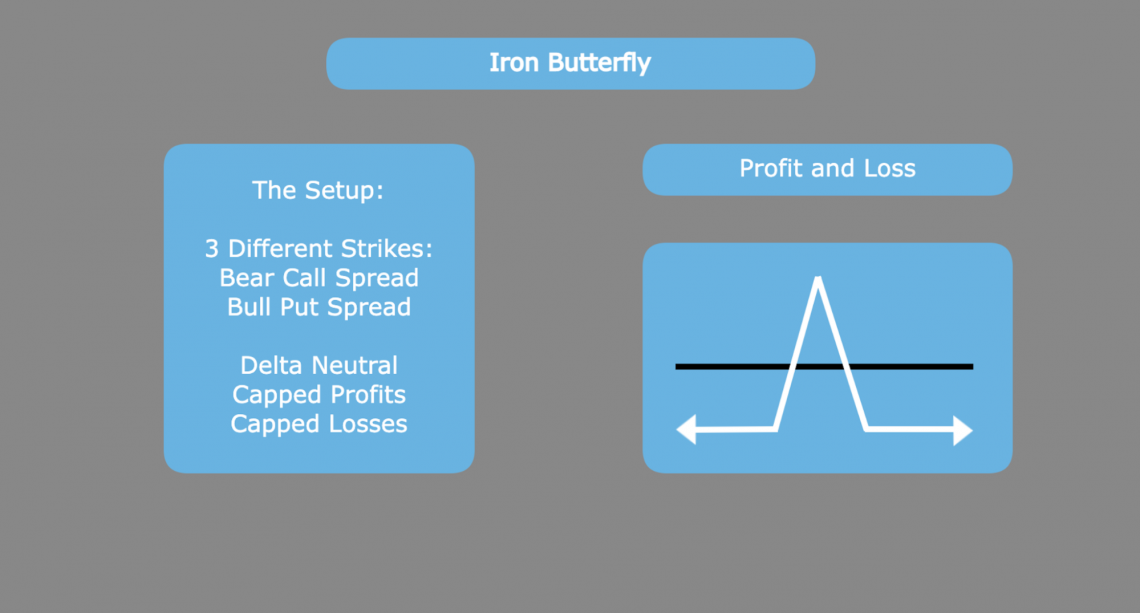

Iron Butterfly

An options strategy consisting of four different legs: two puts and two calls, each expiring on the same day at 3 different strikes.

What Is An Iron Butterfly?

The iron butterfly is an options strategy consisting of four legs: two puts and two calls, each expiring on the same day at three different strikes. These four legs combine to create a delta-neutral strategy aiming to collect a premium.

The most common iron butterfly setup includes two contracts sold at the money and two purchased out of the money.

This means that a vertical put spread will be sold with its long leg below the current market price, and a vertical call spread will be sold with its long leg above the current market price. As a result, both short legs in the two spreads share the same strike: at the money.

These two spreads are individually known as a bull put spread and a bear call spread. The goal is that the underlying expires as close to the short put and short call as possible.

Combining these two spreads, it is clear that the butterfly's profit is maximized when the underlying stock's market price falls exactly at the middle strike at expiration. Conversely, as the price increases or decreases, one of the sold contracts becomes in the money, reducing profit.

Because investors want the price to fall very close on either side of this middle strike, it is also said that they are expecting low volatility.

A volatile stock would be less likely to expire near the middle strike and is much more likely to move far enough that it leaves the investor with a loss.

Although options traders looking to implement the butterfly as an investment strategy are typically neutral, it is possible to construct the strategy slightly bullishly or bearishly.

The investor would move their maximum profit range up or down by creating the iron butterfly with the middle strike either below or above the current price. The conviction would, therefore, be slightly bullish or bearish, respectively.

In short, the iron butterfly is a strategy that:

- Is delta neutral

- Bets on low volatility

- Has capped potential for both profits and losses

- An Iron Butterfly is an advanced options trading strategy that involves four options contracts: buying a lower strike put, selling a middle strike put, selling a middle strike call, and buying a higher strike call.

