Derivatives Market

They are securities that drive their value in whole or in part by having a claim on some underlying security

What Is The Derivatives Market?

A derivatives market is a financial exchange where futures and options are traded. It contains financial instruments that individual and institutional investors utilize for speculating or hedging. The leading players in this market include hedgers, arbitrageurs, margin traders, and speculators based on their trading objectives.

Exchange-traded and over-the-counter derivatives comprise the two main segments of the global derivatives market. These derivatives have varied legal statuses and trading methods, which can vary from nation to nation.

Credit Default Swaps (CDSs) contributed to the economy's collapse during the financial crisis of 2007–2008, and since then, corrective measures have been enacted.

Exchange-traded derivatives comprise options and futures contracts, although over-the-counter markets may also contain swaptions, forwards, options, and futures contracts.

Based on their trading goals, participants in a derivative market can be divided into four groups.

- Hedgers

- Investors

- Arbitrageurs

- Margin Traders

Derivatives are criticized and misused as the stock market's big traders start involving gambling and destabilizing the market.

-

Derivatives are financial securities whose value depends on underlying assets like stocks, bonds, or commodities and are used primarily for risk management.

-

They possess characteristics like liquidity, low transaction costs, and global trading popularity, making them attractive for investors and firms.

-

Derivatives serve two main purposes: speculation to earn profits and hedging to minimize potential losses

-

Participants in the derivatives market include hedgers, speculators, and arbitrageurs, each with different objectives and risk tolerance.

-

Derivatives encompass various types, such as

-

financial (currency, interest rate, equity)

-

and non-financial (weather, commodity) derivatives, providing tools for risk management and investment opportunities.

-

Understanding Derivatives Market

Derivatives can be exchange-traded or traded over the counter (OTC). The term "exchange" refers to the officially recognized stock exchange where securities are exchanged, and participants are subject to certain rules.

In contrast, the OTC market is a dealer-oriented, disorganized market where trading occurs over the phone, by email, etc. In addition, the exchange uses standardized, controlled derivatives.

On the other hand, a larger percentage of derivatives contracts are OTC derivatives, but they are unregulated and have a higher counterpart risk. The following factors have been driving the growth of financial derivatives:

- Increasing financial market asset price volatility.

- More extensive fusion of domestic and foreign financial markets.

- Substantial improvement in communication infrastructure and a sharp drop in expenses.

- Creation of more advanced risk management systems that give economic agents additional options.

- Innovations in the derivative markets integrate risks and returns throughout a wide range of financial assets in the best possible way, resulting in higher returns and lower risks.

Some of the operators in the derivative market are:

1. Hedgers

Hedger wants to reduce and transfer a risk component to safeguard their existing portfolio holding. They are not in the derivative market to make a profit.

2. Speculators

Speculators intentionally take the risk from hedgers in pursuit of profit for a short period. They are willing to take risks and depend on whether the markets would go up or down.

3. Arbitrageurs

Arbitrageurs operate in different markets simultaneously to pursue arbitrage, wanting to gain price mismatch with almost ‘no risk.’ They buy in one market and sell in another.

They could be making money even without putting their own money in, and such opportunities often come up in the market but last for a very short timeframe. This is because arbitrageurs take advantage when the situation emerges, and demand-supply forces drive the market back to normal.

