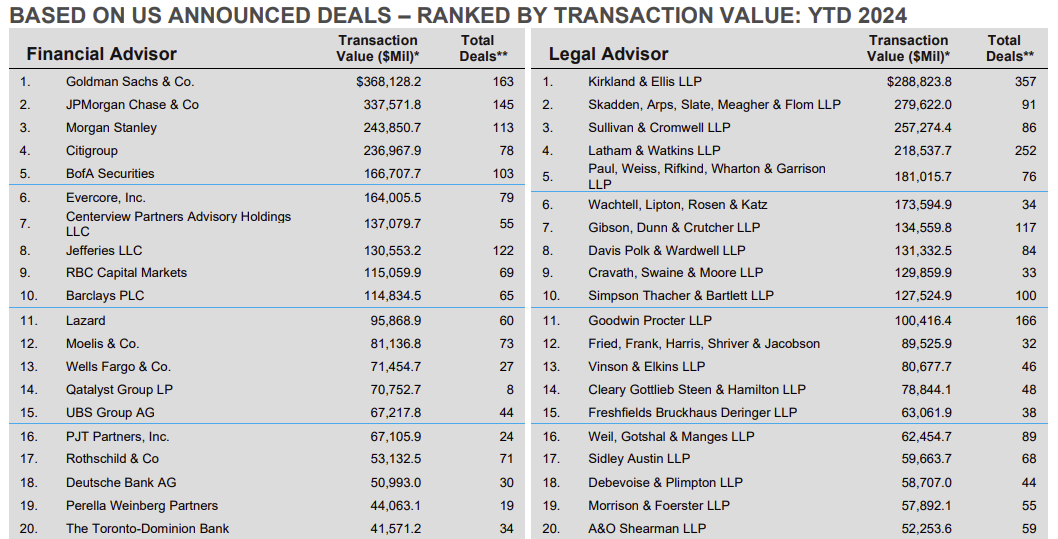

UBS to Divest IB? Now #15 in US M&A, losing 45% of Global IB fees in market share since 2022 (UBS + CS) in YTD 2024

Didn't UBS say they wanted to be #6? Looks like underperforming on a path to divest the IB

- Global IB Revenue market share was 4.0% in 2022 (#5), 2.6% in 2023, 2.7% YTD 2023 (#7) and now 2.3% YTD 2024 (#10) (https://wsjapp.dealogic.com/scorecard)

- They are performing at about 40% of the goal #6 in the US by 2024YTD transaction volume as of September 2024

Not that crazy of an idea

Probably too hard to separate

Has been rumored before… If they don’t perform it’s probably more likely

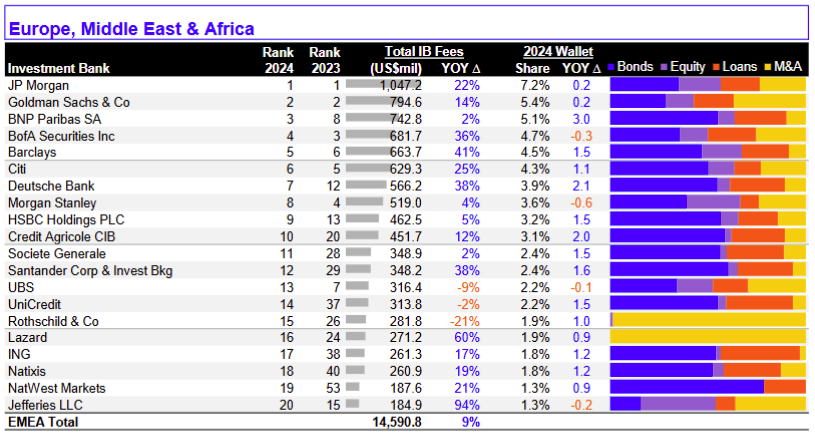

EMEA is doing pretty good

Subtraction by addition

They took what would of been the proforma #6 bank in europe for M&A in Q4 2021 and made it the #10 bank in Europe for M&A Q2 2024

https://www.olshanlaw.com/assets/htmldocuments/FactSet%20Flashwire%20Ad…

https://go.factset.com/hubfs/mergerstat_em/quarterly/AdvisorQuarterly.p…

APAC is crushing it!