- The Iron Butterfly consists of a combination of a bull put spread and a bear call spread centered around the same strike price. This creates a "wings" effect, with the middle strike representing the body of the butterfly.

- The strategy profits when the underlying asset’s price stays close to the middle strike price at expiration. The maximum profit is achieved if the asset’s price is exactly at the middle strike.

- The Iron Butterfly benefits from stable market conditions and low volatility. If the underlying asset's price remains near the middle strike price, the strategy can generate significant profits.

Vertical Spread Components

As mentioned before, the strategy depends on being delta-neutral. The investor does not pick which direction the stock moves to be profitable. A combination of matching vertical spreads achieves this goal.

For the iron butterfly, there are two vertical spreads used. Individually, both of these strategies are examples of credit spreads. The two legs result in a net premium collected because short legs are more expensive than long ones. These spreads include:

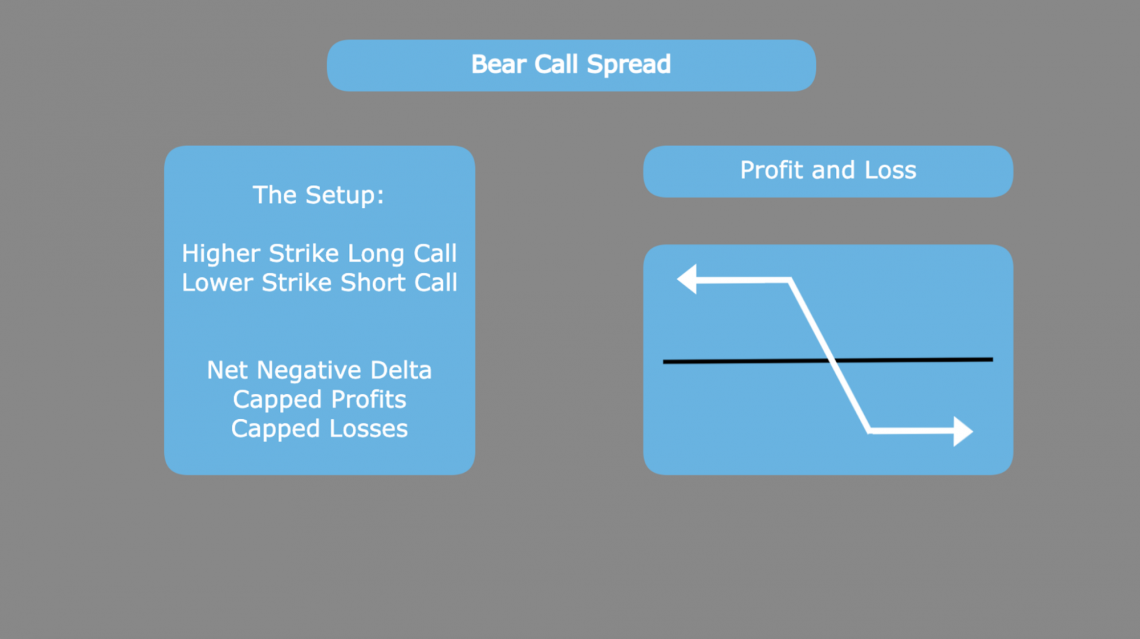

On its own, the bear call spread strategy is a moderately bearish bet. In this strategy, the investor opens a long call at a lower strike and a short one at a higher strike.

The combination of these two options legs creates a net negative delta, as the higher-strike short call will always be farther from the money or less in the money than the lower-strike long call.

The strategy itself has both a maximum profit and loss. The gain is maximized because the premium is initially collected. The long call also reduces the total premium, which is opened to hedge any risk that the short position creates.

The maximum profit of a bear call spread strategy is the total premium collected from selling the spread as a whole. Conversely, the maximum loss is the strike difference multiplied by 100 minus the total premium collected to enter the position.

