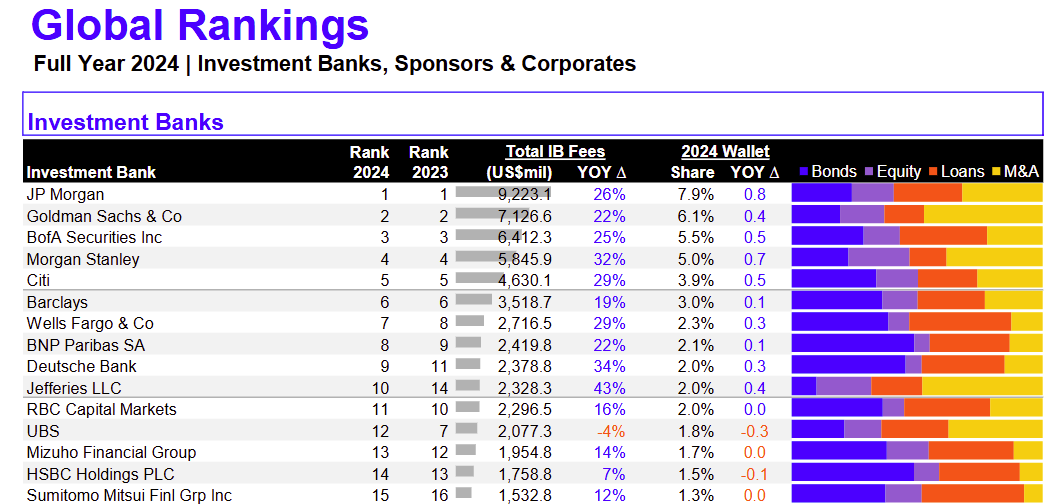

UBS: The Bulge Bracket Remains a Distant Dream

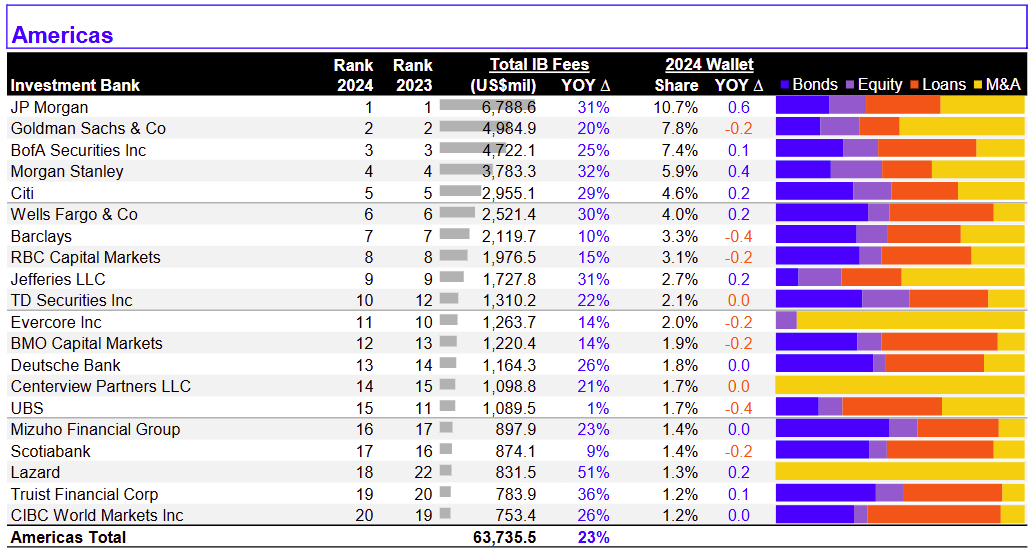

UBS couldn't manage to eke out a position in the top ten in the Americas (#15) and globally (#12).

UBS couldn't manage to eke out a position in the top ten in the Americas (#15) and globally (#12).

| +433 | Don’t work at UBS - UBS Sucks | 40 | 28m |

| +327 | Article - UBS’ Investment Bank Keeps Losing Ground | 41 | 4d |

| +182 | Should My Intern Get a Return Offer? | 53 | 2h |

| +63 | When to Leave Office as Intern | 8 | 5d |

| +56 | F*ck it I'm Going to Med School | 19 | 1d |

| +39 | What do you say to ppl who don’t know EVR/LAZ/CVP/PJT | 29 | 23h |

| +39 | Would you rather be a Touse Squid or a Bouse Mogger in IB | 2 | 5d |

| +36 | Living in greenwich as an analyst? | 7 | 1h |

| +32 | STEM student lost in London IB recruiting | 18 | 6h |

| +26 | lateral hire from Corp Dev to ECM IB (No IB experience) | 10 | 16h |

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

Just commenting on the other post b/c this is very applicable. Also the original article post is from April 2024. Just want to note that before commenting anything b/c this is basically an article that is during integration times, UBS went through massive restructuring in the 1H 2024.

