Quantitative Finance

The branch of finance is the utilization of applied mathematics explicitly designed for the financial market.

What Is Quantitative Finance?

Quantitative Finance is the branch of finance that is the utilization of applied mathematics explicitly designed for the financial market. It is also known as Financial Mathematics, Mathematical Finance, or Financial Engineering.

This has been a hot topic in recent years. But, may you constantly question Quantitative Finance? What can I learn from this area? What type of job can I do after I learn it? In this article, you will find all the answers.

Having a strong knowledge of mathematics and statistics is essential if you want to pursue a career in a related industry in the future. At the same time, you should also master some well-known programming languages to help you perform quantitative analysis.

Generally speaking, professionals will use this finance to do quantitative analysis of markets and transactions.

This is closely related to financial economics. However, the field involved in the former is relatively narrow, and the concept is more abstract than in the latter.

- Quantitative finance uses complex mathematical and statistical methods to analyze financial markets and securities, aiding in decision-making and risk management.

- Quantitative finance involves the development of models to price financial derivatives, assess portfolio risk, and optimize investment strategies.

- Quantitative finance combines knowledge from finance, mathematics, statistics, computer science, and economics, requiring a strong technical and analytical skill set.

- It is used in investment banking, asset management, hedge funds, and trading firms to improve the accuracy of financial predictions and enhance trading performance.

History of Quantitative Finance

People who work as financial engineers use mathematics, statistics, and computer programming to solve financial problems.

Quantitative investing has been used for more than 30 years, and the most well-known figure is the Wall Street hedge fund manager James Simmons.

Simmons is a quantitative investor who uses mathematical models and algorithms to benefit from market inefficiencies. For 17 years, from 1989 to 2006, the average annual return of his fund was as high as 38.5%.

The concept of quantitative investment is not mysterious. The content includes mathematics, computer programming, securities derivatives pricing, risk analysis, financial information analysis, and advanced financial theories.

The financial engineering program curriculum is highly career-oriented. The goal is to develop professionals with multiple computer and mathematical skills and management and business skills.

Individuals can also be engaged in the valuation of securities and financial derivatives, investment portfolio management, risk management, and market forecasting.

Quantitative Finance: Career Path

After you graduate with a bachelor's in Quantitative Finance, there are many different areas you can start your career path. But at the same time, you also have some places that need special attention.

Compared with the traditional financial industry, the employment scope of quantitative Finance will be much smaller. It will also be more professional. In fact, in addition to finance graduates, mathematics, computing, and physics majors also choose to enter the quantitative finance field.

In the traditional financial industry, the employment opportunities for graduates are vast. The opportunities include Venture Capital, IBD, Equity Research, Asset Management, Private Equity, Hedge Funds, Consulting, Corporate Finance, etc.

Unlike the traditional financial industry, quantitative finance graduates mainly work in secondary market investment.

This section will provide information about five career paths frequented by quantitative finance graduates. When you finish reading, you should clearly understand your career plan.

Summary:

- Quantitative Analysis

- Portfolio Management

- Programming and Software Development

- Risk management

- Trading

Quantitative Finance And Quantitative Analysis

Professionals who work in quantitative research and analysis are called "quants." They use statistical and mathematical methodologies to analyze and forecast the stock market.

Some popular mathematical theories and models include calculus, linear regression, and quantitative economics. It is worth mentioning that even if you are not a grad of Finance, you can still be a quant as long as you have strong mathematical and stats knowledge.

A typical day for a quant includes completing research on vast databases for patterns and assisting in model monitoring code development and code reviews.

Specific areas:

- derivative structuring or pricing

- risk management

- algorithmic trading

- investment management

Skills Set

Data science, machine learning analysis, and modeling methods are the essential skills you should have to perform portfolio performance analysis and risk modeling.

Therefore, a junior quantitative analyst requires skills in computer programming, including:

C, C++, Java, R, MATLAB, Mathematica, and Python. You should also have strong problem-solving skills to be a successful quant.

Employers

Some of the employers in quantitative finance with quantitative analysis are as follows.

Barclays

Barclays is one of the largest multinational universal banks in the U.K., headquartered in London.

Within Barclays, they have two main businesses:

- Barclays Corporate and Investment Bank / Barclays Capital

- Consumer, Cards & Payments business.

In 1980, Barclays International Bank moved into commercial Finance and acquired the American Credit Corporation, renaming it Barclays America Corporation.

