[Early 2026] The Definitive and Data-Driven Healthcare IB Group Rankings (Biopharma + Broader HC)

[WSO limits posts to 5,000 characters, so I’m including the methodology/rationale as pictures and the subjective biopharma tiers with commentary in a comment below.]

Why I made this

When I was recruiting, I didn’t have a built-in pipeline to Wall Street. My school wasn’t one of the places that sends dozens of kids into banking each year with dedicated clubs, formal mentorship, and career-center counseling geared toward IB recruiting.

There weren’t enough people around me that I could reliably learn “what’s actually true” from peers a year or two ahead. So like a lot of students in that situation, the main resource I leaned on was the internet, and specifically WallStreetOasis.

And while WSO can be incredibly helpful, it can also be misleading. A lot of rankings are thrown together based on brand name, vibes, or whatever dumb thing people are arguing about. Many are created by 1st or 2nd year analysts who don’t have enough distance to separate short-term noise from real platform strength. And sometimes people are biased for reasons unrelated to reality: a group didn’t interview them, didn’t take them, didn’t give them a return offer, or they had a bad experience with a specific team, which can turn into “rooting against” a platform for years.

In biotech, the last couple weeks of the year (Christmas through early January) are usually the least busy weeks. Nobody wants to launch financings around holidays/JPM, and deal flow slows down. I had a couple days free and wanted to pay it forward by building the guide I wish I had: a transparent, mostly objective ranking framework grounded in actual biopharma M&A and ECM activity, not random opinions.

TBH I’m not a big fan of “rankings,” but we all know rankings are the easiest way for students to digest information quickly. So if we’re going to rank groups, we might as well do it in a way that’s fair, transparent, and grounded in real M&A and ECM activity, not just who has the loudest fan club online or the sharpest axe to grind.

This is meant to be a living resource and am open to serious feedback

Despite the title, I’m not claiming this is perfect or that it should be taken as gospel. But I’m trying to lay it out clearly enough that (1) you can see exactly what I’m doing and (2) we can all improve it over time. I want this to be a living guide that gets updated over time – as I plan to update this based on feedback received in this thread and on a yearly basis around summer analyst recruiting season to help students/juniors make an informed decision.

Feel free to DM me if you have any thoughts. I also might set up an email so that credible people can send thoughtful feedback anonymously (especially for the broader healthcare list, where I’m less confident).

And just to be clear: My goal is that students can use this as a real resource, and not get misled by the typical forum rankings that are often biased and often based on flawed thinking, as I definitely wish I had a resource like this when I was recruiting many years ago.

Core concept: why I didn’t just rely on league tables

Most forum rankings are basically “who shows up highest on the league tables by aggregate deal volume.” That’s how you end up with misleading outcomes.

Example: in 2023, MTS was credited as a co-advisor on Pfizer’s $43B acquisition of Seagen. Per filings, they were brought on later and were not paid on the deal while Centerview got a massive payday. Centerview was really leading the deal. But MTS still got co-advisory credit on a $43B transaction, which can push them near the top of league tables by aggregate M&A value, and that doesn’t tell the full story.