APAC doing GrEaT #9 and down 20% this year! THE SOURCE (lseg.com)

EMEA doing GrEaT #13 and down only 9% this year! THE SOURCE (lseg.com)

Americas doing GrEaT #14 and down only 3% this year! The only bank in the top 20 this year with less fees this year than last year! Tied with Barclays for the most market share loss YOY (0.5%) THE SOURCE (lseg.com)

Global Investment Banking | LSEG

No doing historically bad

No dog in this, but I do wonder if the drama and integration last year prevented them from winning some of these mega-deals that were longer-term burns... The needle movers can be years in the making, they had so much chaos last year that I doubt anyone was awarding them big mandates. They are publicly talking up their IB pipeline lately, but they'll have to put their money where their mouth is.

I guess we'll see in 2025 and 2026 if that's true or not. Could definitely see them becoming a wealth shop if this continues.

Using the 80 / 20 rule

Top 20% of CS bankers responsible for 80% of the CS revenue left in 2023 as the bank collapsed

Top 20% of UBS bankers responsible for 80% of the UBS revenue were pushed out as Barclays consolidated power across almost all groups

Self selected Barclays bankers who didn't have a bright future there / didn't get promoted (mid to lower bucket) left for UBS

End result is UBS is about the same as it was pre-integration performance / revenue wise with 30% more cost.

This narrative is basically right

Business is overall performing OK, you guys are a bit much

It’s not this bad?

They had more revenue dis-synergies than cost synergies, lost 45 percent of all combined IB revenue not just M&A.

No major wins since Kroger Albertsons in 2022 (CS), which could easily still be blocked.

https://www.albertsonscompanies.com/newsroom/press-releases/news-detail…

laughing hard at this thread

its true the merger when looked at a pro forma basis, the revenue in US IB is pathetic. worse than pre merger

and the kroger deal is 1000% getting blocked. especially with kamala likely winning in november.

frankly, you cannot be a top 10 bank

would be hilarious if sergio divested the US IB after all this posturing by the new leadership brought in from barclays

like how does two large BB swiss bank combine and still be behind RBC in the league tables....

It's interesting how little LevFin leads or success has impacted UBS M&A activity especially as UBS has seemingly gotten significantly more aggressive on the LevFin side. The coverage and M&A folks are simply not pulling their weight. However, the one thing to note is that the M&A deals being done now are mostly mandates won in 2023... where nobody in their right mind would have given UBS or CS a mandate given all the chaos happening. Based on public statements from the CEO and Marco Valla, they seemingly have a strong 2025 and 2026 pipeline, we will see how true that is within the next year or so. It's impossible to judge till then. A few of UBS's top guys, CS's top guys, and a few Barclays good MDs are still there, it's very much a bits and pieces kind of deal but probably still somewhat stronger than pre-acquisition even if it's just purely due to UBS being more aggressive in terms of winning LevFin lead mandates (the one thing the Investment Bank in the US is geuninly actually good at).

You are being brainwashed, UBS+CS in 2022 have also lost market share relative to 1H 2024 in just syndicated loans

UBS now # 14 (2.1% Share) in Global Syndicated Loan Fees for 1H 2024 (Global Investment Banking | LSEG_)

In 2022, Credit Suisse was #10 (2.6% Share) and UBS was unranked

Dude look at the Lead Left rankings for below BB-rated credit (what is typically considered LevFin across the street)... UBS is top 5. Syndicated loan rankings aren't a reflection of LevFin strength just pure balance sheet lending. There's a reason WF is 6th in here but not t10 in terms of leads, they never actually lead processes and are always on the right of these deals. Don't speak about products you are unfamiliar with.

Why PRECISELY is it the case that no one in their right mind gave UBS a mandate in 2023? Is it just a signalling/perception issue? Or was there an objective real (set of) reason(s) why it would be disadvantageous for clients to use UBS?

I believe it’s the threat of restructuring and layoffs. From the outside looking in as a client, you don’t know if your banker will still be there in a years time. I think many clients still see this as a risk given three way merger and Sergio’s historical lackluster embrace of the IB. There’s also been 3 IB global heads in last 2-3 years which points to continuous churn and instability.

.

.

Evercore killing it too

Do league tables even matter?

For sure, you don't want to sit there aimlessly marketing

Not sure how well the merger is going or how long Sergio will be patient

Wonder what the best team is, hard to tell

Avoid, Avoid Avoid!