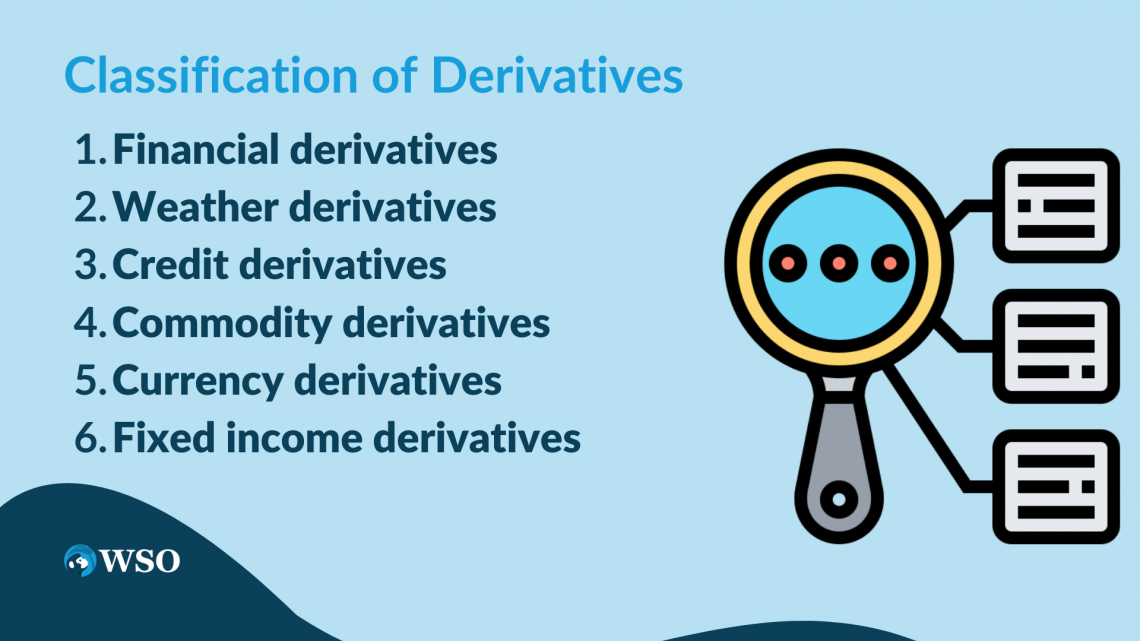

Classification of Derivatives

Derivatives are securities that drive their value in whole or in part by having a claim on some underlying security, such as stocks, bonds, currencies, commodities, precious metals, market indexes, reference rates, interest rates, and foreign exchange rates.

These are known as “Bases.” Derivatives are classified into financial and non-financial. Non-financial cover commodities, metals, weather, etc.; financial derivatives are forwards, options, credit, and swaps.

Derivatives have no intrinsic value of their own. Forwards, futures, options, swaps, caps, floor, collar, etc., are commonly used derivatives. They are tools used by a firm or an investor to reduce risk.

Characteristics of Derivatives:

- They are liquid and have low transaction costs.

- The margin requirements for derivatives are relatively low, reflecting the relatively low credit risk associated with derivatives.

- They are traded globally and have strong popularity in financial markets.

- Taking a short position in derivatives is more comfortable than in other assets. An investor is said to have a short position in a derivative product if he is obliged to deliver the underlying asset on a specified future date.

Now, let Us discuss the types of derivatives.

1. Financial derivatives

They are useful in controlling risk and hedging funds. There are three types:

- Currency futures, where the position involves foreign currencies.

- Interest rate futures, where the position involves fixed-income securities.

- Equity futures, where the position involves equities.

2. Weather derivatives

Weather affects the product's volume of production and sales price. Therefore, revenues are adversely affected by it. Hedging through weather derivatives minimizes the risk exposure of the companies having agriculture products or power generation.

Weather derivatives enable businesses to hedge against unpredictable temperature swings, thus managing risk and increasing profit.

3. Credit derivatives

It is an instrument that allows credit risk to be priced and traded independently of market risks like interest rate and currency risk. It reduces the risk related to loans. It helps banks, insurance companies, mutual funds, pension funds, etc.

Note

Market and credit risks are the two main hazards businesses experience in each financial transaction.

Market risk occurs when fluctuations in interest rates, foreign exchange rates, stock prices, and commodity prices reduce a company's worth. However, credit risk is present when the company fails to make required payments to counterparties on schedule.

4. Commodity derivatives

It includes physical products like zinc, nickel, gold, and silver. In the case of commodities, a contract varies widely based on the quality of underlying assets.

5. Currency derivatives

It is a contractual agreement between buyer and seller for purchasing or selling a particular currency at a specified future date at a predetermined price. One of the “pairs” of currencies is invariably the US$.

6. Fixed-income derivatives

Market participants are now more vulnerable to several dangers due to the economy's deregulation of interest rates. Fixed-income derivatives were allowed in the OTC market to monitor and control risks and expand the money market.

Hedging in the derivatives market

Hedging is used to reduce risk by using derivatives. It covers derivatives market positions designed to offset the potential losses from the existing cash market positions.

Example: An income fund has a large portfolio of bonds. This portfolio stands to make losses when the interest rate goes up. Hence, the fund may go short on interest rate futures to offset this loss.

Three issues define the objective of hedging:

1. Hedging for firm

Corporations will choose a reduction in the variability of corporate income as an appropriate target.

