The Real Large-cap Corporate PE Placement by Bank

Something seemed a bit off while going over the recent thread on MF PE placement based on bank and school, so I decided to do one based on more stringent criteria. I excluded schools because it was pretty obvious most of theses funds were filled predominantly by Wharton and the usual targets.

Method

This list only includes Associates at large-cap corporate PEs in North America across the whole region (NYC, SF, Boston, Chicago, and Austin) with recent fund sizes of $15B+ and historically considered MF PEs, namely Advent, Oaktree, Bain Cap, KKR, Blackstone, Warburg, Vista Equity, CVC, EQT, Cinven, Apollo, TPG, Thoma Bravo, Silver Lake, Carlyle, H&F, and CD&R. Also, the list only reflects Associates who directly exited from the respective banks. For example, if an Associate A worked at Barclays then lateralled to MS, then the placement was credited to MS.

Previous and many placement lists are misleading because those lists include all the Associate titles in non-corporate buy out roles, such as capital markets, special situations investing, credit, secondaries, client solutions, growth investing, real estate, etc. Therefore, I only included associates who are part of the corporate buyout team at their funds or the funds have no investing team other than their corporate buyout team. Any unidentifiable associates were omitted for all banks.

I highly doubt such omission will lead to a biased information gathering, as it is unlikely the sample characteristics between who chose to disclose being part of corporate PE role and non-corporate PE roles across the listed banks will be meaningfully different. Simply, the percentage of associates who do not disclose them being part of the corporate PE team will likely be similar across all firms. Not to discount those roles (personally find non-corporate PE investing more attractive nowadays), but seems like the best interest of this forum is about corporate PE placement which is arguably the most competitive investing role.

Interesting Observations

For EBs

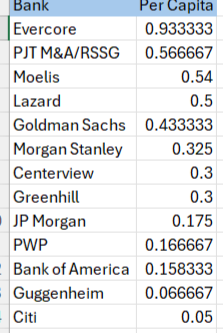

- Considering the analyst class size of around 60 at Evercore, their placement at these so-called MF PEs seemed to be leaps and bounds above any other banks. Evercore seems to be the only bank that sends analysts from completely non-target like UC schools to MF PEs.

- PJT M&A and RSSG share similar exits in contrast to this forum's perception that RSSG is a tier above the M&A group in terms of exits. Likely due to selection bias, it was observable that many RSSG analysts exited to special situations investing (both public and private roles) which was not included in this list. Similarly, HL RX had many special situations exit which is also not included in this list.

- Guggenheim shows more than expected exits to these funds.

- Lazard likely had better exits in the 2010s, as there were some numbers of principals/managing directors at these funds. Quite underwhelming exits recently.

- Greenhill mostly exits to UMM and credit/special situations roles.

- Associates from Moelis had the least pedigreed degrees, but their exits were solid.

- Note that the estimated class sizes are around 60 for Evercore and Guggenheim, 50 for Moelis, 20-30 for PWP, CVP, Lazard and PJT, 10 for Greenhill. This reflects the class sizes 3-4 years ago not the current sizes.

For BBs

- JPM, Citi, and Barclays had surprisingly weak exits, while BofA seems to be a bank with better than perceived exits.

- For JPM, the vast majority of the associates came from the M&A group, with one or two from Healthcare and Media groups.

- For BofA, the vast majority of the associates came from the M&A group with few from FSG.

- For MS, the vast majority of the associates came from the M&A group followed by Tech, and few from Media and HC.

- For GS, it was quite evenly distributed among TMT, Industrials, and Healthcare, while two or three exits were from FIG and Consumer.

- Expecting around 90~120 class sizes for the mentioned BBs.

Conclusion

The sheer numbers may be marginally off, but if the exits were ranked like this, I highly doubt this will change, as the same method was applied to all the firms. Also, CVP and PWP exits are quite challenging to gauge due to the large numbers of A2As, but I highly doubt they will be discounted by any funds compared to other top banks, especially CVP.

Since today is a slow day, I decided to update and include the per capita information. Aligning with the perception of this website, Greenhill still has great exits considering the class size, while the Guggenheim number looks quite grim. Furthermore, although Lazard is not perceived as it was in the past, their exits still look better than most of the places. If one's goal is to truly land at one of the largest PE firms, it is plausible that the only realistic route is to lateral to GS/MS/JPM/BofA and EBs.

