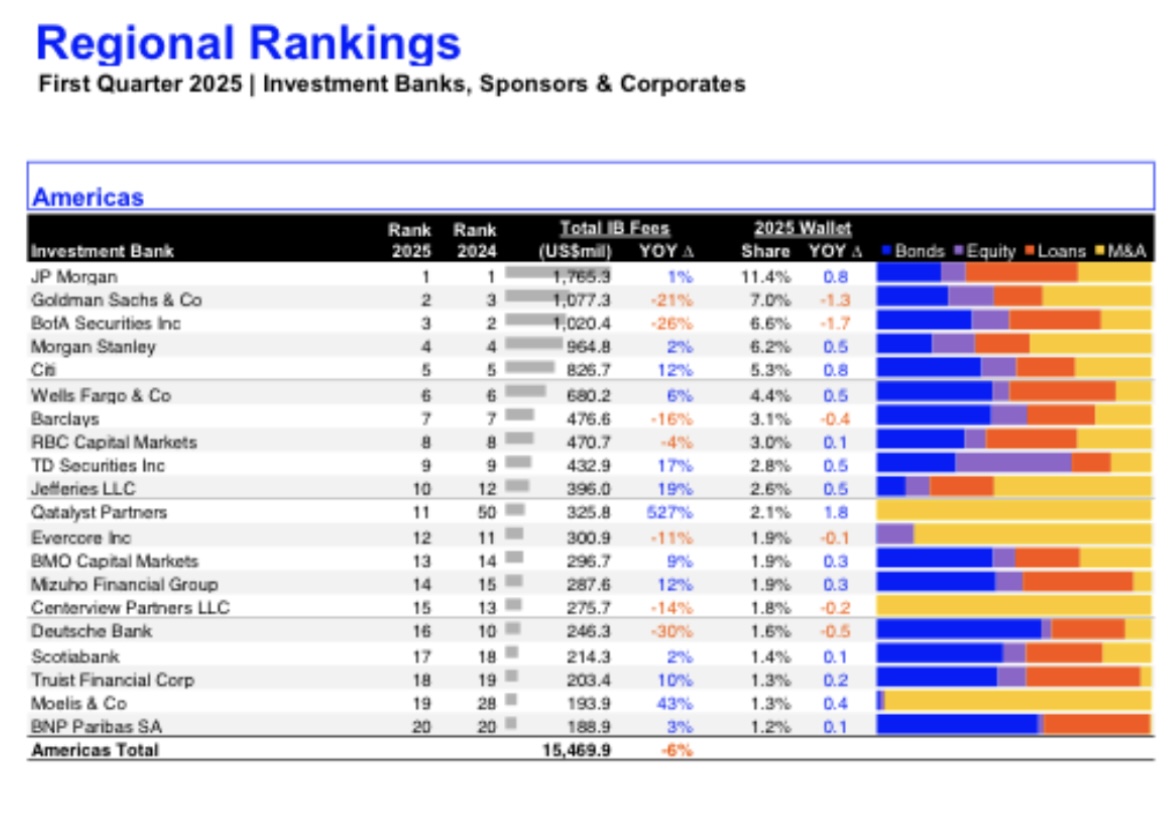

UBS IB Americas Fees Collapse: 25Q1 Fees half of 24Q1 Fees and outside Top 20 (LSEG Data)

