Software bankers how is deal flow?

What are you guys seeing in this market? Seems some of these businesses have existential risks today…

What are you guys seeing in this market? Seems some of these businesses have existential risks today…

| +186 | UBS Accused of Favoring H-1B Workers While Cutting U.S.-Born Employees | 45 | 3m |

| +79 | IB Energy Drink Tier List / Ranking | 54 | 7m |

| +76 | PJT M&A Group Selection 2026 | 13 | 8h |

| +42 | ONLY THESE BANKS OR YOU STRUCK OUT | 10 | 31m |

| +36 | Quick Thoughts on CVC AI Sale Process | 7 | 3d |

| +33 | Feedback for internship first desk at IBD BB - personal fit, "don't be too confident" | 23 | 23h |

| +28 | Does BofA still pay its associates rat pellets? | 13 | 58m |

| +19 | Updated JPM Group Rankings | 29 | 32m |

| +18 | What happened to Greenhill | 8 | 3d |

| +18 | VP Deal Origination Credit | 2 | 7h |

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

I just saw a post on linkedin about "rule of 60" is the new "rule of 40". If that becomes the new benchmark for SaaS, what you're going to have is businesses that are being bought only if they have hockey stick revenue and AI running operations.

But that means some businesses will be way better

Many deals now on pause, people don’t want to make decisions right now, pretty rough

PE or banking?

Both because ~70% of software deals are banks selling to PE firms (work in software group)

At a bulge bracket and credit standards being meaningfully tightened at the moment, which should be a read through as far as LBOs are concerned. Particularly anything even moderately under ai displacement threat, which is anyone’s guess.

At one of GS/MS; think some sponsors are more motivated to do deals than they were a few months ago (mostly the tech specalist firms and a value firm here or there giving software a second look) but most generalist sponsors have pretty much put tech investing on pause.

Think there's been a ton of talk around this on the forum; but generally some of these generalists that dabbled in tech investing might be wiped out (some funds are going to be sub-5% IRR) given how bad their previous tech investments are. There's a bunch of JAMMBO owned point solutions with no diffrenitation that are either never getting sold or getting sold for significantly less than what it was bought for. Some software specalists have some of those in the portcos, but generally JAMMBO's that dabble in tech have worse positioned portfolios IMO.

See some businesses doing very well and seeing acceleration in rev growth and margin acceleration, but even those are negatively effected by lower multiples in terms of finding a exit. Think as time goes on, software valuations are probably going to be split between high-quality businesses that every sponsor wants (thus maintaining high multiples in auctions) and the rest that nobody wants (really hard to value some of these point solutions that might go to zero in the next 4-5 years). As long as capital continues to be allocated to software only investors (Hg just announced they raised $30bn in very short order this Feb), there will be sponsor Tech PE deal flow.

Great write up. Do you think there’s going to be a problem with how many bankers cover software relative to the deal flow?

Unsure, am just a Tech An2 who is speaking from my internal infrastracture work and deals. Think for better or worse, my group is fairly insulated from a pure deal flow perspective just given brand name. We still have a lot of mandates and a lot of bake-offs are happening now. Just hard to know how many of these will close given the wide range of views on software among sponsors and strategics.

I think there will still be deals for some of the better assets in the market just because these PE sponsors have to invest the captail they raise, think bigger issue is the exits of the companies these firms bought before the rise of AI. Just my 2 cents is that I think 2026 will be a year of a lot of firms acquiring or investing growth rounds in AI disruptors by the more growth-y investors and also some take-privates of public names a PE firm might see some value in.

Replying to you here. I just started that valuation thread that you commented on. We traded some thoughts a couple days ago.

Yes I’d move out of SW banking to industrials / special project financing. I’m doing that but as PE investor.

On other thread, would appreciate if you could give some of the datapoints in response vs asking if I’d leave SW banking. I’m trying to get people data to answer that question. Think it could be very helpful if it gets momentum.

Seems no one replied to your other thread…

Yeah too bad… and got MS here lol. Oh well… no responses isn’t great data but we have the market for that. I think the bid-ask spread is massive given limited SW deals getting done.

Have you reached a conclusion on your career next steps / leaning more one way now? Curious.

SW seems tough. My general approach to banking is you don’t want to sell things people don’t want to buy. What do you make of all the software dry powder? That’s the one interesting thing. Wonder if they pivot to growth equity?

I think growth equity is in just as much trouble. The same trends are hitting them. On the dry powder… I think firms are going to wind down their software teams. I know of 1 firm already doing it… pushing non tech investors into the tech team before pushing them out as well so they can say “we unwound our team strategy” with more fake datapoints for LPs. A lot of ICs are guys that have been doing this for 30 years, made their money and doing really care about the next generation of leaders at their firm.

