2026 Q1: GS, JPM, MS, EVR Shine, UBS Falls as M&A Roars back

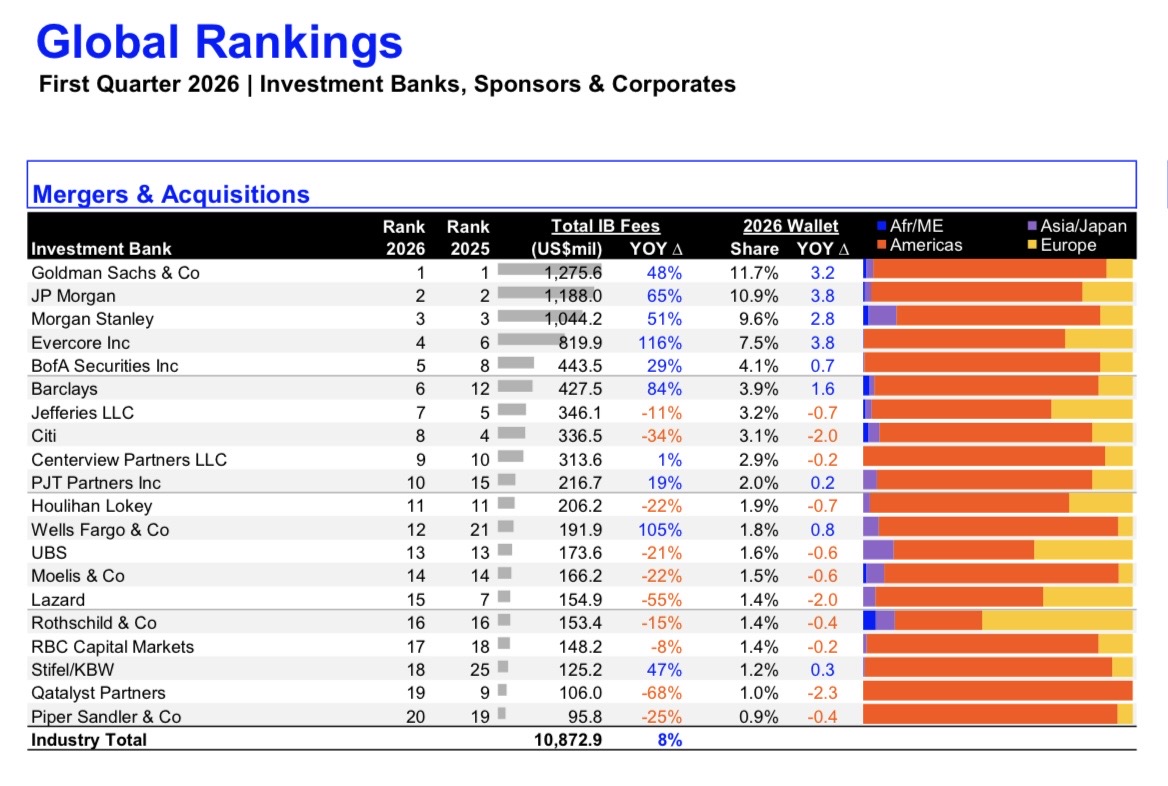

The M&A market has clearly turned a corner in 2026, with industry fees up ~8% and activity snapping back across sponsors and corporates. Goldman Sachs is once again at the center of it, leading the league tables with ~$1.3B in fees and ~12% wallet share, while JPMorgan and Morgan Stanley are right behind, all posting strong double-digit growth and capturing the bulk of high-value mandates.

The rebound is also amplifying the strength of elite boutiques. Evercore (+116%), Centerview Partners, and PJT Partners continue to gain share, reinforcing a broader trend: in a complex M&A environment, clients are leaning toward trusted senior advice, not just balance sheet.

But while the leaders and boutiques are accelerating, the middle of the pack is exposing clear winners and losers—and UBS is firmly in the latter camp. Sitting at #13 with just ~$174M in fees, down ~21% YoY and holding only ~1.6% wallet share, UBS is notably absent from a recovery it should be benefiting from. Post-integration, the expectation was that scale and expanded coverage would translate into advisory momentum. Instead, the firm appears stuck in transition—struggling to consistently win lead roles, retain top dealmakers, and present a cohesive M&A franchise to clients.

In a market where peers are posting 50%+ growth and market leaders are taking share with focused execution, UBS’s decline stands out less as a cyclical issue and more as an execution gap. The platform has the pieces, but they are not yet translating into results.