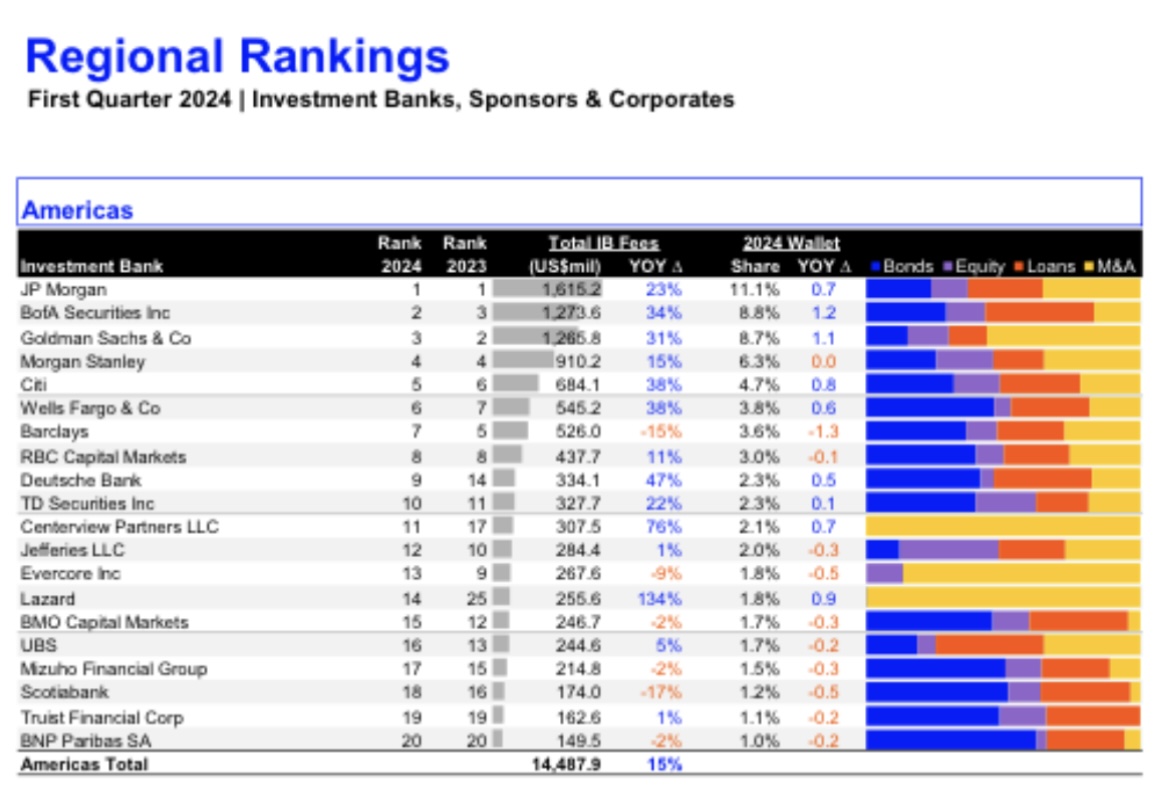

Catastrophic quarter for IB Fees for the bank in the Americas now outside top 20. Q1 25 fees in the Americas estimated at $122m (Subtracting EMEA and APAC from global rev) which is about half of Q1 2024

https://thesource.lseg.com/thesource/getfile/index/7d28c042-0c6f-4a81-b7d4-ebbb6d44b445

https://www.lseg.com/en/data-analytics/products/deals-intelligence/glob…

Damn did anything happen? They fading out their IB bussiness

To think they got CS almost for free and fumbled the bag

Listen I hate UBS as much as the next person but these are all just estimates (read my various previous threads shitting on the firm, MV, and why I would pick a lot of other firms including WF over UBS for reference). Revenues for IB can only be calculated once firms report; these are all extremely preliminary numbers. I would only look at fee revenue calculations for quarters post-earnings.

Think there was a previous post showing UBS is 8th or 9th for Q1 for US M&A as per Bloomberg, and by all accounts. UBS had higher deal flow this quarter than in previous ones, at least for the M&A product. Afaik from what I've heard, weaker LevFin quarter after a really strong relative to UBS 2024. ECM and DCM were, as always, dead for UBS. I can see a reasonable world where they didn't have top maybe 15 fees in the US, but even in such a world, the reason for that would come from lower ECM and DCM fees, not M&A ones. Also want to note deal attribution differs by what source you use, but goes without saying Bloomberg is the best source of finance data as it's by far the most widely used source.