Therefore, the investor's goal is for the price to remain below the short leg, where the profit remains maximized.

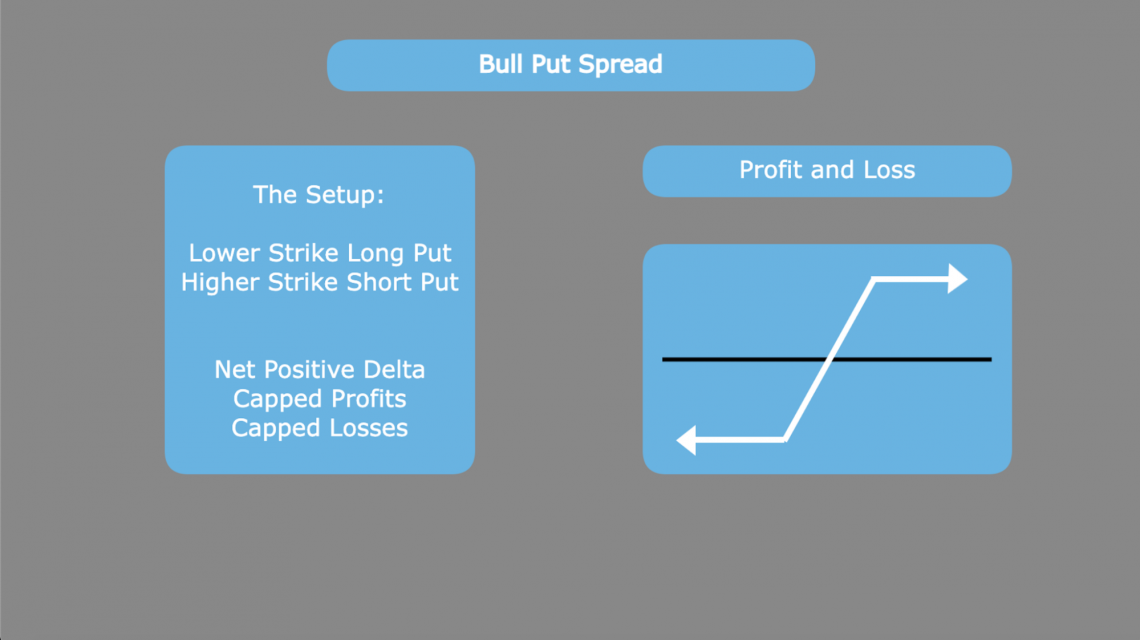

The bull-put spread strategy, on its own, is a moderately bullish bet. In this strategy, the investor opens a long put at a lower and a short one at a higher strike.

The combination of these two options legs creates a net positive delta, as the lower-strike long put will always be farther from the money or less in the money than the higher-strike short put.

The strategy itself has both a maximum profit and loss. The profit is maximized because the premium is initially collected. This total premium is also reduced by the long put, which is opened to hedge the risk that the short position creates.

The maximum profit of a bull put spread strategy is the total premium collected from selling the spread as a whole. Conversely, the maximum loss is the strike difference multiplied by 100 minus the total premium collected to enter the position.

Therefore, the investor's goal is for the price to remain above the short leg, where the profit remains maximized.