Another fun marketing narrative is firms shifting to focusing on “picks and shovels” of AI… really funny to think firms that were bad as asset light businesses being good at asset heavy businesses.

But HG won’t wind down right?!

If these trends persist and play out… can see the large pure play tech PE funds getting smaller… maybe winding down after enough time. Clipping fees is still a good biz model for managing partners as long as LPs still show up. I think the wind downs will be more dramatic for firms that have multiple verticals… not very hard to wind down a team and shift $ deployed to the other verticals.

No reason for Hg to wind down. As long as you deliver alpha relative to your peers, you will be fine in all of investing. These pension funds want exposure to all industries fundamentally, and you are evaluated relative to funds with similar level of industry exposure, same idea as in HF. Pensions will always want exposure to private software as an industry given it's % of the private markets.

What we are already seeing is that software specalists are succeeding in raising a ton of money, more than before, including Hg which just last month announced it already raised $30bn. The JAMMBO's (which from the comment history of the VP you are replying to, it's abundantly clear that's the type of fund he/she is at) of the world might exit software, but no real reason for specalists to exit.

Me: If these trends play out and persist I can see them [Hg and peers] getting smaller

You: JAMMBO guy (not btw lol) above doesn’t get pension funds. They WILL always want software exposure. Repeats my point on JAMMBOs winding down tech teams.