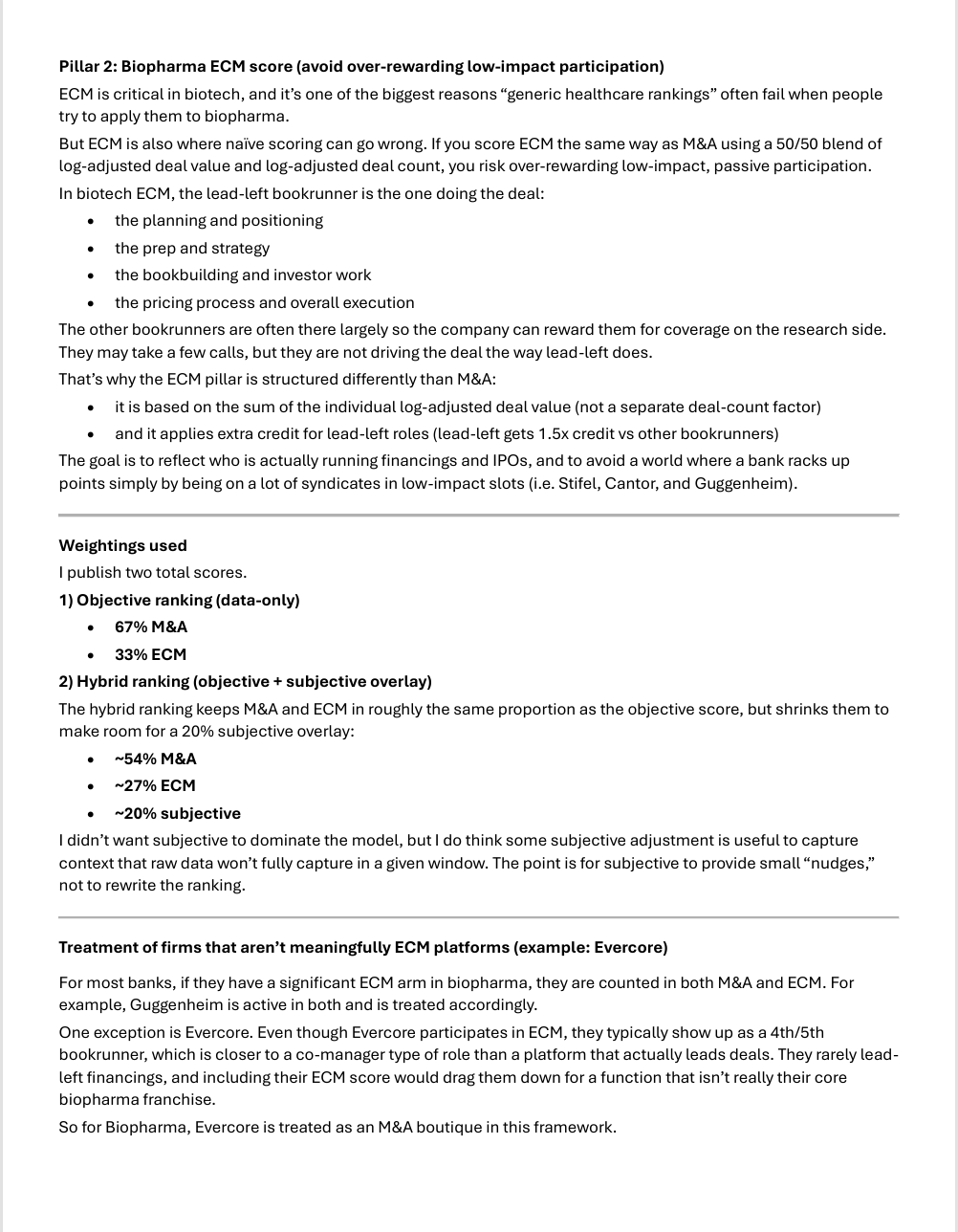

That’s why I built the scoring method this way: to reduce the influence of massive outliers, and reflect both (a) consistency/flow and (b) meaningful deal size, instead of letting one mega deal hijack perception. Also, many “league table” rankings are heavily M&A-focused and don’t properly capture ECM, which is a huge part of biotech banking and a major differentiator in biopharma.