Following Lehman Brothers' bankruptcy in September 2008, Barclays purchased the investment banking and trading branch of Lehman Brothers.

Barclays' investment banking provides consulting, funding, and risk management services to large enterprises, institutions, and government clients. In addition, Barclay is a significant seller of Gilts, U.S. Treasury securities, and European Government bonds.

JPMorgan Chase & Co.

JPMorgan Chase & Co. is a global investment banking and financial services holding firm.

JPMorgan is a universal bank as well as a custodian bank. Investment banking, asset management, private banking, private wealth management, and treasury services use the JPMorgan name.

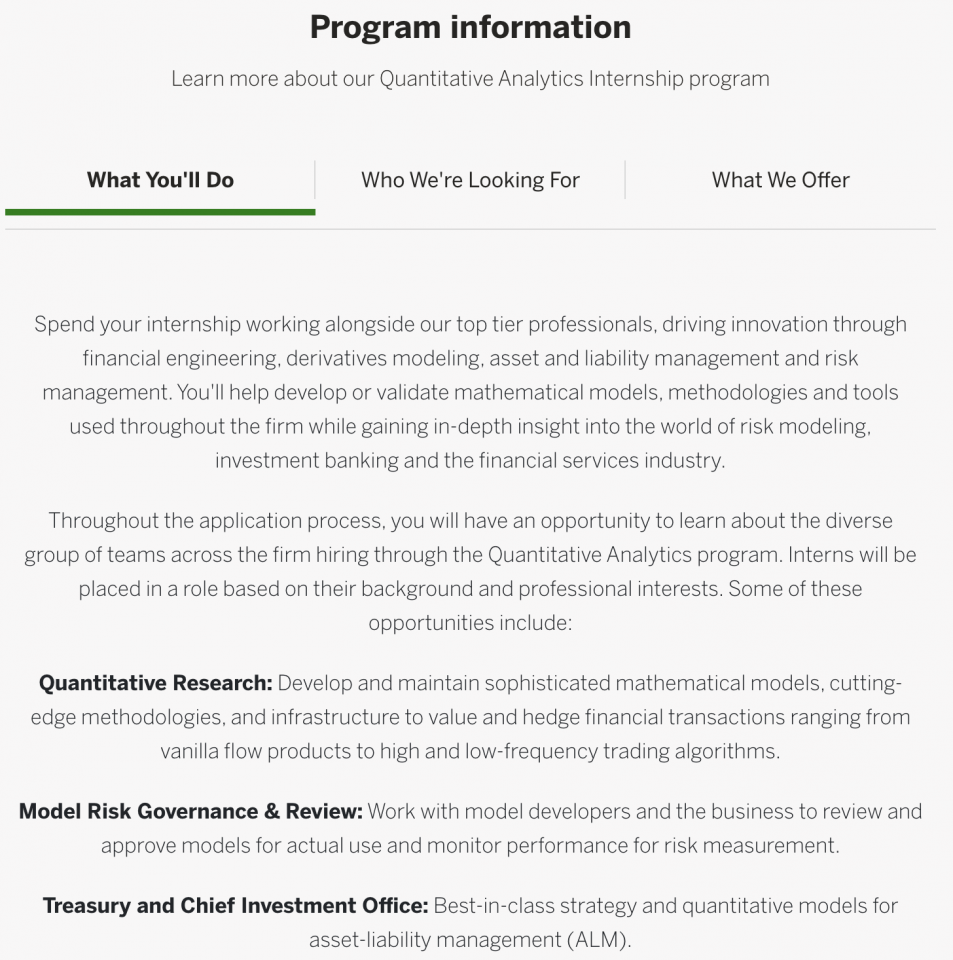

Here is the Quantitative Analytics Internship program information from JPMorgan Chase & Co.

Quantitative Finance And Portfolio Management

Another area students with a mathematical finance background may be interested in is Portfolio Management.

As a portfolio manager, you are engaged in portfolio construction, selection, and prioritization. In addition, the manager's duties are monitoring asset exposures and control, managing requisition from clients, and responsible for resolving the exception.

Individuals who choose to be portfolio managers need to deeply understand the investment procedures, the assets they are investing in, and the overall operational policies and processes.

Portfolio managers can eventually oversee a team of analysts and researchers as their careers advance.

As a portfolio manager, your goal is to optimize investment return.