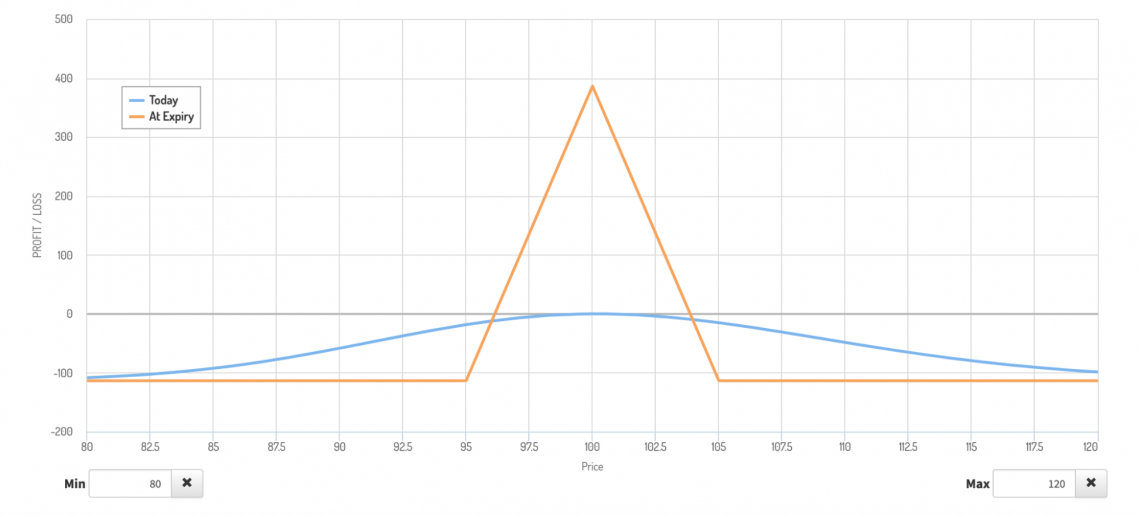

Iron Butterfly Example

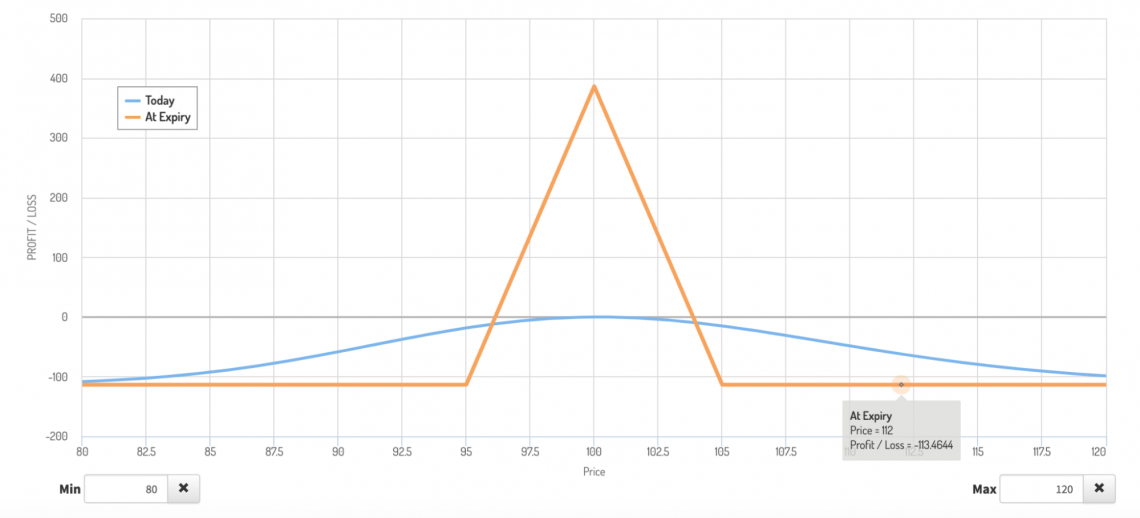

For this example, stock XYZ is currently trading for 100. The following call and put options expire in 30 days with an implied volatility of 30.

Looking at the profit and loss graph, we can see that the maximum profit is exactly at the short strike of 100.

The profit is the net premium collected from the four contract legs when the two contracts are sold.

The collected premium will always equal the sum of individual premiums for the respective call and put spreads included in the contract.

In this example, the net credit is around $386.54. If we look at the bear call spread and the bull put spread components, we see that the premiums are $189.64 and $196.90, respectively.

When added together, these two premiums give us the total premium for the iron butterfly. Our example checks out.

Max Profit = Total Premium = Bear Call Spread Premium + Bull Put Spread Premium

As with vertical credit spreads, the premium determines the maximum loss and the break-even points.