Methodology

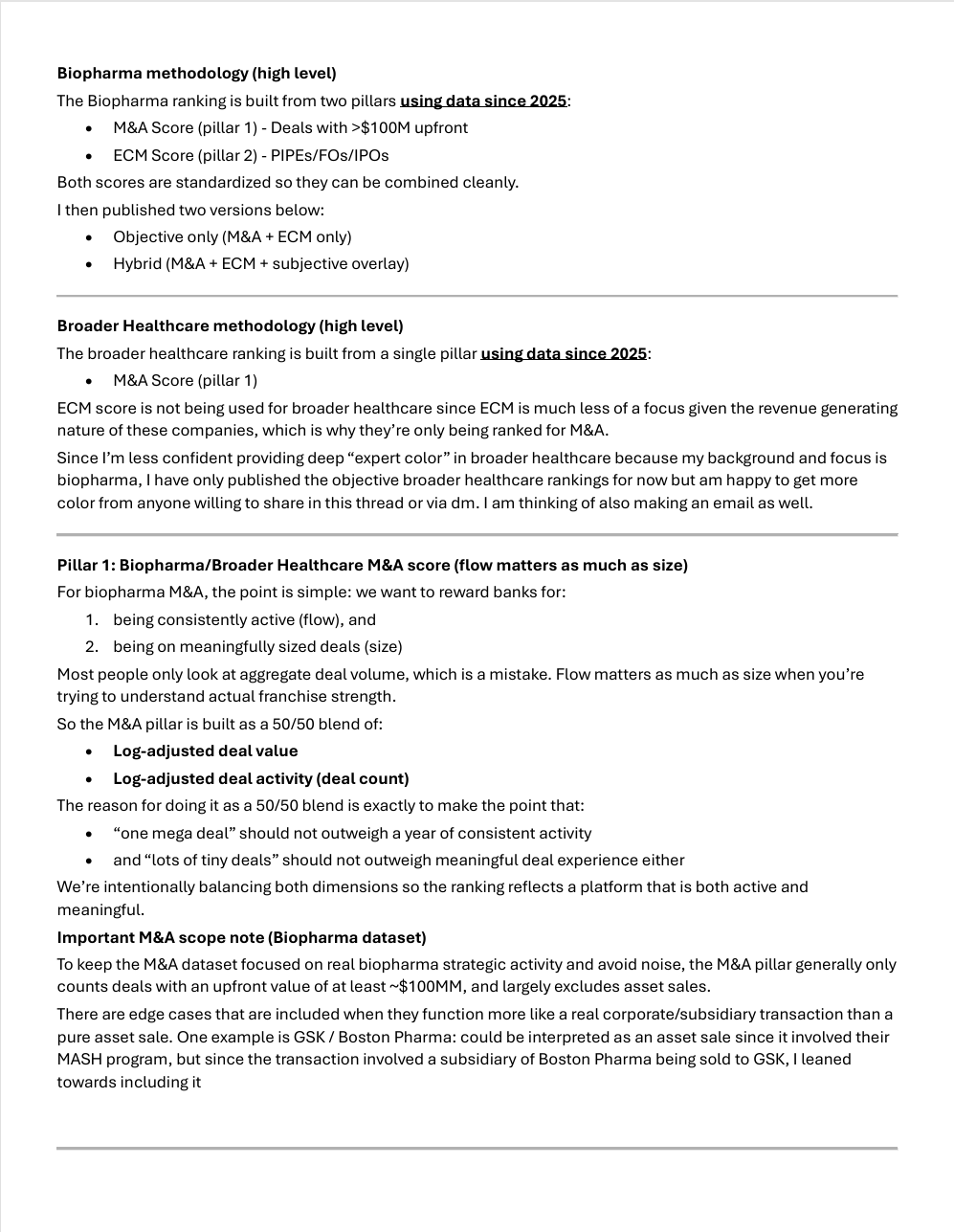

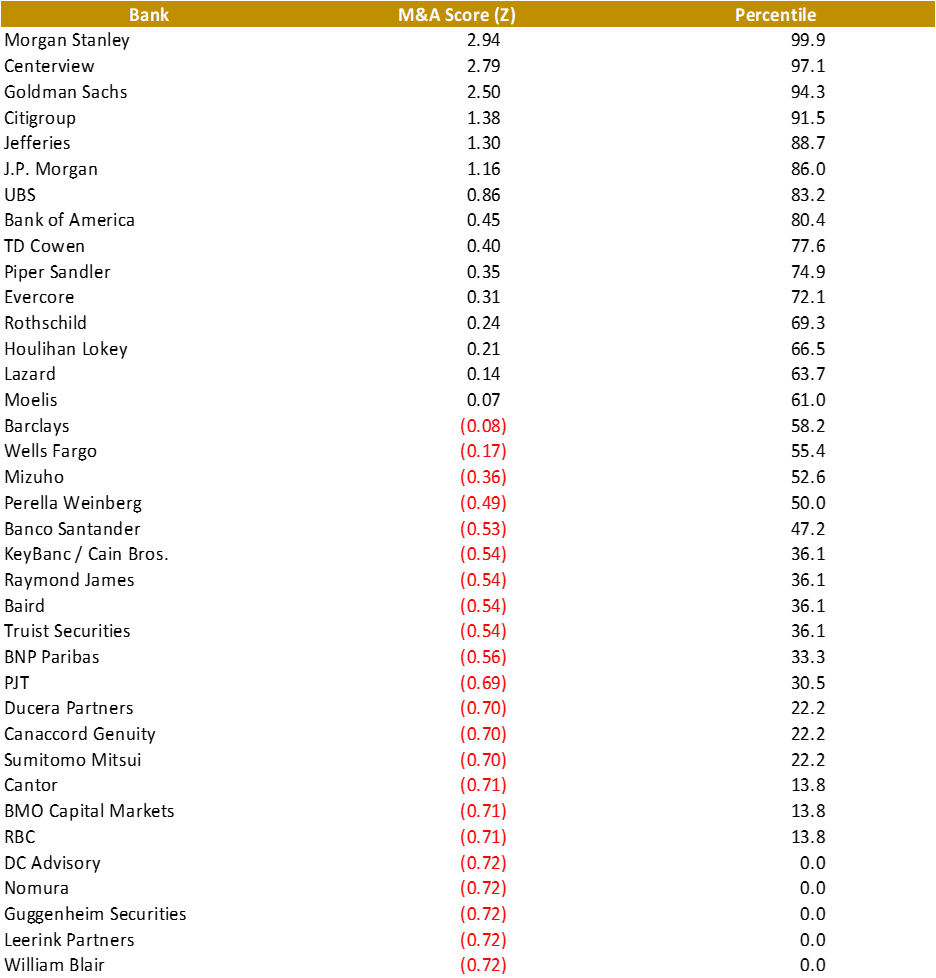

1) Biopharma rankings (2025 data)

This is a big focus of the post, given its uniqueness, and the area I’m most confident in.

And below are the two biopharma rankings I’ve created:

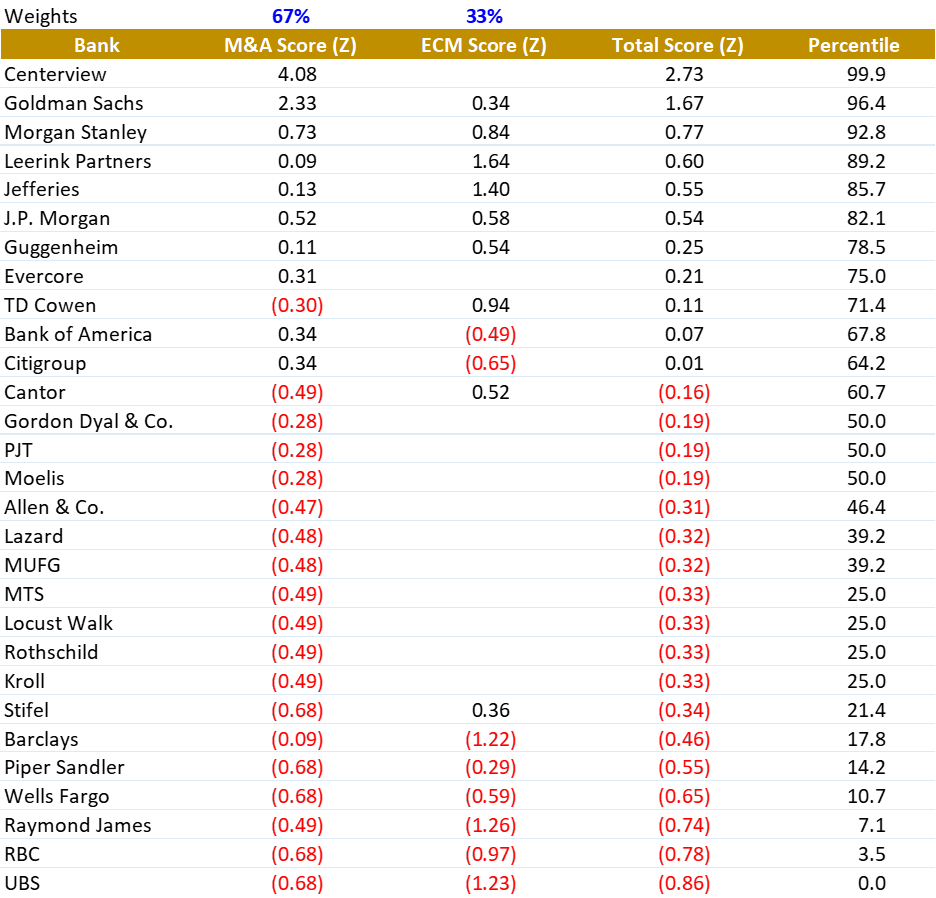

Biopharma objective ranking (data-only) – 2025

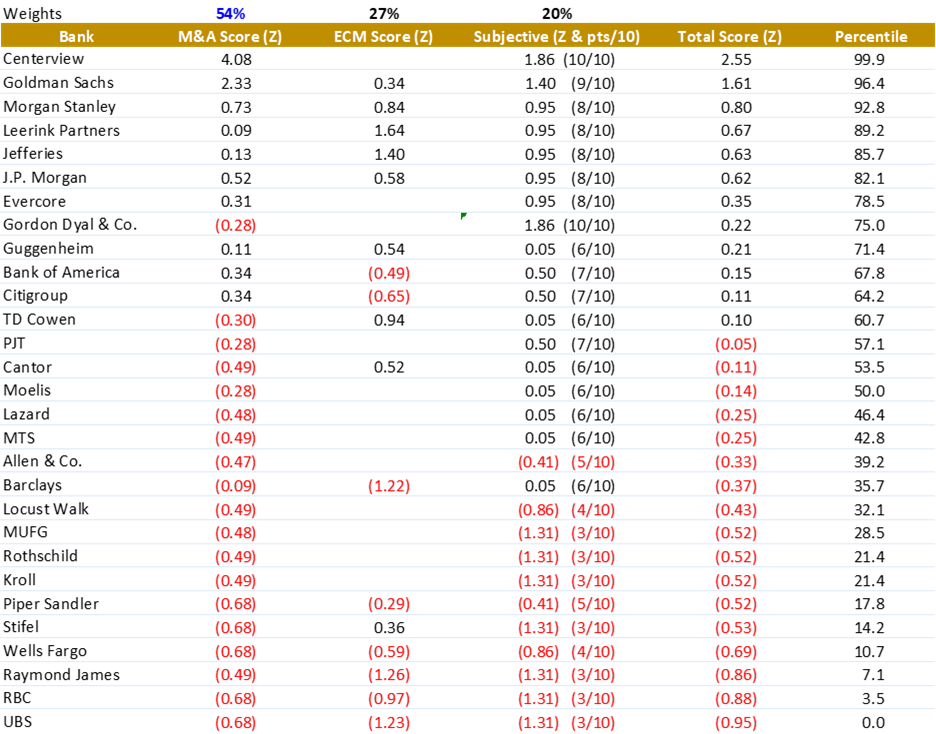

Biopharma hybrid objective/subjective ranking (80% Data + 20% Subjective) – 2025

2) Broader healthcare rankings (2025 Data)

This is the area I’m less familiar with. Generally, for broader healthcare, ECM is much less of a focus, hence only ranking for M&A. I’m publishing it because people ask for it, but treating it more cautiously and I’m open to serious feedback. Note: the Broader HC dataset was compiled using FactSet of NA/UK deals above $100M in total deal size (quick scrub), so others may have better sources that could be leveraged or can help provide additional color/subjectivity to eventually create a hybrid ranking.