UBS Tech is a massive reason for their lower rankings than last year. Tech should take up 30-40% of a bank's wallet and was the big industry this year, it takes up 5-10% of UBS. This alongside a lack of energy business, one of the largest sectors this year, means UBS is going to do worse overall. Certain groups improved such as Industrials and LevFin they will get fine bonuses. Some groups dramatically dropped the ball like Tech and M&T which will reflect in their bonuses.

Honestly impressive that it's even up 1% b/c that 2023 number includes some tech and M&T deal flow, primarily from the old CS franchisewhilst there is none this year outside of ECM+ LevFin-led things.

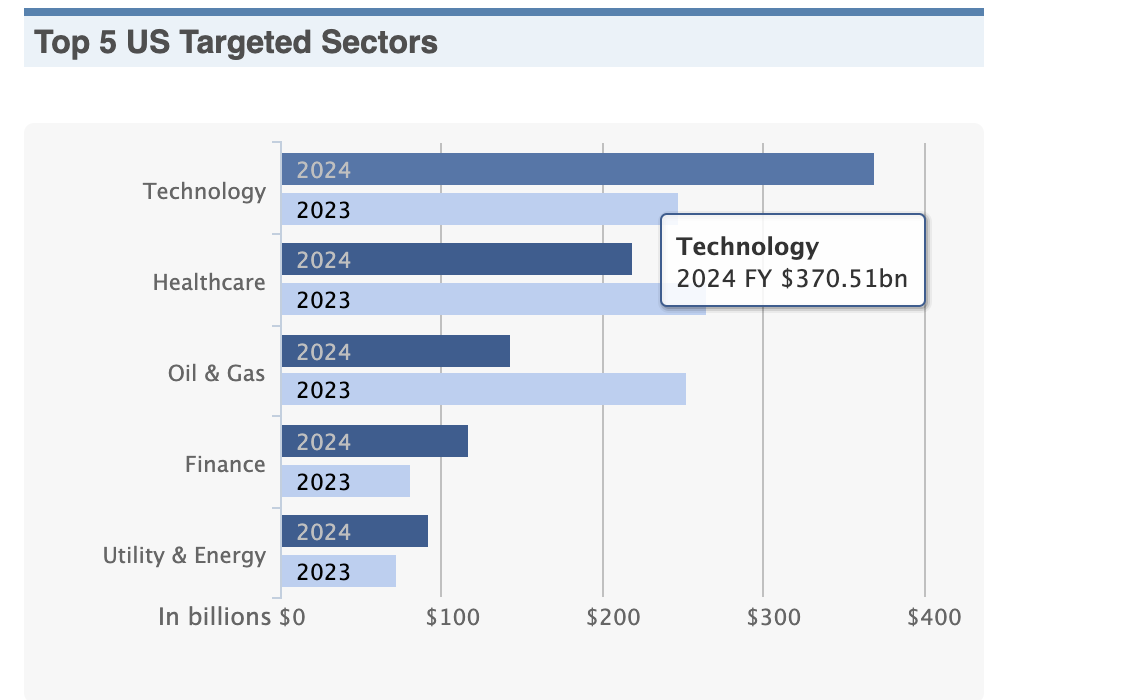

Edit: Just want to note that basically, no competing bank has Tech underperformed as much as UBS has, which is super relevant given it was by far the largest sector seeing almost $ 100B increase in M&A volume. That's basically all the transaction volume of the financials industry combined for 2024. UBS's strong suit industries in Industrials and Financials saw significantly less increase in overall deal flow, despite UBS's market share increasing. HC also saw a slight UBS market share increase but the healthcare M&A sector actually shrunk this year from ~$265Bn to ~220Bn. UBS outside of tech was better than last year.

WSJ league tables for reference:

Check FactSet for additional data; but UBS Tech had a decrease in market share whilst other groups such as LevFin, HC, GIG had increased. The problem for UBS is that this year was so Tech dominated that the bank saw a nearly flat overall bottom-line with only low single-digit fee growth because the tech team did so much worse when the broader tech world did so much better.

To summarize: UBS performed roughly the same as last year with some improvements in some groups market share wise, but the tech group massively dragged it down in a year dominated by tech transactions.

Easier way to understand this/different comment from last post to easier understand this:

The biggest sector this year by far was tech; the sector was so large that it was basically the combination of the next 2 largest sectors in M&A. Now in this sector, UBS massively declined but improved in most other sectors including the second and 4th largest sectors in M&A. The thing that is not reflected because WSJ does not give as much data as Factset does, but WSJ is the best that I can post since Factset is work-related content and I do not want to post from there. Additionally, the 3rd and 5th largest sectors are sectors in which UBS does not do business. UBS has as mentioned improved market share in most of it's other sectors, it's pretty clearly tech that is a large part of the issue for UBS with a lot of the rest coming from a distinct lack of O&G deals since again UBS doesn't do O&G but O&G was a massive sector this year in the US for this specific year.

