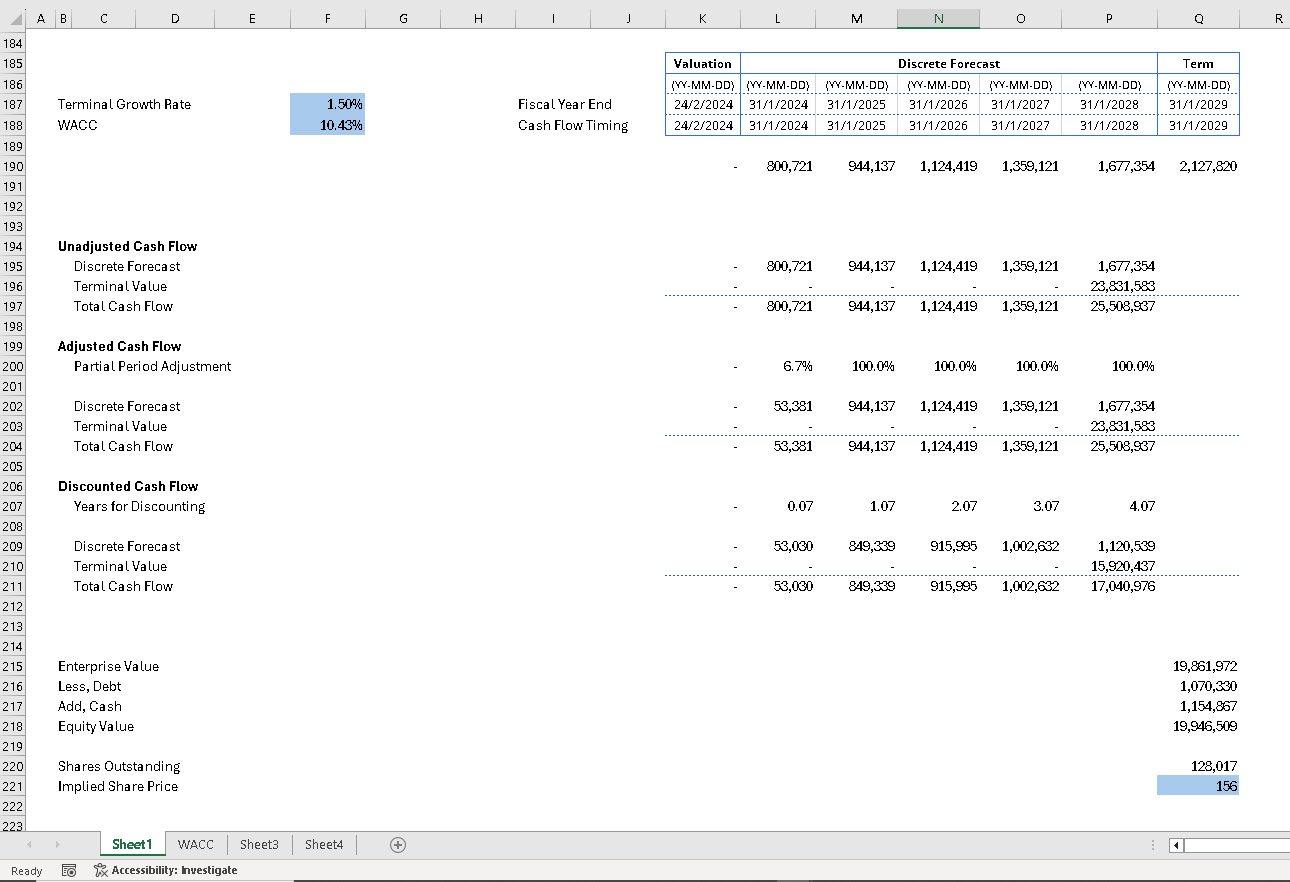

I just finished a DCF course and tried to make a DCF Model of lululemon from scratch. It seems like its most likely wrong as it has a -66% downside for the implied share price.