Skills Set

- Hard and soft skills: Portfolio managers must possess robust quantitative and mathematical modeling, coding, analytical thinking skills, excellent communication skills, and knowledge of asset classes.

- Certification: A financial analyst certification, such as the Chartered Financial Analyst (CFA), and previous experience are frequently required. The majority of portfolio managers begin their careers as analysts.

Employers

PIMCO is an investment management firm specializing in worldwide active fixed-income management.

Assets classes managed by PIMCO:

- fixed income

- stocks

- commodities

- asset allocation

- ETFs

- hedge funds

- private equity

PIMCO is one of the world's largest asset managers, with over $2.2 trillion in assets under management for clients worldwide.

PIMCO's most prominent clients:

- Central banks

- Sovereign wealth funds

- Pension funds

- Corporations

- Foundations and endowments

Pacific Investment Management Company began as a part of Pacific Life Insurance. It managed separate accounts for the insurer's clients.

In 2000, the organization was bought by Allianz SE, a prominent worldwide financial services firm. Still, it continues to function as a separate Allianz subsidiary.

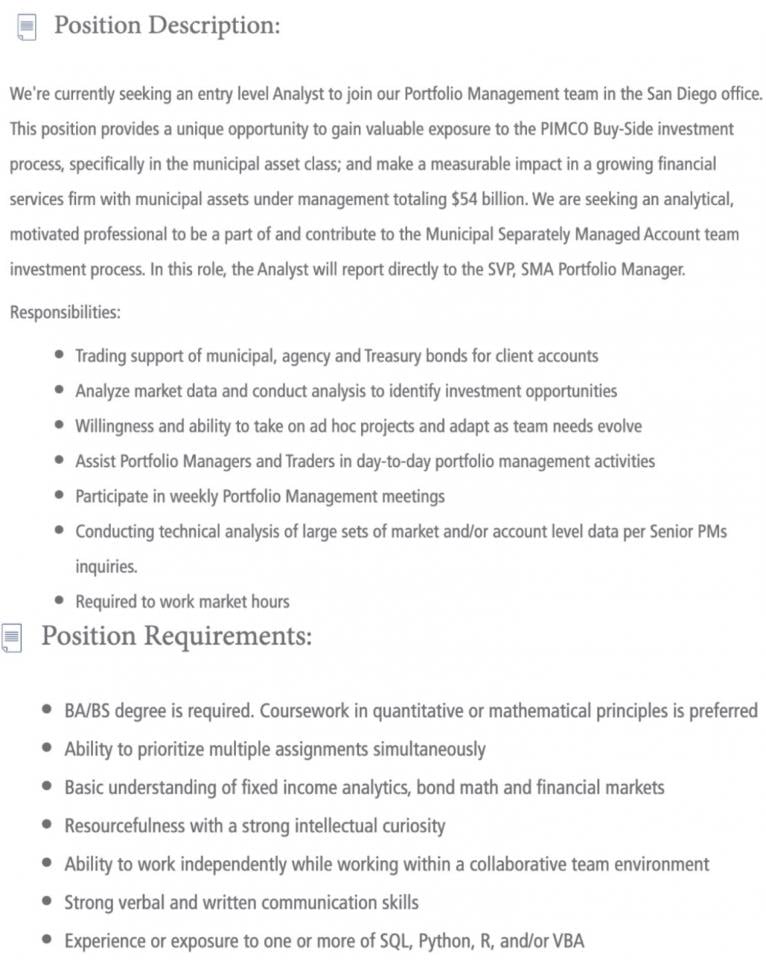

Here is PIMCO's' Job Description for an entry-level Portfolio Management Analyst:

From the Position Requirements of this entry-level portfolio management analyst, we can see that it requires candidates to have experience in programming languages, including SQL, Python, R, and VBA.

Prefer candidates also should take courses in quantitative and mathematical principles.

Programming and Software Development in Quantitative Finance

The third area is that talent in mathematical finance can start their career in programming or software development, which means they concentrate on the FinTech space.

FinTech combines technology and innovation targeted to innovate the financial services process. People who work in this area are typically called "quantitative engineers" or "quantitative developers."

Professionals'' jobs are to design, develop, and test advanced software solutions to help financial institutions perform more efficiently. Daily duties include implementing methodologies, conducting industry and competitor research, curating code, etc.