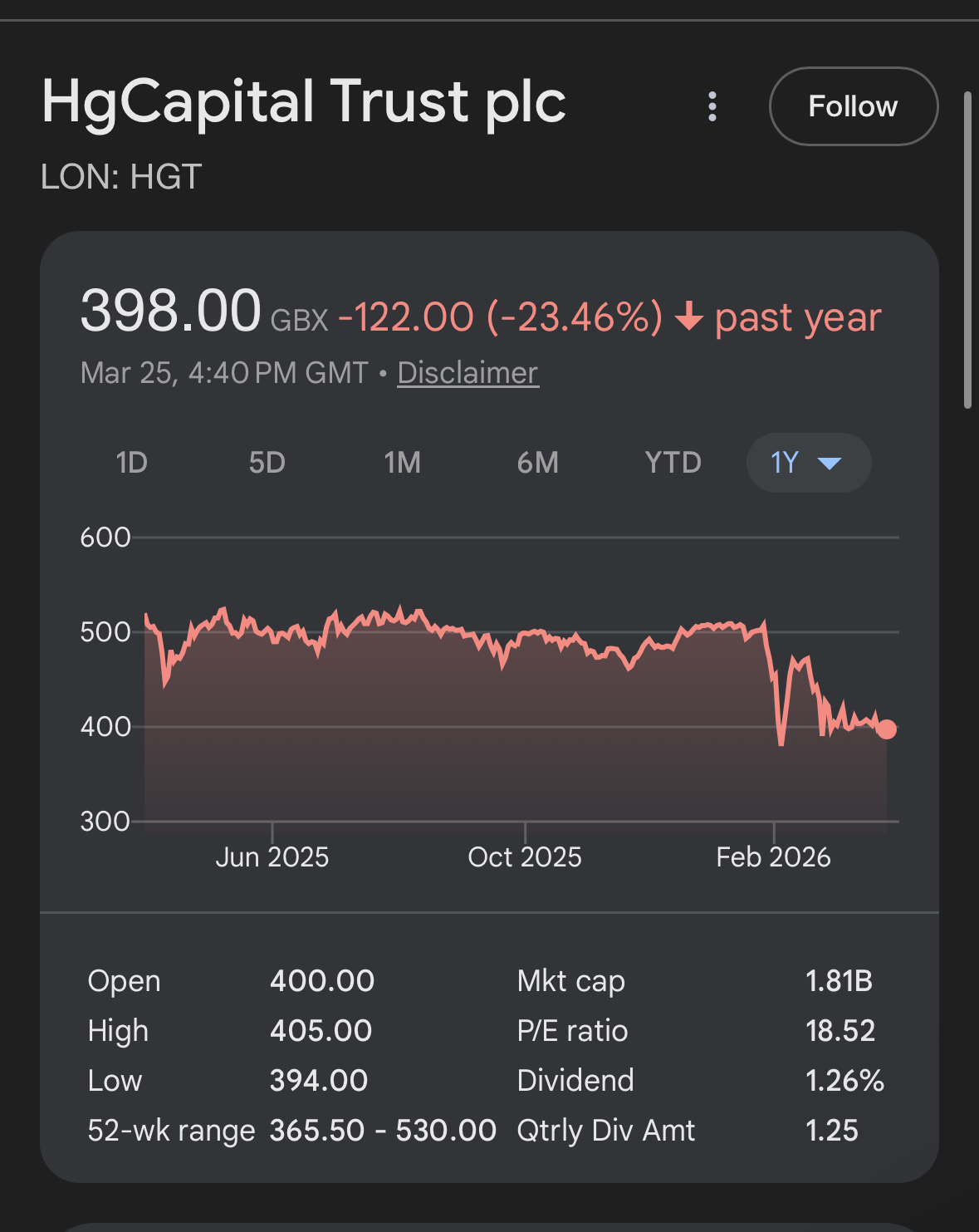

Are you sure pension funds won’t pull back on pure software GPs if trends persist like I said? You know Hg has public vehicles right? You think pension funds will keep supporting software if the below chart continues? Fundraising is a lagging indicator and LPs are slower to react to trends.

How much has O&G PE shrunk since the early 2010's? I don't have the stats, but look at the shadows (or carcasses) of sector focused GPs that were leftover from that period

None because as long as you deliver alpha relative to your peers, you will be fine in all of investing. These pension funds want exposure to all industries fundamentally, and you are evaluated relative to funds with similar level of industry exposure, same idea as in HF. Pensions will always want exposure to private O&G as an industry given it's % of the private markets.

Except O&G is not as privately held as software, and therefore you can get more exposure to the sector through the public markets. O&G also had a sustained downturn from a macro perspective, software as a % of American GDP is growing still (important to remember most AI applications are effectively sold as software), albiet at slower rates than before. Fundamentally, pensions want to diversify and hold the broader economy. I think you misunderstand what LP's are looking for. If performance was all that mattered, HF's as an asset class would be long out of business.

Just another horrific take. Please stop commenting on my posts. You consistently say things that are wrong or so obvious that they derail the discussion.

You originally pushed back on tech funds / teams decreasing in size… now you are enlightening me on AI effectively being a software model… it’s actually fundamentally different unit economics which are driven by compute usage but sure… subscription plans are how it’s being packaged now to drive adoption and are heavily subsidized. Not going to last forever or go way up to better match costs. What’s AI?

Also… which you’d have noticed if you ever researched anything… the LPs are getting AI exposure by going direct. They don’t need a GP to invest in OAI or Anthropic. You’re grasping for stuff / throwing shit at the wall but actually further proving my point without realizing it.

Remind me which frontier model or any leading AI company is owned by a PE fund that gets money from LPs?

I’m way closer to LP mindset than you. You can’t over simplify what LPs want to “fundamentally own the broader economy.” That’s dumbed down to level where you might be trolling. Do you mean they want GDP level growth? No, they fundamentally want to generate enough returns to meet their liabilities… going to argue that next?

Look at the chart I posted. That’s software PE right now and likely the next ~5 to 10 years. Hg is sharp but this disruption is hitting everyone. Downside of going public… reporting.

LPs invest in hedge funds to… as hedges within their publics portfolio. It’s in the name.

S&P performance has been driven by MAG7 but yeah totally more of a need to get software exposure via privates…

What’s your take on covering AI companies at a bank?

Not positive either. I think AI (and software going fwd) will be a very consolidated industry from banking client prospective / few winners. Think we’ll have a lot of small disrupters that pop up, make some cash and then are in turn disrupted.

The line to cover the big names will be out the door with very few B / C tier clients for the Director levels to win to make MD. This is mainly through M&A lens but the winners are so big that I think they are only going public once.

Pray to god that kid doesn’t comment for these next parts but… I think it’s just going to be very difficult to bank those names and limited M&A.

It’s fundamentally different business model / product than we’ve seen before. Why buy a competitor when you can replicate their capabilities with your product or an LLM? Way smaller scale but I basically use this logic when I add skills to my openclaw… I don’t download a skill, I just build it “myself” to avoid malicious code. Have to imagine real engineering teams can do to this at way bigger scale. Kinda see it with the frontier models mirroring each other on UX / tools. It’s not pure convergent evolution IMO.

For frontier models why hire / pay full fee to a banker if your product can handle all of the grunt work and you already have a massive investor base / insane demand for your equity?

I’d also be weary on covering “AI” companies. I think real chance you end up getting stuck mainly with disrupted software business that want the AI label during a sell-side. Every software biz is trying that line.

For my hottest take… I actually think local models win long-term (I’m like 70/30 on this right now). Those are free or can be effectively created through distillation. They just make too much sense for consumer… customizable, no per token cost, some really good free ones already. They basically lag frontier by 6 months and require local RAM but doable and only getting better too. Google’s TurboQuant will be a gamechanger when available (basically algo improvement type advancement — more power on less compute).