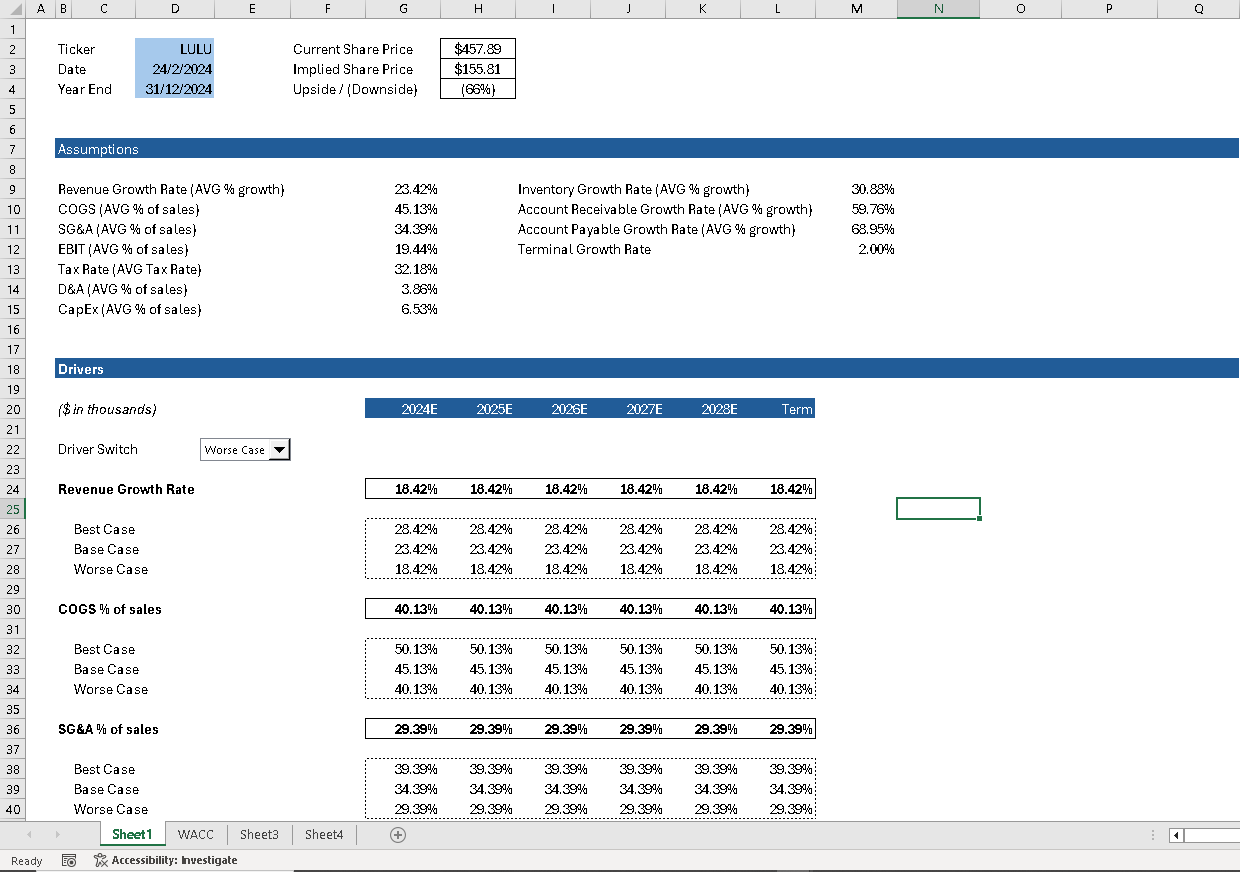

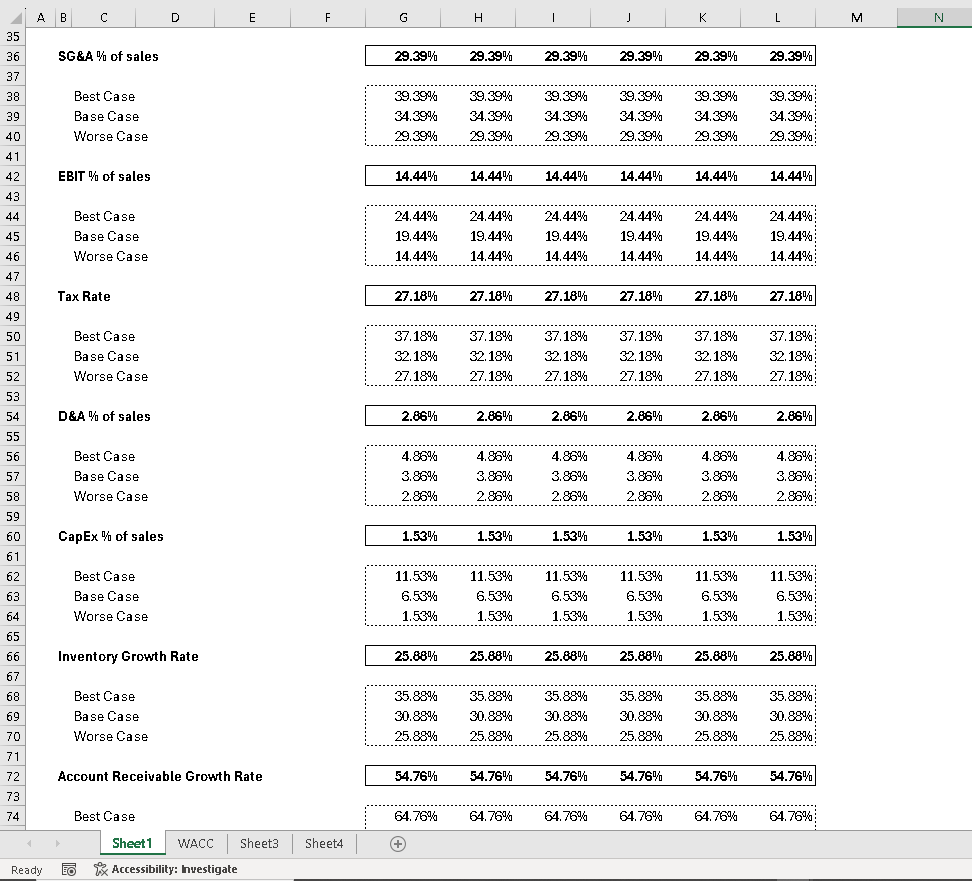

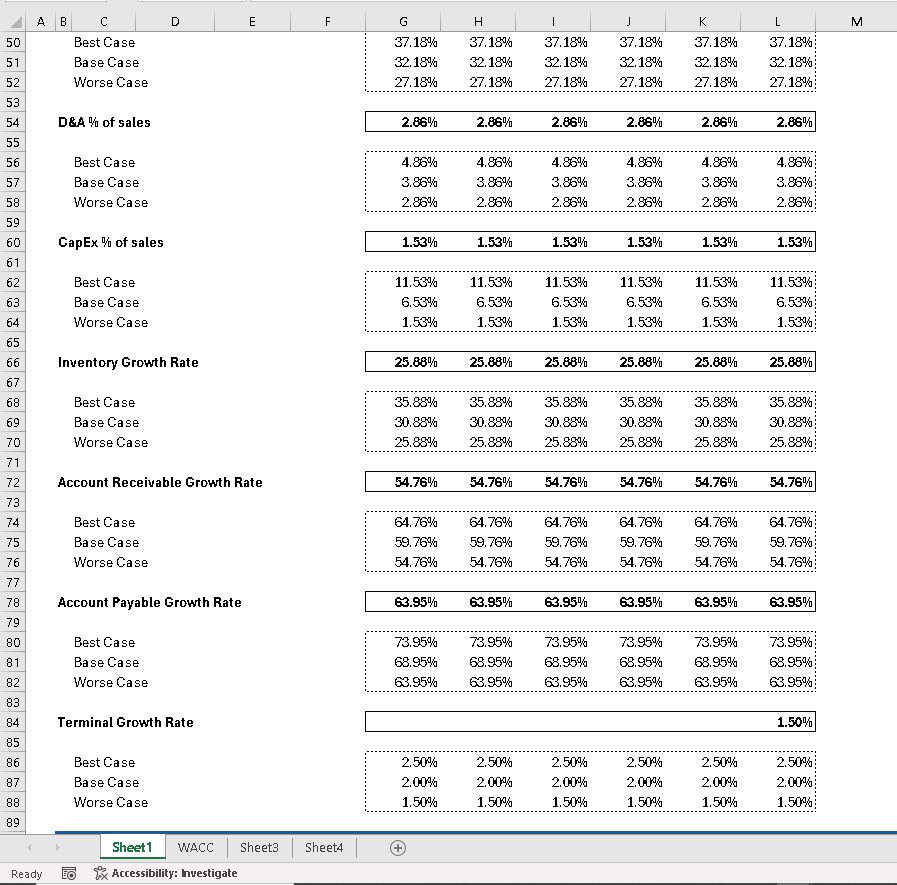

I'm unsure of how I should get assumptions so I just took the average of the past 7 year growth rates and added/subtracted 5% for Best and Worse case respectively.

Below I have attached the DCF model and I sincerely hope to receive feedback on how I can make it better. I have labeled the models in alphabetical order