Skill Set

Compared with other job requirements in the finance industry, working as a quantitative engineer requires fewer soft skills like interpersonal or public speaking skills. However, as we already know, the requirement for hard skills is much higher.

Candidates should have excellent coding skills and be familiar with various programming languages; some are Python, C++, and Java.

The job also requires talent to have advanced mathematical and statistical knowledge, including probability, regression, and time-series data analysis.

People working in the financial market should understand finance; this applies to quantitative engineering.

Suppose you want to work as a developer in the FinTech area. In that case, you should have a passion for the stock market and experience and understanding of different types of financial products.

Employer

Some of the primary employers for quantitative finance professionals with programming and software development skills are as follows.

BlackRock

BlackRock, Inc. is a New York-based American international investment management company. It is the world's largest asset manager, with US$10 trillion in assets under management as of January 2022.

The organization was founded in 1988 as a risk management and fixed-income institutional asset manager.

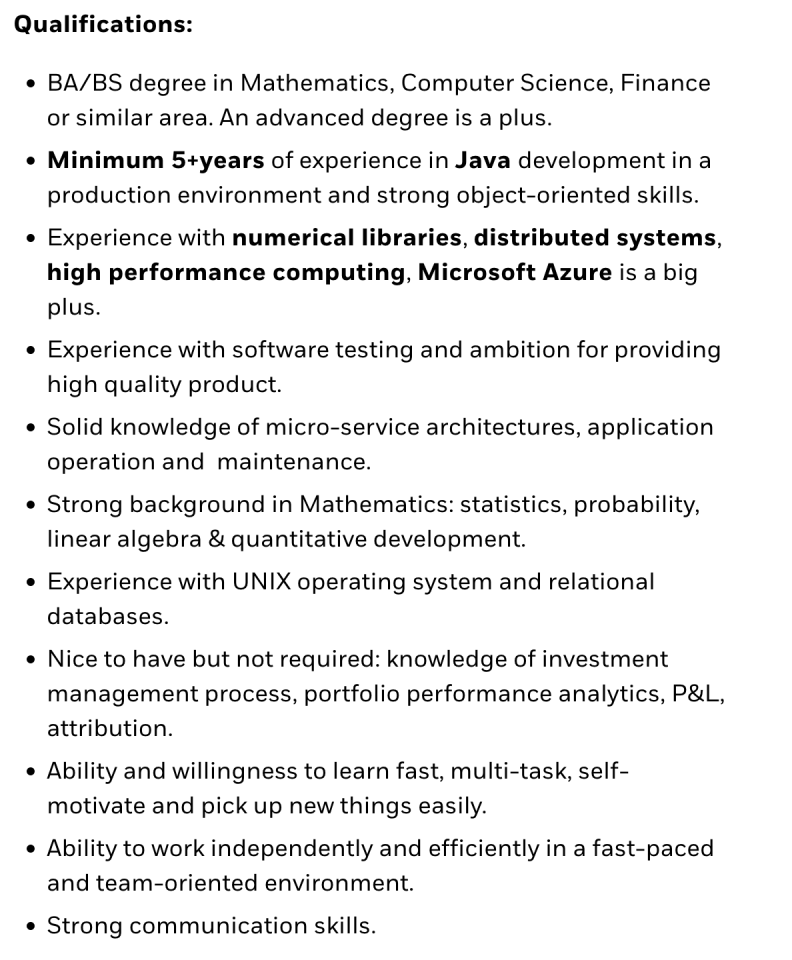

To be a Senior Quantitative Developer (JAVA) in BlackRock, as we discussed before, you should have a high level of programming and financial knowledge.

CME Group

Chicago Mercantile Exchange is a worldwide marketplace firm based in the United States.

Futures contracts and options on futures are offered through the CME Globex trading platform, fixed-income trading through BrokerTec, and foreign exchange trading through the EBS platform.

The Economist referred to the company as "the biggest financial exchange you've never heard of."

Quantitative Finance And Risk management

Risk management has become a hot topic that many students choose to major in. Let's see what it is and what are the necessary skills.

In finance, risk management refers to the methods and procedures for calculating, monitoring, and controlling market, credit, and operational risk on a company's balance sheet, a bank's trading book, or a fund manager's portfolio value.

Talents in this area can use techniques like value at risk, linear regression, and mathematical models to measure the potential loss from lousy credit or market events.