In this case, the maximum loss would occur when the long call or long put becomes in the money. Then, the long options cover the short contract obligation, stopping the losses.

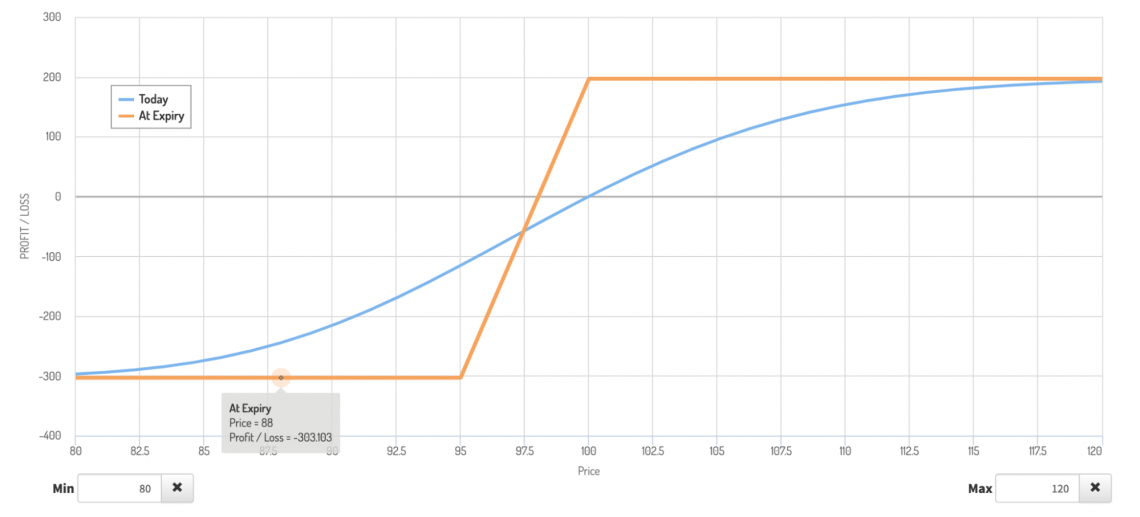

Looking at a situation where the underlying drops to $88, we see the iron butterfly reach its maximum loss because the embedded bull put reaches its maximum loss. This loss is the same at any point below $95, the long put's strike.

Looking at the bull put spread, we see a maximum loss of $303.10. This is equal to the difference between the strikes, multiplied by 100 (as each contract controls 100 shares) minus the premium collected. In this case, $500 - $189.90 gives us our max loss.

Our iron butterfly, however, has a loss of less than $303.10. This is because the bear call spread expired out of the money. The additional premium from that option brings us to our actual loss of $113.46.

Looking closely, this is equal to the difference between the strikes and the premium collected. In this case, however, the extra premium collected from the bear call spread helps to lower the loss overall.