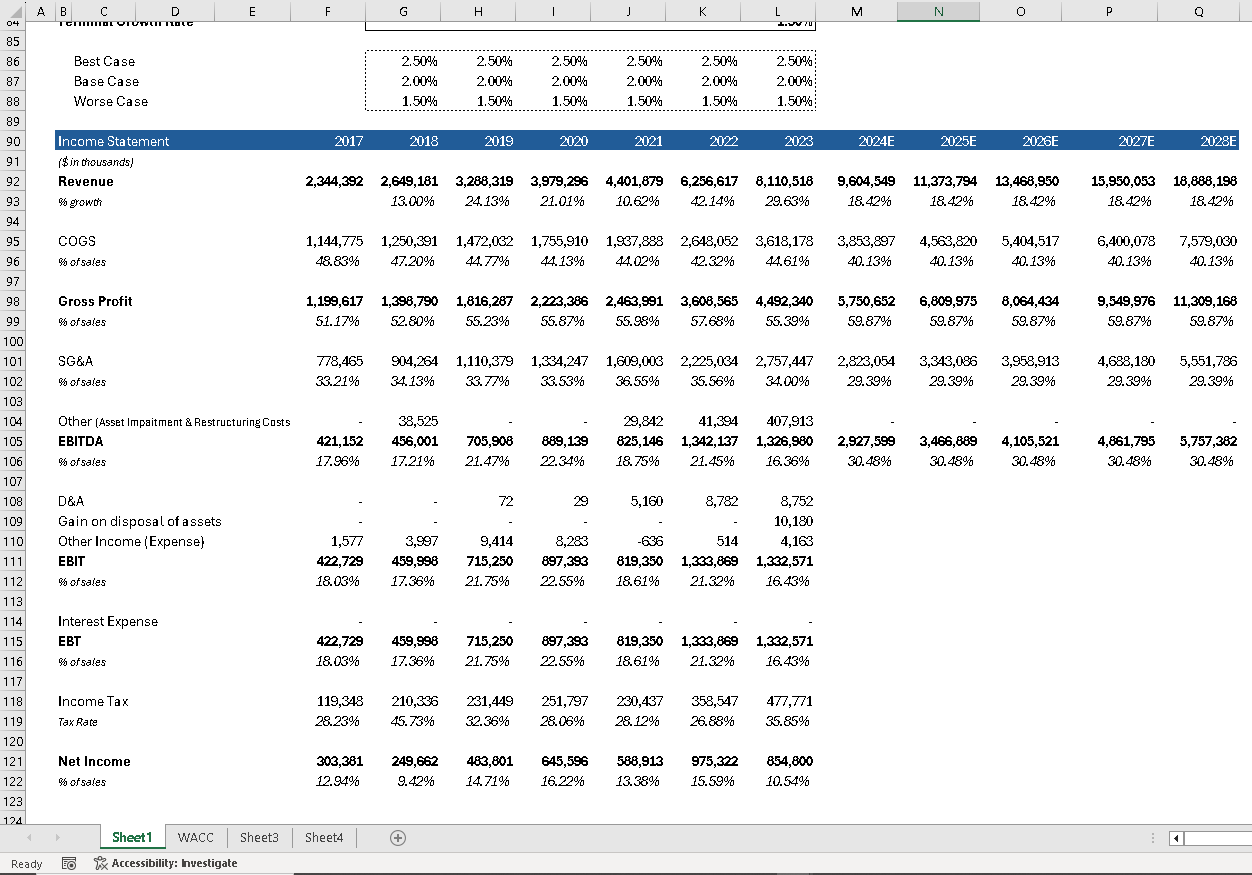

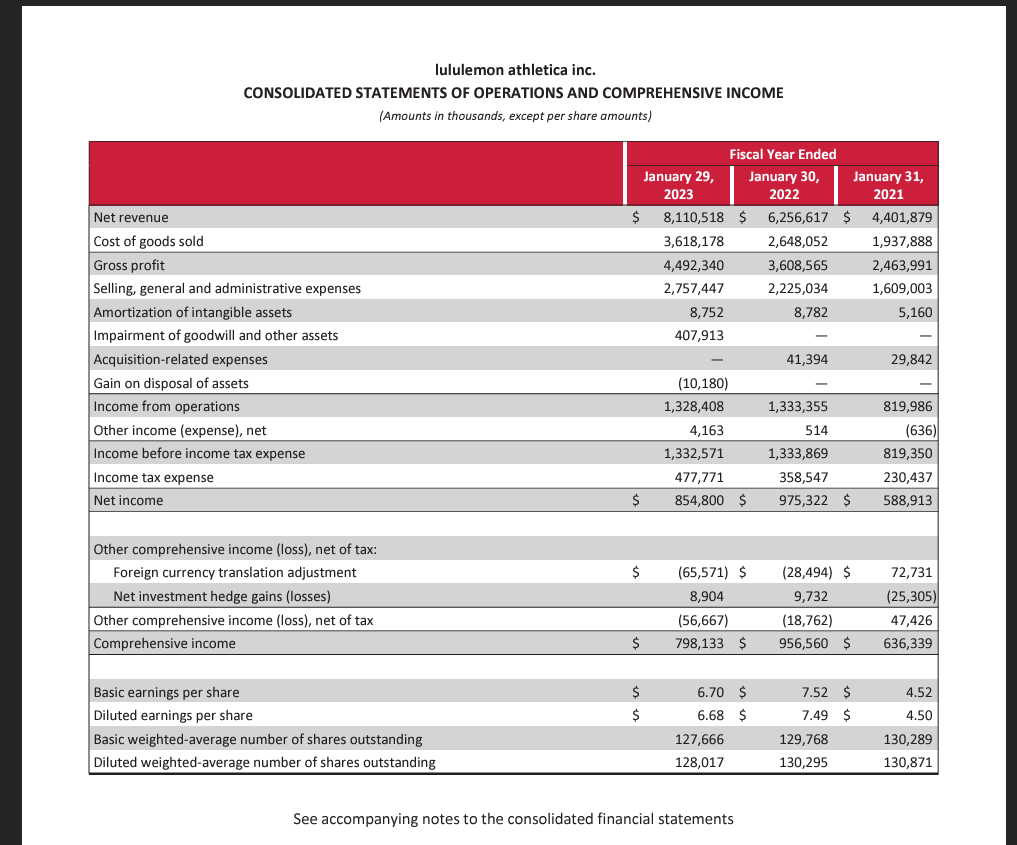

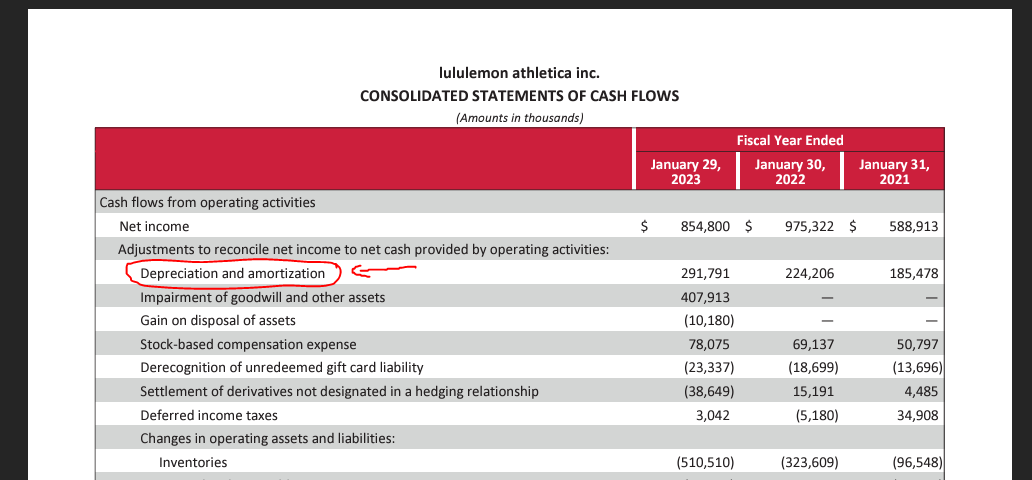

Also, please help me clear some doubts. When I look at the incomes statement for LULU (Screenshot I), there is not depreciation line item. But when I go down to the cashflow statement (Screenshot J, red arrow), there is a depreciation line item. Would like to seek clarity on this.

Thanks in advance for the help.