2. Firm’s exposure to financial price risk

There are three types of risk for every financial price to which a firm is exposed.

- Transactional risk means fluctuations in financial prices on the cash flow from purchases or sales.

- Translation risk means changes in the value of a foreign asset due to changes in the foreign exchange rates.

- Economic exposure means the impact of fluctuations in prices on the core business of the firm.

3. The various hedging instruments available in the corporate treasurer and how they behave in different pricing environments.

The ability to operate within the parameters of their shareholder-defined restrictions and select the hedging vehicle for a certain exposure and economic climate distinguishes a great corporate treasurer from a mediocre one.

In addition to the goals above, improved risk management through hedging has the following benefits:

- Debt Capacity Enhancement

- Increased focus on operations

- Isolating management performance

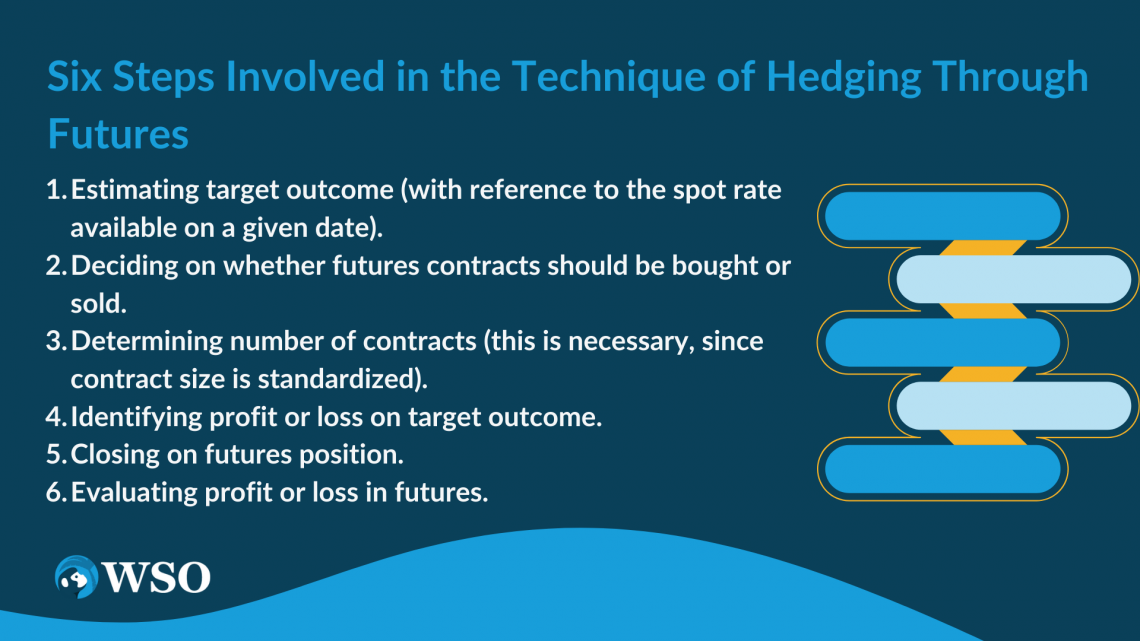

Hedging with Futures Contracts

There are six steps involved in hedging through futures. These are

- Estimating target outcome (regarding the spot rate available on a given date).

- Deciding on whether futures contracts should be bought or sold.

- Determining the number of contracts (this is necessary since contract size is standardized).

- Identifying profit or loss on a target outcome.

- Closing on futures position.

- Evaluating profit or loss in futures.

The derivative market, also known as the credit market (of which the futures market is a part), is one in which the price is fixed on one day, and the delivery and settlement are done on another date later.

Hedging's main goal is to lessen the "price risk" associated with a position taken in the cash market. An investor can use a futures contract as a hedge by establishing a position opposite to one in the cash market. Long or short positions are both possible. The terms "long" and "short" refer to bought and sold positions, respectively.

Swaps In the Derivatives Market

A swap is a derivative in which two counterparties agree to exchange one stream of cash flows against another stream. These streams are called the legs of the swaps. As a result, the counterparties can profit from movements in price without posting the notional amount in cash.