Just as an ending note: listen I think the goal of everyone that is posting about UBS on this forum is simple - expose how much worse a large chunk of UBS has gotten and how the firm has gotten worse culturally post merger. That's not something that can successfully be done by cherry picking data by going to every reputable source and finding that one that has UBS at the lowest ranking (ideal to always use Bloomberg for the most accurate data and failing that maybe CapIQ or Factset) or giving what are at best preliminary estimates, some very real facts and data show how UBS has fallen that we can stick to and paint both a honest and declining view of UBS in the Americas. For example, UBS financials is something like 18th in US M&A by LTM and Tech is also way outside the top 10 or even 15, those are real things that can be pointed to and aren't easily disproven by a quick Bloomberg search by these prospects.

I guess that the previous question asked about confusion on whether the ED that is ex-UBS and always posting about UBS hates or loves UBS has been answered; it hates it. Slick of you to just selectively use data to show it, was for a little bit thinking you were just giving an honest view on UBS, but good to know to also take your thoughts with heavy uncertainty.

We understand you got laid off.

Fees seem like a bit of a lagging indicator, even if ideal for determining whether a BB was actually materially involved in the advisory side of things. Here's Q1 announced for Americas (Mizuho includes Greenhill):

How are fees accurately calcualted before reporting of financials by these firms? If these fees were 100% calculatable and not estimates, you wouldn't get instances of banks beating IB revenue earnings or having significantly higher IB revenue earnings than expected. Think deal volume makes more sense in the absence of that information. Also seems like Bloomberg and LSEG disagree on rankings, which is almost always the case, but particularly present for UBS, as per my previous post, where I posted the Bloomberg rankings, UBS was 8th there and is 12th here. Don't think it changes where the overall flow for the bank sits in the broader tier of things, but interesting difference there.

Also, to get a sense of how much work a bank is doing, shouldn't we be solely looking at M&A fees, not all fees? I am not sure what a bunch of DCM fees or ECM fees have to do to show how much work a bank does in the M&A sector.

UBS Apologist above.

M&A is only one product and even then wether a $10bn deal has one bank or 10 banks it would show up the same using your method. This is a legitimate source and even then a comparison using the same source across two periods…

Just admit there are structural fundamental flaws with the bank in the Americas and some groups need to be overhauled

TD is that high damn... anyone know why?

TD is paradise

It counts Canada, where TD (and RBC) are much stronger... which contrary to popular belief, is not in fact the US but is in the America's. Also, as the data that is being cited shows... It's mostly ECM flow. TD didn't do much M&A this quarter and wasn't even top 15 let alone top 20, in M&A for the US this quarter.

UBS insider here and can confirm that

I wish that I could fly

Into the sky

So very high

Just like a dragonfly

I'd fly above the trees

Over the seas

In all degrees

To anywhere I please

Oh, I want to get awayyyyyy

I want to fly awayyyyyyy

Yeah, yeah, yeah

Fly away fast

Same source for data across two periods.

An estimate but this is a reputable source that looks across all products not just M&A credit claims.

We all know that's BS... look at the data that banks actually use and are the usual suppliers of deal tracking in the US... Bloomberg, FactSet, CapIQ, and Deal Logic are the only ones used very commonly, and where banks pick and choose their rankings from. LSEG is used more in the trading world, not for IB; anyone who works in US IB knows this.

UBS pays for LSEG (Refinitiv) liscences for IB

UBS also pays for dozens of non revenue generating MDs

Mergermarket Q1 league table. Lazard and Rothschild seem to be off to very good starts.

These seem to confirm down by 50%

Yeah I agree, I'm not defending UBS as you assumed.

Isn't 12th around where UBS is LTM (think they are 11th in LTM as per Bloomberg when I checked a few days ago) as a whole though? Just makes it seem like Q1 2024 was more of an odd quarter and the rest are closer in range to a 12th ranking. Also 12th and your claim of off the top 20 are very different.

Credit Agricole new BB

Clients can hear about when you treat employees and clients like shit, assume it causes market share losses

How can you be a BB and then not in the top 20 in the Americas?