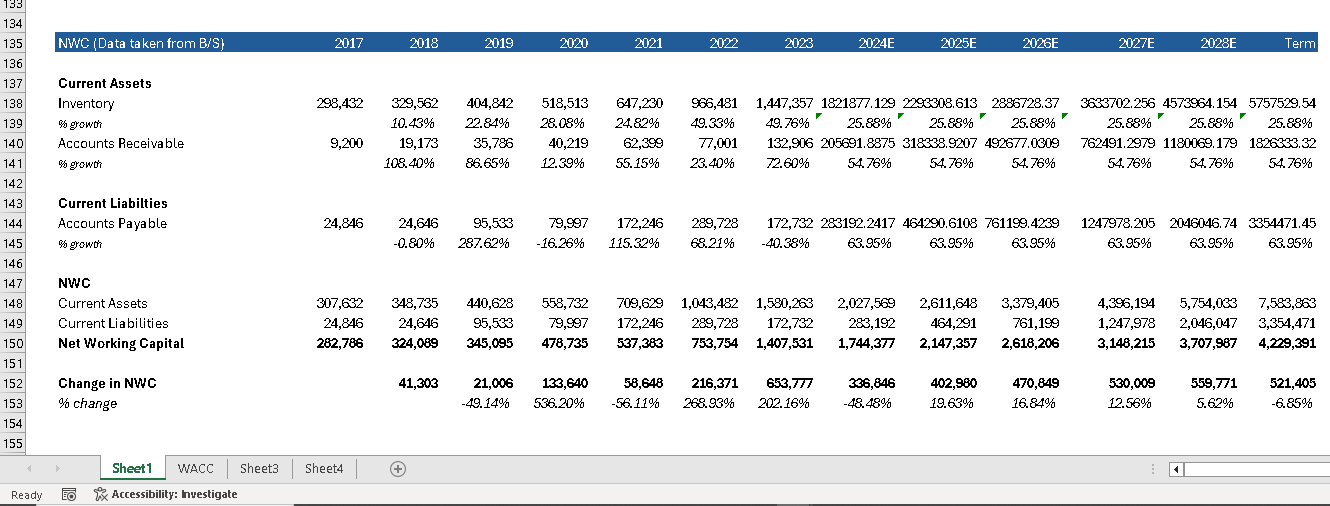

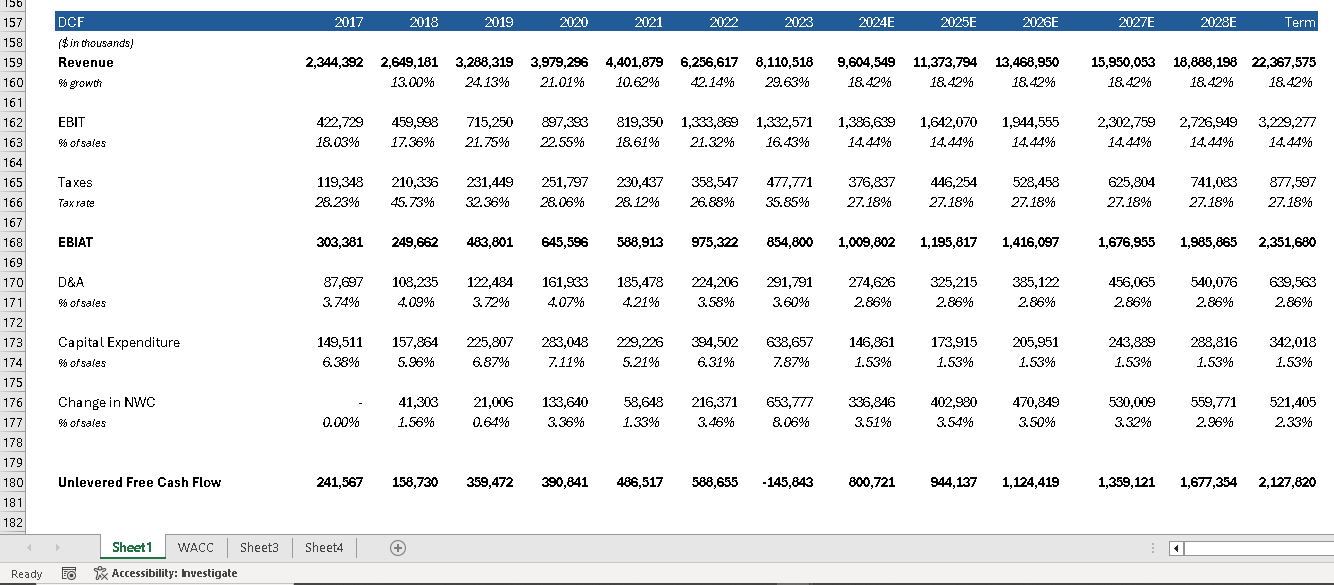

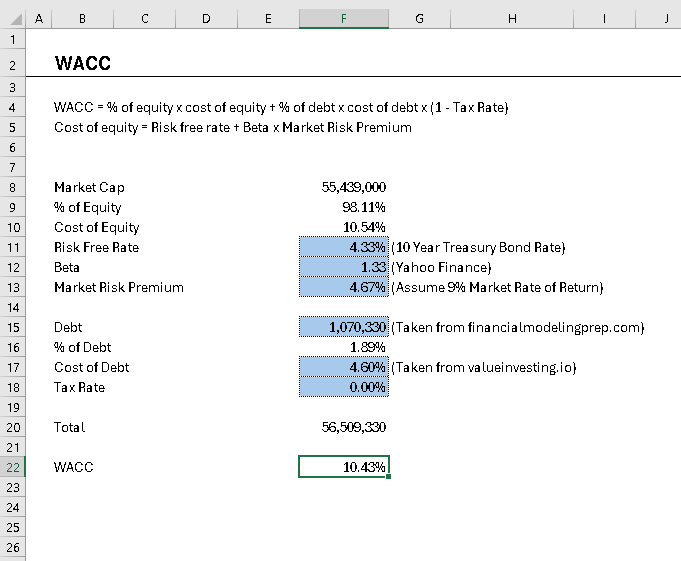

Screenshot A

Screenshot B

Screenshot C

Screenshot D

Screenshot E

Screenshot E

Screenshot F

Screenshot G

Screenshot H

Screenshot I

Screenshot J

Dm excel

On mobile so I will come back to this to look at the screenshots in detail, but it’s hard to audit by sight much easier if you share the excel with folks to see how you’re linking things up as that can cause a lot of a trouble - general advice though:

- Depreciation: You should always get D&A from the cash flow statement. On the income statement D&A is usually included into a variety of operating expenses (So R&D includes D&A expense for example) and you can get a specific breakdown of where the D&A is by looking at the Notes in the financial statements. Because the CFS must account for all D&A to add back, it is much easier to just use that line as a catch-all.

- Assumptions (especially on growth): It is very elementary (seems like you’re just starting out so I get it) to just average past growth and keep that flat forward. If you keep growth flat, but your expenses are growing a variable rate thats more than revenue growth you would suggest the business will generate less and less cash flow over time. That would make sense why you’re ending enterprise value is so low. This is where we think critically and working in the industry helps because a DCF is literally all assumptions. Try to read news on the business, read free earnings summaries online to get a sense directionally where the business is going. Past performance is not a good indicator of future trajectory - it is backwards looking. Generally speaking, I would take the conpany’s current annual growth rate and determine what their terminal growth rate would be (let’s say 3% to be nice) and do a 10-year DCF tapering down growth from say, 18%, down to like 5% (mature C&R company), then have a 3% terminal growth rate. In that same vein, as growth slows - profitability should improve. So if there is some evidence that can support this, maybe work the conpany’s EBITDA margin up to a sensible level as well. “Sensible” entirely depends on the context of the industry as metrics for C&R is very different than HC or Tech.