A swap can create unfunded exposure to an underlying asset and hedge certain risks, such as interest rate risk. These are the following generic swaps;

1. Interest rate swaps

It is an arrangement whereby one party exchanges one set of interest rate payments for another. They can be used to manage fixed or floating assets and liabilities and unfunded bond exposures to profit from changes in interest rates.

Interest rate swaps can be fixed-for-fixed, fixed-for-floating, or floating-for-floating. In addition, the legs of the swap can be of the same currency or different currencies.

2. Asset swaps

The portfolio consists of fixed-rate notes and an interest rate swap that pays fixed and receives floating to the stated maturity of the underlying fixed-rate note.

3. Currency swaps

These are arrangements whereby currencies are exchanged at specified exchange rates and intervals. It involves an exchange of cash payments in one currency for cash payments in another.

Note

A currency swap is an easy alternative for companies investing abroad. The basic purpose is to lock in the rate. It allows these companies to enter into new markets and raise capital.

4. Credit swaps

Credit swaps pay the buyer protection of a given contingent amount at a given credit event, such as default.

Contingent Amount = Face Value of Bond – Market Value paid at Default Time of Underlying Bond

In return, the buyer of protection pays an annuity premium till the maturity date of the credit swap or credit event, whichever is earlier.

5. Commodity swaps

It is an agreement involving exchanging a series of commodity price payments against variable commodity price payments resulting exclusively in a cash settlement.

6. Equity swaps

An equity swap is a special type of total return swap. Here, the underlying asset is the stock or stock index. In it, you do not have to pay anything upfront.

products in the Derivatives market

The derivative is a product that does not have any value. Instead, it derives value from some underlying.

It is a one-to-one bipartite contract to be performed in the future. Buyer and seller can enter a forward contract for any goods, commodities, or assets.

- It provides flexibility regarding the contract price, quantity, delivery time, and place.

- No money is involved at the time of deal is signed.

- They are not traded on an exchange but traded on over-the-counter.

- Poor liquidity and default risk.

2. Future contract

These are organized contracts for quantity, delivery date, time, and place traded on exchanges to help with secondary market trading. They are fluid in character.

- The clearinghouse provides the settlement guarantee for each trade to buy and sell commodities at a predetermined future date at a specified price.

- Minimum and maximum fluctuations in prices may be fixed.

- The buyers and sellers have to deposit some margin in the form of cash to ensure the honoring of the deal.

- There is a market-to-market daily, i.e., profit and loss are calculated daily. If there is profit, one will receive it; if there are losses, one needs to pay the exchange.

Since both serve the same function and work through a contract between counterparties, one may wonder if future contracts are similar to forward contracts. The difference is in terms of standardization (contract size) and method of operation (organized exchange trade).

Note

Futures contracts could be used to hedge risk. However, in forward contracts, the seller must deliver to the buyer on the due date, and the buyer will pay the seller the agreed price.

3. Options

It represents claims on an underlying common stock that investors create and sell to other investors. There are two types of options- call option and put option.

Call option (option to buy) gives a holder a ‘right to buy’ an underlying asset by a certain date. Conversely, the put option (option to sell) gives the holder a ‘right to sell’ an underlying asset.

- An investor who writes a call option against stock in his portfolio is said to be selling a covered option.

- Options sold without the stock to back them up are called naked options.

- Clearing house guarantees performance. Thus, no risk of default.

Conclusion

The myth is that “derivatives increase speculation and do not serve any economic purpose.”

There is widespread agreement, both in the commercial and public sectors, that derivatives give numerous and significant benefits to various/different consumers. For example, using derivatives, users can manage their exposure to interest rates, commodity prices, securities prices, and other factors cheaply.

The commodities market first felt the need for derivatives as a hedging tool. Agriculture futures and options helped farmers and processors hedge against the risk of commodity price fluctuations.

The period of the Bretton Woods Agreement was marked by some remarkable innovations in the financial markets, such as:

- Introduction of floating rate of currencies

- Increased trading in various derivative instruments

- Online trading in the capital market

As the complexity of instruments increased manifold, the accompanying risk factors grew in gigantic proportion. This situation led to more development in derivatives as risk management tools for various market participants.

Spot markets are for immediate delivery, while forward markets are for deferred delivery. Finally, the margin is the “good faith” deposit to ensure contract completion.

Options include a smaller investment than transacting in the stock, knowing the maximum loss in advance, leverage, and expanding the opportunity set available to investors.

or Want to Sign up with your social account?