The answer is you can’t and it’s not a BB

jeez is there a UBS post everyday

It's the most hated bank on this forum by far and for justifiable reasons. A ton of the groups are useless and toxic, The culture has dramatically gotten worse from when most of the juniors posting here joined; there have been tons of layoffs. It's also a good enough bank to where there are some expectations of it being decent. For example if Nomura or TD (no offense to either, just picking classic MM firms) was trash or declining in the US nobody would care because there are no expectations but UBS has publicly positioned itself as having a lot of expectations post acquisition with the Barclays hires (that have turned into a nightmare for large part) and the announcment of a desire to be a top 6 M&A franchise (which it is not even close to; in the past quarter it finished as a 8-12 ranged bank in M&A EV for the US (depending on what deal tracker you look at).

At a junior level, the bank has devolved from a decent lifestyle shop where you were treated reasonably well to becoming a toxic sweatshop where you get grinded to death on stupid bullshit (MDs aren’t even doing deals) and get paid below street. Your bonus is not getting included in the next round of layoffs. No one at any level is happy and everyone wants to leave. It’s all the worst things about investment banking, combined with endemic unsolvable bank-specific issues and it is a total nightmare. The top performers keep leaving, and then the few competent people keep getting crushed, and then they leave and the cycle continues until the only people left are incompetent people who can’t find a new job or people who are trapped because of their visa. It’s so not worth it and incoming interns and analysts should find something else to do with their lives.

I have no dog in this fight, but can somebody pls explain to me all this recent UBS slander...?

Bank is collapsing and tripping over itself

TL;DR: UBS has a few high-performing groups but is struggling overall in the Americas. Cultural deterioration, underperforming MDs, below-market comp, and inconsistent deal flow have led to growing discontent. What’s particularly important is the wide variance in group quality; some are top-10 in their space and closer to BB level (I think previous comments indicate 3 coverage groups and LevFin/Sponsors as t10 in M&A TEV for LTM), while others have virtually no flow and toxic dynamics (kind of seems like the rest of the groups from the ED's and others comments).

UBS isn’t objectively terrible in M&A (deal flow data in this thread shows they’re still mid-tier overall in the sense of being clearly below the top and mid-tier BB/EB's but also clearly above the MM's and firms like DB), but the firm is in a rough, transitional spot. The backlash is amplified by two things: A) the sharp cultural decline since many juniors were recruited, and B) UBS’s public positioning as a “culture bank” and its aggressive self-promotion around growth, which set expectations it hasn’t lived up to.

It has grown at a way slower rate than their headcount growth, diluting the esperience for everyone

Echoing the posts above. My group has gone from being a lifestyle group to a grindfest toxic group. Only constant is no deal flow.

For the first time considering quitting or ask to be laid off.

Which group? HC? FIG?

Has to be Tech

Calm down

Another banger

Baby, calm down, calm down

London bridge has fallen

Molestiae voluptatem qui iure distinctio. Unde delectus quod similique fugiat optio repellendus.

Vitae harum qui illo eos dolores reprehenderit odit accusamus. Itaque aut veniam fuga qui non est minus. Molestias et quos consequatur natus et.

Cumque reiciendis aut eligendi. Sint ipsum et non doloribus.

Omnis deleniti deserunt dolorem atque. Aut distinctio numquam id facilis necessitatibus. Quisquam officiis excepturi commodi et molestiae natus exercitationem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Culpa et qui dolorem sint ab explicabo. Omnis autem ratione occaecati rerum suscipit soluta in qui. Officiis sed tenetur repellendus velit.

Eos aperiam quis vel quis harum. Eius necessitatibus aut qui non sit mollitia enim perferendis.

Laborum soluta earum fugiat fugiat. Iusto rem necessitatibus nihil ut. Natus deleniti quidem quia eos. Sequi ut magni molestiae aut aut.

Soluta in optio atque autem ut. Unde nihil et sed reiciendis inventore et distinctio. Impedit in adipisci eaque repellendus et perspiciatis. Excepturi et ea harum. Iure nesciunt impedit fugiat numquam est sed accusamus. Expedita distinctio repudiandae sed dicta aut. A quis nulla sint nulla occaecati et ab quod.