Further down the table, some of the declines look more like timing than structural issues. Lazard (-55%) and Qatalyst Partners (-68%) stand out on a YoY basis, but both firms are historically more dependent on episodic, large-cap or tech-driven mandates. Their positioning means results can swing meaningfully quarter-to-quarter depending on deal closings, suggesting the current drop is less about lost relevance and more about pipeline timing.

The broader takeaway is simple: the M&A recovery is real, but it is highly concentrated. The firms with clarity of strategy and strong client pull are widening the gap, while those still integrating, restructuring, or recalibrating are falling further behind—and in this cycle, that gap is becoming increasingly hard to close.

Can’t forget Wells. Has more global M&A than UBS despite almost all of it being in the US

Wells Fargo is paradise

Hilarious that Barclays has 2x UBS’s M&A after offloading all their flunky MDs to UBS

Bro Evercore double BofA is crazy

Evercore about to make it to elite M&A status as a Big 4 with GS, JPM and MS

with 10% of the people

Where did you get this data?

Looks like LSEG data

Wells is a BB confirmed

Citi got on all the huge deals but looks like they didn't really get much fees for them compared to the rest

Which means they aren’t actually “on” most of the deals. Just getting adds for lending / financing rather than actual advisory.

Congrats on UBS!

Lazard is so cooked

.

WF is the next big thing confirmed

This is crazy. I assume Evercore (M&A only) is probably like half the size of MS or JPM? Yet they are generating ~70-80% of their fees

Evercore has more bankers than Morgan Stanley.

Still crazy that they're doing that level of business without a balance sheet but Evercore is really not the same as the other EBs given their sheer size.

lol EVR is the same size as LAZ and not sure where you got the data for MS having less bankers vs EVR... EVR has 1.6K bankers globally (not just M&A), pretty sure MS has much more lol

On what earth Evercore has more bankers compared to MS, bud? Even if you take only the US (where Evercore predominantly operates), MS has like 2x more bankers, if not more

LAZ is atrocious. They have the same scale or size as EVR (+better international reach given their EU presence) yet they generate like 1/5 of EVR's fees. Talk about underperformance

How is Lazard FIG?

Or we can go, we can go up up up up!

Stifel > Qatalyst confirmed

Based on the table looks like Stifel has more US M&A than UBS

UBS sucking is old news but man… Lazard really fell off. They are not in the same galaxy as the other EBs anymore

LAZ sucks as ususal, what a joke

What are they feeding the guys at Evercore man, damn...

Listen, UBS is a shitshow, but it’s clearly engagement bait to specifically call them out when their ranking was unchanged and Lazard and Moelis also fell off. Not to mention the only people who actually care about 1 quarter of M&A are not in the industry.

Look at this UBS clown, always full of excuses

When I first started at UBS they were 5th, that’s why a goal of 6th was originally reasonable on the (now laughable) press tour they did claiming that

Citi is surpisingly low. Thought Vis had hired a load of rainmakers from JPM.

Comfortably 4th on the deal values ranking so assume they have just focused resources on getting deal credit for the largest deals?

This Senior VP in IB - Cov clearly works at Citi and has been trying to hype up the bank for a while now across multiple threads. Just need to come to terms with the fact that Citi is and always will be a balance sheet bank that clients call on for lending rather than true strategic M&A advisory. Sure it's got some traction in tech and healthcare, but it just can't compete with the likes of Evercore, Centerview or the Top 3 BBs

Citi, BofA, and recently Wells fall firmly into the “2nd tier” of BBs who get the occasional pure M&A cred but are mainly used for financing. Not a terrible place to be given the entire IB landscape, but the top 3 BBs are on on another level

Congrats on MS/JPM

Top 3 BBs lmao.. Dude, nowadays it is pretty much GS, EVR, and CVP as the top M&A players. JPM mostly gets credit to maintain financing relationship, even on deals they are "exclusive advisors". And MS has fallen off a lot over the past couple of years - It used to go toe to toe with GS, but now they are clearly no. 2/3 BB

Eius fugiat labore dolore. Hic cum animi reiciendis molestias ut sed nihil. Alias ab doloremque quaerat odit officiis. Voluptas aut quis quasi aspernatur nam. Tempore nihil veniam est nobis. Ipsum libero dolorem aliquam ipsam harum. Temporibus eos reiciendis saepe reprehenderit.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Optio omnis omnis id eos. Amet voluptates nobis impedit. Nostrum et soluta maiores soluta est tempora. Nesciunt recusandae temporibus atque sunt sit fuga.

Beatae totam et et quae necessitatibus odit. Facere eum accusamus a perferendis commodi. Accusantium alias dolor rem laudantium aliquid officia.