- Super low enterprise value: This happens sometimes if you have a genuinely contrarian view of the business, but the larger the delta between your value and consensus value (market value) the more you need to have robust explanations for your assumptions driven by insight or analysis you think everyone else is missing. Down 66% alone does not mean you are wrong, but if you are an expert on the business and have some differentiated insight, you know it’s a clear short position.

The point is, I would try to flex assumptions to get as close to the same value as current enterprise value - then see what it looks like. That’s a good idea of how the street is valuing it. Then your up case is your opinion of what outperformance looks like (maybe growth only slows to 10%, then 3% PGR for example) and your down case is your negative Nancy opinion. You should have a critical eye into the business but that only comes from seeing many similar businesses over a period of time

here is a link to download the excel

https://fastupload.io/bgXXsSJxt3UFshw/file

thanks for the feedback, i’ll read and digest it.

^^^ exactly this. Will have a look at excel file.

thank you for ur feedback

Check WACC and Beta, use comps average unlevered beta. Send model for more insight.

Ab eius sit sunt consequuntur. Quas nihil explicabo qui quasi accusantium. Doloremque minus quo laborum unde maiores qui.

Magnam labore suscipit iure minima sunt ut nisi. Magni repudiandae autem sint enim fugit voluptatum. Eaque totam vel inventore voluptatem est odio laudantium. Delectus et atque ipsum autem qui veritatis qui. Minima possimus ducimus nemo corporis et a et temporibus.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...