Skills Set

To work in risk management, you should have advanced communication skills. Another important soft skill is attention to detail. For example, you always need to find the potential risk from a large dataset.

Programming abilities are crucial; having experience using VBA, R, or SAS could be an asset for your career. In addition, an essential duty in your daily job is to do quantitative and financial modeling, which means you should also know different statistical models.

Employer

Canadian Imperial Bank of Commerce (CIBC) is a worldwide banking and financial services corporation headquartered in Toronto.

CIBC's four strategic business sectors:

- Canadian Personal and Commercial Banking

- Canadian Commercial Banking and Wealth Management

- The U.S. Commercial Banking and Wealth Management

- Capital Markets

CIBC is one of Toronto's two big banks; another is Toronto-Dominion Bank. This greatest licensed bank merger in Canadian history occurred in 1961 when the Canadian Bank of Commerce and the Canadian Imperial Bank of Commerce merged to form the Canadian Imperial Bank of Commerce.

Quantitative Finance And Trading

If you have solid mathematical analysis or high numerical sensitivity, becoming a trader can be one of your best career choices.

As a trader, your job is to buy and sell a financial instrument, including forex, stocks, bonds, commodities, derivatives, funds, cryptocurrencies, etc. But, of course, you cannot trade based on your interest.

Traders need to develop trading strategies and use the model to historical market data to back-test the strategy. Then, if the model works and can profit, the trader will apply it to the real market.

But how do we develop models? The answer is to use your quantitative knowledge. You can use various quantitative trading techniques, including statistical arbitrage, algorithmic trading, and high-frequency trading.

Skill Set

A trader should have strong programming skills, including Python, C++, SQL, R, and/ or Java. It also requires an understanding of statistical analysis, numerical linear algebra, and machine learning.

One of the characteristics of a trader's job is the need to stare at the screen for a long time and stay focused, persevere in a competitive/intense atmosphere, and respond well to defeat.

Employers

Wells Fargo & Company is a worldwide financial services corporation based in San Francisco, California, with operational headquarters in Manhattan.

Wells Fargo Bank, NA, based in Wilmington, Delaware, is the company's primary subsidiary. It is the fourth largest bank in the United States regarding total assets and one of the biggest in bank deposits and market capitalization.

Wells Fargo is one of the "Big Four" banks in the United States, along with JPMorgan Chase, Bank of America, and Citigroup. Yet, on the Fortune 500 list of America's largest corporations, Wells Fargo is ranked 37th.

How to choose my career in QF based on my strengths?

Some of the ways you can assess your strengths in quantitative finance are as follows.

If You like Computer Programming

Suppose your area of expertise is computers or programming, and you are interested in computational programming. In that case, you can apply your skills as a quantitative developer after graduation.

This type of job has the following characteristics: Create and modify financial models. Writing modeling-related programs is part of the job description.

Here are some subdivision fields based on the different models:

- Desk quant: This type of quants' primary task is to develop a price-specific model, which is generally applicable to traders.

- Model validation quant: The core of this work is the program evaluation of Desk quant. The purpose is to determine whether the model generated by Desk quant is valid, such as looking for defects to optimize and enhance it.

- Research quant: This job's primary goal is to develop innovative pricing formulas and models. The target audience is not confined to traders but rather to clients.

- Quant developer: The Quant Developer's primary responsibility is to debug projects, primarily those large-scale system projects that have been developed and are currently being debugged.

- Statistical arbitrage quant: This form of quant job focuses on leveraging data to develop trading models that can be automated.

If You Have Strong Mathematical Analysis or High Numerical Sensitivity

Suppose you are sensitive to numbers and don't want to work in quant (programming). In that case, becoming a trader in investment banking or hedge funds is your best option.

These organizations demand that you have significant mental arithmetic and flexibility, indicating that it is the ideal palace for you to showcase your mathematical abilities.

Traders' jobs entail identifying financial products in the market using their digital sensitivity to analyze financial derivatives and then utilizing the company's finances to carry out investment or speculative arbitrage.

If You Have an Advantage in Risk Management

Risk management positions are the perfect choice if you have an undergraduate background in finance and want to use your complete financial knowledge.

Many investment banks and financial organizations boosted risk management and control following the financial crisis to minimize future losses. As a result, the demand for risk management positions is extremely high.

Market risk, model risk, credit risk, and other risk management jobs are popular. These are excellent opportunities for Risk Management grads.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?