Help on DCF analysis WACC and Perpetuity Growth Rate

To clarify: I'm not so much concerned with the inputs I used as I am generally with how WACC is used in the industry. Do you use a predetermined discount rate or calculate WACC in a different manner than I have etc.?

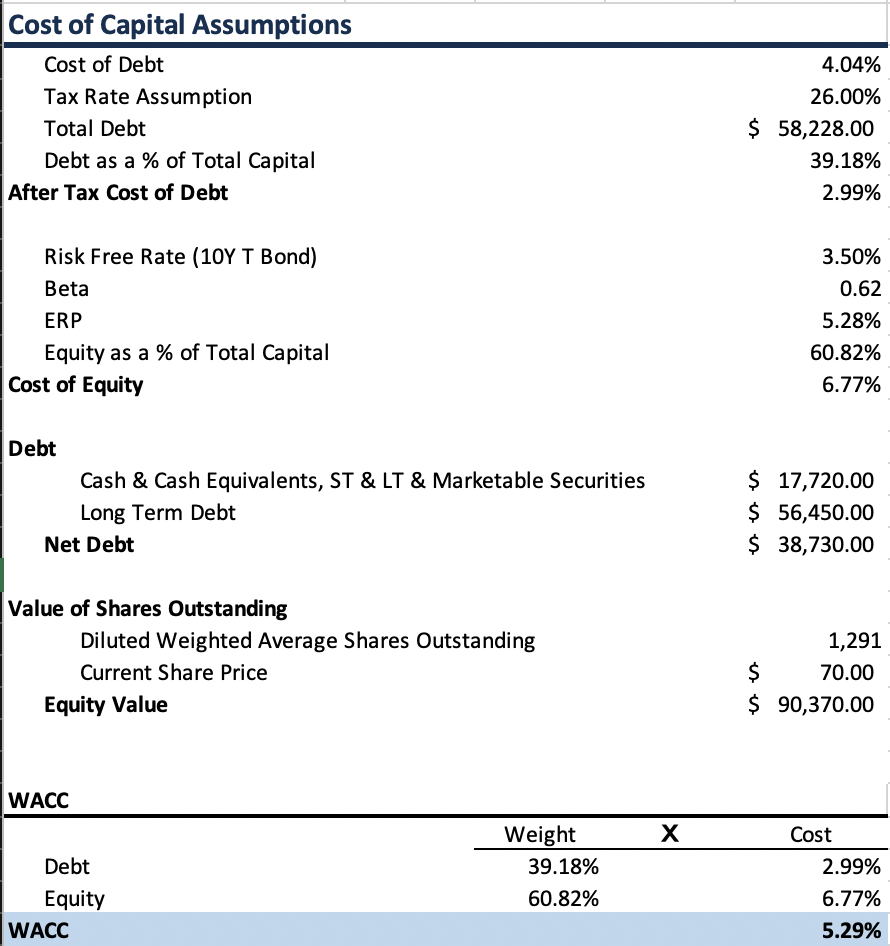

I'm working on a DCF for a stock and had a couple of questions regarding WACC and the perpetuity growth rate. I calculated WACC as shown below using information from the company and it seems to be unreasonably low. I'm a sophomore in college so I have zero experience with this. I was wondering what some best practices were for deciding on the WACC to use in a model. Should I use an industry average or some other measure other than calculating it as I did? I would essentially need a perpetuity growth rate of zero for the model to make any logical sense even if I rounded up to 6% (since the valuation at 5.29% is a bit insane). What are some common ways of handling this? I really appreciate any responses.

And instead of doing work your off to a forum..gen z will just be hand off enough for millennials to kill off the planet with AI

I have no idea what this is supposed to mean. Instead of doing what work? I'm learning financial modeling entirely on my own time and thought I'd use the resource of industry professionals that is WSO to ask a question since I sadly failed to emerge from the womb with a complete grasp of financial markets.

Do you have any insights that would be helpful to my question?