Another factor and I’m not complaining is AI researchers / builders seem to opensouce their products a lot more.

I can see banking “data” companies as a good idea but just too horizontal and those will be covered by respective industry bankers. Realizing my post is only focused on AI software. I’m a lot more positive on AI hardware companies.

What about vertical software (ie industrials)? I would think those businesses are safe? I agree over the next 1-2 years I don’t see how LBOs happen when private credit is bragging. Also, one stream deal did get done so there is debt for some software…

Are you referencing the Paramount deal? That’s a big one but a unicorn-type deal, just like the EA one IMO. Gonna get some debt at $110b EV with huge equity cushion. Just different.

Can you expand on why you think industrials vertical software would be more insulated? Any specific names? I don’t really see the angle.

There are a few historically nice targets that I can think of like Prometheus. Traded in ~mid 2024 but that’s ancient history given how fast AI risk / functionality has grown. I’m over simplifying but would think any biz like that which sits on top of SAP has much greater risk of SAP building it themselves > lower value, harder to trade. Same thing with some of the O&G (or other) worker tracking / safety quals bizs. Definitely better than some end-markets with faster innovation cycles but still hard to see strong deal flow in near term.

Would look into insurance SW (better data moats) or other heavily regulated end markets.

New to the thread but what about your thoughts on Govtech software?

Interested in your take given I've spent some time around industrial software. Btw I think he's referring to Onestream's $6.4B acquisition by Hg - there was good demand for the debt.

Yes, Prometheus was a prominent industrial software deal. More recently TPG carved out Kepware / Thingworx and Proficy from PTC and GE, respectively, combining them into 1 industrial software company focused on connectivity and MES.

I think this is an interesting space that is probably more defensible against AI than white collar focused software. This is a slow moving industry and the cost of being wrong is severe (people getting injured on the factory floor) so I think it's relatively shielded, at least for now.

I think the SAP argument is wrong, as they've had decades to build a viable competitor (and already have competitive modules) yet some of these businesses in categories like MES, SCADA, EAM, etc (that are close integration partners w/ SAP) continue to do well.

Ah yeah…. That makes sense. Open to pushback. I think we need to differentiate bookings being OKish for now vs. investors making money on deals. You can get comfortable with almost any books trends but riskier terminal value can really slow deals.

SAP has had decades and are notorious slow. I looked at a couple of these so naturally this was one of the biggest risks if not the biggest. SAPs innovation cycle only got faster with AI + can help them progress through HANA migrations faster.

They are slower moving industries with sales cycles of like 12-24 months so recent bookings probably OKish but “next buyer” risks are huge right now.

Yes bad things can happen in heavy industry but I don’t think it’s often software causes or stops accidents. Workforces and projects scale up and down so managing / onboarding a qualified workforce is a core value add a lot of the time. I’m cynical generally but I’ve never seen a CIM that didn’t say this product is mission critical or something similar.

Reiterating that software teams eventually have to deploy. Debt teams are verticalized too.

Buried the lead but…. can we agree SAP should be one of the most defensible, entrenched and mission critical names? It’s down 30% YTD. Gets to the second part of my first point and term value risk… that should scare off some buyers for awhile.

im incoming A1 in a software group, should i look to pivot to hardware?

Do you agree industrial software will be safe (autodesk, hexagon etc). I think they will be okay and command a premium but curious if it’s baby thrown out with bath water.

Excepturi ut optio ipsam in quisquam nemo. Aliquid ea repudiandae ipsum sint id facere sint. Veritatis quos numquam mollitia ratione tempora quis labore assumenda. Ut et quas dolores rem.

Reprehenderit quae non placeat ut pariatur. Maxime atque repellendus rerum enim ratione voluptates sunt.

Id nobis illo vel perspiciatis. Et molestiae deleniti ipsam quaerat et nobis. Facere quas dolor in qui et corrupti. Et eligendi officiis est et. Quas aut et asperiores velit amet ut officia harum. Asperiores et repellendus natus. Doloribus omnis qui cum occaecati vel blanditiis ipsa.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Suscipit placeat a dolor dolorem. Inventore maiores consequatur enim enim. Dolorum consectetur excepturi est est aliquid omnis voluptatem.

Vel vitae voluptate in quaerat laborum enim maxime molestias. Et alias et enim voluptatem et nisi qui. Adipisci pariatur soluta sunt officia qui ut. Sed dolores atque et libero incidunt molestiae exercitationem.

Maxime vel vitae et quia. Fuga esse sit omnis repudiandae omnis. Qui nostrum laboriosam in sunt explicabo totam accusantium. Voluptatibus velit corrupti eum est cupiditate architecto consequuntur.