Why does this have oaktree, tpg, bain cap if it's for 15bn+ corporate pe funds?

My bad, forgot to mentioned I also included names generally considered MFPEs. Honestly could not take out those names as those funds still seem to be more desired than $15B funds like New Mountain.

nwc is more desirable than oaktree but not tpg or bain cap.

Moelis analyst class for the last few years is ~40

Edit: Moelis NY analyst class is ~40, Moelis LA is around 7-10.

believe it's more if including satellite offices (LA esp)

LA is 9, SF is 11. Moelis also has Chicago, Boston, and Houston offices so the number checks out

Assuming Moelis recently expanded their class size from SVB absorption and Trauber crew joining the Houston office, current PE associates should be assumed from the analyst class size of 50ish prior to expansion.

Can we not do this?

Much better/accurate list than previous, however would consider adding in MF SS funds. Not including an Apollo HVF but including a bain cap PE seems a bit redundant. Likely skewing PJT numbers downwards (although already top 2 per capita)

Fair point considering how competitive it is to get those SS/HV seats. However, such inclusion will make BB exits look unnecessarily worse compared to EBs with RX practices, as SS/HV seats are realistically only available to RX analysts to my knowledge. It's not that BB analysts lack certain aptitude to do SS/HV but they simply don't have the exposure needed to be successful in those seats. Of course it could be argued that BB analysts lacked technical aptitude to get offers from EBs, but they simply might not have been interested in RX in the first place. I wanted to keep this list apples to apples. Still, I agree that PJT exits are negatively skewed, as SS/HV seats are equally if not more competitive to get than the traditional buyout seats. I think we can all agree that Evercore and PJT are in leagues of their own in terms of exits regardless.

League on their own, agree

so "PE associate" counts any of associate year 1 and associate year 2s ?

So evercore, with a class 60 analyst class size, has 56 PE associates, meaning 120 analysts (2 x 60 analyst classes -- that is, over 2 years) have produced 56 PE associates?

PE associates include senior associates as well. Honestly, Evercore placement is rather downwardly skewed, as I left SS/HV exits likely from the RX group. Evercore both by sheer number and per capita has the most MF PE exits.

The EVR class size is also much bigger than 60 these days, more like 100+ including regional offices

This is based on their class size 2-3 years ago

Greenhill Mizuho better exits than JPM💀

Someone with a specific brand of autism should do some work to give each exit seat a value rating from 1-10 relative value units (RVUs) and then produce a list of banks ranked by total RVUs per capita, and also do it for schools. I mean, no one should do that, but if we’re going to do this that’s how it should be done, but it shouldn’t

I like that. Then I think the second analysis is based on composition of the analyst class ie school create a composite expected value for a group and then seeing if the placement from each group exceeded that EV to see if there’s a benefit to be from a certain group or those groups just hire all Wharton / Harvard etc

See that’s why you’re a senior vp

would assume this also skews towards analysts who self-reported their group (e.g being part of JPM HC vs. JPM diversified industries) on linkedin?

This is my very subjective opinion based on what I've heard in the bullpen and from my alma kids, but I really think it's self selection for BBs. I've never heard or aware of any JPM weaker group analysts not getting interviews at places that they wanted if they prepped reasonably well. I I think it's not that JPM non-top groups are discriminated but kids who are there just lack enough preparation. Anecdotally, two kids who got offers at EB RX and M&A negotiated their offers with guaranteed MS M&A and JPM M&A placements, which they just skipped the whole group placement process. This may not be the norm but sure you can see who lands at top groups at GS or MS.

i meant in terms of this posts linkedin analysis — not actual placement. know not every banker puts their group as part of their description

bump

Blanditiis repellat et at vel ex et. Fugiat voluptate harum saepe illo consequatur quia. Veniam sit sequi id odit. Nihil eos facilis ut cum sit.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Repellat magni veritatis commodi eum laudantium et earum. Labore autem dolores praesentium fugit at ut. Architecto labore atque aut. Repellat illo mollitia consequatur. Pariatur vel et voluptate consequatur sed dolorem est.

In cum quis saepe perferendis tempora temporibus at. Nulla fugit aut ea animi quibusdam.