I'm in bed rn but here are some general thoughts(i'm a junior btw):

For a sophomore this is a great starting point and good on you for doing this

1. Since 2018 the corporate tax rate has been 21% so if I'm lazy I use 21% or I look at 10k for "effective tax rate"

2. ERP I use Aswath Damodaran's market risk premium

3. I would also look up unlevering and relevering your beta (in case the beta you're using is from yahoo finance)

4. For a sanity check I will look at comps to see if the WACCs (and capital structure) are similar

5. When I use perpetuity(which is rarely) I keep rate near historical inflation levels

6. Lastly, I would recommend making a sensitivity table where your axes are your exit multiple and WACC testing your 'implied value'

Thanks! I used last years effective tax rate in the 10k and Damadoran. I calculated the weighted average interest rate on outstanding senior notes for the cost of debt. I'll look at comps. I'm fairly sure the inputs are all correct I was wondering if you've seen any different ways of treating WACC. I've seen some sites use the risk free rate plus the ERP and use that as the discount rate instead of calculating it from the company. I looked at the implied multiple as well. I can get an implied multiple thats inline with the 5 year average using a 6% WACC but it feels odd using a growth rate that is so low to do so.

Just saw that now. The calculation of the cost of debt is not what you would want to use. Think of it like that - you want the WACC to discount future cash flows, so all WACC inputs should also be forward-looking. What you do by taking IS/BS data for the interest rate is to implicitly assume that the past financing is indicative of the future. Now we all saw what happened to interest rates in the past months. Alone by the gap between cost of debt (4%) and rf rate (3.5%), you see that this looks odd.

Hierarchy of options for cost of debt calc:

(i) bond outstanding - take the yield

(ii) no bond outstanding - take the credit rating, look what that means for default probability and top up risk free rate

(iii) no bond and no credit rating - construct synthetic credit rating (simple approach by Damodaran - ND/EBITDA, complexer ones available as well)

Thanks so much this is incredibly helpful. Would it make sense to use an index like BofA BBB Us Corporates effective yield since the company is BBB rated? If not should I use the yield on the bonds with the longest maturity?

IRL we typically handspread WACC comps with CAPM based off unlevered beta, apply the median and recalculate according to the applicable company’s cap structure.

(Also IRL, your MD will just say “that looks low, let’s go with x.x%)

All the advice above is good. In reality, if the WACC is too low then it’s engineered higher by using a higher erp or adding a size premium if possible. And for the exit multiple, usually just comps but also whatever the MDs “gut” is and you back into reasoning for it..

The gearing in your assumptions at the top differs a lot from the valuation at the bottom (39% debt vs c. 29% in valuation below). You assume 58m of debt at the top and in reality it is only 38.7. You assume a target capital structure? Aare you going to maintain that high leverage in the forecast? Probably not, while your WACC will remain the same (which implies you maintain that gearing). I don't know about US cost of debt - is 4% up to date?

I have seen slightly higher ERP - see comment on Damodaran (https://pages.stern.nyu.edu/~adamodar)

With regards to terminal value: read about the value driver method: gordon growth formula lets you assume high RONICS into perpetuity while WACC is 6% (that would attract a lot of competition and reduce profitablity etc.).

Finally, think about your forecast. Are you only taking into account a bullish case? I like to make 2 or 3 scenarios that show the impact of the 2 major threats to the company and then take a chance-weighted average of those 2 - 3 outcomes.

Thanks so much for the help. For the cost of debt I used the total debt of $58B. Net debt was $38.7B. Are you saying I should have used the net debt figure in calculating cost of debt?

For the forecast I used the lowest analyst estimate for revenues in an effort to be conservative and same as last, a growth rate, or 5yr avg margin to get the other figures. I will definitely look more bearish/bullish cases.

All of the below is highly subjective:

In my opinion there is two ways to look at it gross/net debt discussion:

For a take-private situation I would use a target leverage that is sustainable. Opening leverage in my opinion is not sustainable, while WACC assumes that capital strucutre into perpetuity. Given that you assume EBITDA growth, the gearing will become lower anyway (EV up, debt stable at best in short run). Long story short: I would not go crazy on gearing, because it never remains that high in practice.

Impossible to say since its the ouyput only but first sight considerations:

(i) Cost of Debt at 4.04% is really only slightly above your risk-free rate, implying a AA if not AA+ rating. Thats rare among individual companies but obviously could be the case.

(ii) Beta seems very low. If its not a utilities company I wouldn't trust that at all. Whats your calculation based on?

Et quae aut iste nihil. Magni quae reprehenderit unde illum accusamus officiis. Expedita blanditiis possimus sapiente sit magnam ducimus explicabo modi. Molestias voluptatibus placeat repudiandae voluptatum laudantium aut eaque. Commodi et suscipit soluta rerum.

Exercitationem adipisci ipsum velit dicta dolores. Molestiae voluptatem laboriosam nobis nostrum enim.

Deserunt in omnis ipsam magni perferendis dicta. Libero nobis magnam sed facilis.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...