Surprisingly very close poll results

Not shocking at all, UBS has a lot of juniors who rightfully hate their job(very clear favoritism in a lot of groups, less deal flow than promised in most group, wide difference in analyst experience across groups, a lot of layoffs including juniors, etc.). This site is also full of a lot of MM firms analyst that see themselves as above UBS/DB, and want to push that narrative. Therefore, you get results like this. Make no mistake, UBS has absolutely underperformed but also to be perfectly fair 2024 deals are mostly 2023 mandates when nobody in their right mind would give a mandate to UBS given the whole instability and merger thing. It doesn't really make sense to give a mandate to UBS then b/c you don't even know who your banker will be given all the layoffs across all levels. Until UBS goes a few months at least without major MD layoffs, this should continue to be the case, it'll be very difficult to get people to trust your bank to be M&A advisor for them when the client doesn't even know if the MD they gave the mandate to will even be there for long.

In 2025 the story will be who in their right mind would give UBS M&A if they didn’t have M&A in 2024, because they had changes in 2023. Please give us until 2026.

The cycle will continue in perpetuity as long as Marco is there.

They still number 7 globally. USA will grow steadily after 2026 when integration is completed

Really drinking the koolaid from that info session

They #10 in 2024

With IB expected to have about $2bn in earnings would have a $12bn to $16bn valuation (P/E = 6 to 8).

Possible acquirers that could easily afford: HSBC, RBC, BNP, Truist, BMO, Macquarie, Scotiabank, Santander

would be hilarious if sergio sold UBS IB americas to Truist or something. lmao

Trust buying and then firing all legacy Barclays MDs would be an all time full circle moment

They are just mid and perfectly happy to be mid. Happy to accept deals other firms don't have capacity to work.

Probably

Initial 3rd quarter league tables show they are in trouble

No, there is not a single chance that UBS will become a wealth management-only platform. IB will always be there as a dead weight. Years before the merger, Sergio was hired to restructure UBS, and his strategies included trimming the fat in IB and upsizing wealth management. After that, Ralph became the CEO, and there were no major layoffs in IB for about four years(you can’t cut it to the bones), but then the merger ruined everything

Now they are #17, they had $1bn in M&A in one month…

Imagine having several hundred MDs do ~$1bn in M&A combined in a month… Run (don’t walk) away!

M&A is lumpy but doesn’t sound good

Rio Tinto - Arcadium was a $6.7Bn cross-border deal (Tinto is Australian and Arcadium is American) that included the US and was announced in the past month. Not sure what site you are using for aggregation, but UBS was cited as an financial advisor on that deal and it should be counted as an America deal.

Congrats on the nice chunky deal. This deal was announced in October. Previous statement referenced Sepetmber 1 to October 1 announcements. October looking 4x better than September with 1 deal

Seems more likely everyday

2024 numbers were not good, bank head could be replaced

They must be starting to question the whole deeper entry into the Americas strategy. There could be an about face as they see how crowded the Americas is

Asian focused banks such as Mizuho, HSBC, and Nomura could be good fits

Seems relevant

Voluptate ab aut officia rerum sed. Et qui rerum totam velit laudantium voluptatum enim. Excepturi neque laboriosam voluptas laborum explicabo quod. Corporis consequatur voluptatem ad tempora dolore quae esse.

Consequatur molestiae architecto quia. Libero beatae amet repellendus. Vel amet quo aliquam earum labore eius. Nostrum sed consequatur esse ut. Rerum est asperiores provident ex rerum nemo et. Commodi minima unde voluptatibus sed sint quos.

Porro incidunt assumenda sed fuga sed veniam eaque. Quibusdam harum deserunt error accusantium sapiente repellendus. Debitis enim est cum.

Vitae natus minima eveniet non. Et qui modi quibusdam. Molestias sapiente ullam consectetur est eos nesciunt. Quo similique eligendi quod aperiam fuga in. Excepturi aliquid dolor unde et natus officia qui et. Provident alias temporibus sint vitae quis.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Repudiandae et delectus mollitia voluptate eum voluptatem. Qui harum labore voluptates ea temporibus exercitationem. Sint et dolore asperiores inventore.

Ea odio minus sed ea voluptatem. Doloribus assumenda quaerat dolor et. Est quas eveniet voluptatem totam. Rem nobis odit repellendus laboriosam perspiciatis.

Fugiat expedita sapiente molestiae non alias dolores id vel. A est vel debitis repellendus numquam inventore. Nobis quidem tempore quo minus eos omnis quae. Dolorem nulla et voluptas et possimus placeat cum.

Nulla et molestiae consequatur aut placeat qui minus. Placeat culpa qui aut odit.