I am not out here defending UBS, merely explaining what the state of the bank is. This also means acknowledging what the source of the struggles are and which groups are doing well and which ones are not.

Will UBS return to being around the 8-12 range in the Americas? Really depends on what the industry mix for deal flow looks like, but if less tech-heavy then most likely yes. If more tech heavy then most likely no. Alternatively, they could fire this tech team now and bring in new MDs or bring in even more tech MDs in the hope to finally make tech not be completely useless.

I know UBS shut down their Oil and Gas group but do they not have a group there now of CS people? CS still had an O&G group at the time of acquisition.

TLDR bad bank and let’s scapegoat one group in the entire IB. A couple thousand bankers globally, let’s focus on less than 100 in one group

Not what I said, please re-read. There are some good groups at the firm such as Sponsors and LevFin. I am also not scapegoating, just explaining the standing in the league table, which is reflective of the environment in the year, which this year was tech-heavy which is where UBS struggled the most. These are just facts, it doesn't matter if it hurts the tech team's feelings. Also, I don't speak for the global bank, as Idk much about what is happening in Asia or Europe.

Important to note that 1H UBS was a time of massive restructuring of UBS as well, 2H UBS was better than 1H globally and within the US. Also logical to not give mandates to a bank going through integration as clients would not know if the senior they have a relationship with will remain there. Even if a bit unfair to UBS, momentum leads to more deals so it should be taken into account when evaluating the bank. However, from a global perspective, 2023 seems a bit more reflective than 2024 especially since even pre-acquisition UBS was close to the 8-10 range than 12th globally. Regardless, I again cannot speak to the state of the Asian or European banks so hard for me to truly comment on it outside of speculation.

The decline continues… they are getting worse each year and will become what the UBS IB has always been, simply a service for wealth management clients without significant origination capability. For full year 2024, they rank at or below 2024 1H for the main metrics below. There is no momentum and look for the slide to continue into 2025.

https://www.lseg.com/en/data-analytics/products/deals-intelligence/glob…

Rankings:

Global IB Fees

2022 CS+UBS: 6 (CS: 7, UBS: 21)

2023: 7

2024 1H: 11

2024: 12

Global M&A

2022: CS+UBS: 6 (CS: 12, UBS: 14)

2023: 9

2024 1H: 10

2024: 13

Sponsors Fees

2022 CS+UBS: 2 (CS: 5, UBS: 14)

2023: 6

2024 1H: 7

2024: 7

Americas Fees:

2022 CS+UBS: >= 8 (CS: 8, UBS: Unranked)

2023: 11

2024 1H: 14

2024: 15

Del

Translation: If you don’t show UBS is doing great it’s misinformation.

If you disagree come with your own data or stfu. If you think LSEG/Refinitiv is wrong then email [email protected] with your specific concerns.

Can’t be bulge if you are not top 10..

they are too bad to be a bulge bracket bank, but not good enough at Middle market deals to be a middle market bank.

i propose a new category for the not quite bulge bracket banks

We pay you a lot, so we can treat you however we want -UBS MD

UBS no longer listed as bulge example:

https://prospectrockpartners.com/bulge-bracket-bonus-schedule-2025-what…

Neither is Barclays or DB according to your logic…

Would say Barclays yes, DB no

If you think Barclays isn't a BB, idk what to tell you.

If you have high standards for what to call a BB can make the case there are only 5, and Barclays clearly 6th behind all of them. Big drop off after that though

BB status is earned and not given. UBS no longer BB in any sense of the word

Dream on

BNP the next BB

It’s a no from me dog

Good one!

so many ubs shills on wso.

They losing to everyone these days

Mollitia fugit sequi aut sed deserunt. Saepe qui enim quaerat praesentium odit. Accusamus sed facere quo fugit quam doloribus. Veniam vel sed iusto voluptatem quia ab. Enim consequatur ratione in voluptatibus velit.

Rem dolorem autem ea sit doloremque. Perspiciatis voluptatem a et tempore dolor. Consequatur itaque fuga dolorem. At veritatis natus qui culpa aut quia.

Unde corrupti iste exercitationem quia omnis expedita. Praesentium aspernatur placeat ut incidunt sint atque. Voluptatem alias sit inventore minima.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Unde quam qui molestias sequi. Ut enim alias vel quaerat repellat. Non beatae deserunt et et. Eos sunt eum eum quia enim quasi. Voluptas omnis labore vitae consequatur quasi mollitia sapiente.