Max Loss = Strike difference x 100 - Contract Premium

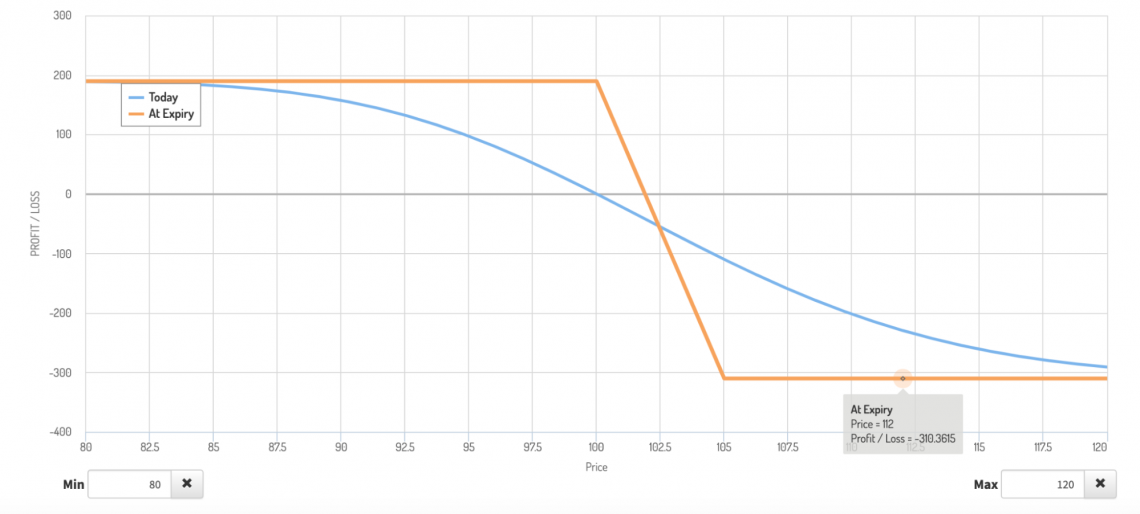

What is the downside of collecting this extra premium? At specific points, if the price rises too high, the bear call spread is, instead, in the money. This means there is also a potential for losses if the price moves up instead of just if it moves down.

Looking past the long call $105 strike, we see where the bear call spread reaches its maximum loss.

Once again, the strike difference leaves the investor with a $500 loss, partially offset by the $189.64 in premium collected. As a result, the bear call loses the investor $310.36 overall.

As was the case in the situation with a big price decline, the loss on the in-the-money spread is further offset by the premium of the opposing spread. In this case, the bull put spread is out of the money and helps take away the loss of the bear call component.

Regardless of the direction of the price movement, there is no situation where both vertical spreads are in the money. For this reason, the maximum loss is smaller, but there is a chance for a loss regardless of the direction of price movement.

Final Considerations

While we can summarize the key points regarding an iron butterfly in a few points, investors looking to use this strategy must be aware of other potential risks and factors that can affect this strategy's profitability.

First, the key points:

- The iron butterfly is a delta-neutral strategy, and investors do not need a directional conviction on the underlying asset.

- Both the profit potential and loss potential for the strategy are fixed.

- This strategy involves four legs, which we can break down into two distinct vertical spreads.

Beyond these basic points, there are a few other aspects that can affect the profitability of the iron condor strategy. Therefore, we must take these aspects into account before entering a position.

The most important of these is the difference between actual and implied volatility. Every option contract has implied volatility, which the contract price can determine.

Supply and demand for option contracts typically make the implied volatility reflect the likelihood of actual movement relatively well. This is because there will be more demand for options of moving contracts due to the greater chance of profit and vice versa.

In situations where the investor is betting on low volatility, such as the iron butterfly, investors should consider how the implied volatility of the contract compares to their actual volatility expectations.

Higher-volatility contracts will fetch a greater premium but are more likely to move away from the middle strike.

Investors would be smart to enter a trade when they think the implied volatility of the contract is higher than the volatility they expect during the contract's lifespan.

Selling a contract with the actual high volatility likely to have its implied volatility lowered in the future will generate extra premium while offering less risk.

Beyond understanding volatility and its implications on price, traders must be aware of the early assignment risk present with short option legs. This is especially important when there is a dividend before expiration.

The call option holders may decide to exercise if they think the dividend payment will be greater than the remaining time value in the contract. Conversely, put option holders may exercise if they feel the time value exceeds the dividend.

Depending on the account specifications, an early assignment can be quite impactful. If there is no sufficient balance in the account, liquidation may occur, which is a very real and extreme risk. It has caused some traders to lose thousands of percent on their positions.

As with all options strategies, there is a greater degree of risk associated with increased leverage when using an iron butterfly. Beyond just understanding the setup, investors should have an understanding of equity valuation based on fundamentals.

For this strategy, it is fair to say that an investor thinks a stock will not have a drastic move in price. An investor may come to this conclusion if they feel that the company's fundamentals designate that the stock's current market price is the fair value.

Feel free to check out our financial modeling course to understand these concepts better. Due diligence in the underlying and a strong conviction of price movement is a must-have when using strategies susceptible to extra volatility.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?