Based on the most helpful WSO content, here’s a breakdown of the key points and methodology behind the rankings for Healthcare IB groups, particularly in Biopharma and broader Healthcare:

Why This Guide Stands Out

Key Methodology Highlights

Avoiding League Table Pitfalls:

Biopharma Rankings:

Broader Healthcare Rankings:

Why This Matters for Students

Takeaways for Biopharma and Broader HC Rankings

This guide is a valuable resource for anyone navigating healthcare IB recruiting, offering a balanced and data-driven perspective that cuts through the noise of traditional rankings.

Sources: Credit Suisse, Barclays, and Jefferies Healthcare, Biotech finance part 2: valuation methodologies and modeling considerations, Questions about Healthcare M&A, Biotech/Life Sciences Vertical in IB: Day to day

Subjective Biopharma tiers with commentary/rationale (subjective score, hybrid percentile)

Gold Standard

Top decile (90th to 99th percentile)

Second decile (80th to 89th percentile)

Rounding out the top quartile (75th to 79th percentile)

Second quartile (50th to 74th percentile)

Bottom 50% (below 50th percentile)

finally looks like this post is now up after being stuck in purgatory, this was mainly written over the course of last weekend and have had some more time to think and plan on slightly changing some of the subjective scores this weekend, i.e. Moelis to an 7/8 on the subjective score and UBS a higher subjective score with the recent hiring of Michael Yee (aka Yeezus) who is one of the top equity research analysts in biotech that was hired from Jefferies and is certainly going to help them get on some syndicates

MS also just lost their Chairman of Biotechnology IB Jessica Chutter who is retiring.

Evercore poached Ben Carpenter from JPM who is a biopharma banker.

UBS hired a trio of biotech bankers from RBC.

Can you opine on how those moves will affect rankings?

And Lazard poached biopharma banker Gabor Szabo from Moelis

Wow thank you so much for taking the time to create this!

This is all great but what exactly does an analyst learn after 2 years of doing follow ons or co-manager IPO roles for Leerink or whatever? For what most WSO student-like members look for Biotech ECM heavy ranking is worthless.

Totally fair to prioritize M&A, and that’s why it’s weighted about 2x ECM in the model, so I wouldn't call this "ECM Heavy" unless a lot of others disagree. "ECM Heavy" to me would be giving each equal weighing.

But I think calling biotech ECM “worthless” is exactly the common bias on here that I’m trying to push back on a bit. In biopharma, a lot of analysts ultimately care about buy-side optionality, and the people who leave tend to skew more toward VC/growth investing than traditional PE, with some even opting to work on the corporate side. Pure M&A reps translate great to PE mostly because PE cares a ton about modeling and process, but biotech ECM (i.e. working on IPOs/Financings) is what forces you to think like an investor: you’re constantly selling and defending the company’s story, explaining why investors should care, how the data is differentiated vs competitors, what the regulatory path looks like, and where the real risks are. You learn how to separate “spin” from substance because you see, in real time, what actually convinces investors and what gets shredded in diligence. That judgment is incredibly transferable if you want to evaluate companies on the other side.

So yes, M&A is the backbone and should get most of the credit, but i'd argue that going to a platform that gives you both strong M&A reps (modeling/process) and real biotech ECM reps (investor mindset) is what maximizes optionality in 2 years while you figure out whether you want PE, VC, work on the corporate side, or stay in banking. If you're dead set on PE, then go to a M&A-only platform, but if you want optionality then go somewhere that will give you a mix of ECM and M&A reps.

But what are the analysts doing other than internal memos? EOD IPOs can be a great learning experience but problem with biotech is most are pre-revenue phase 2 couple of pipeline drugs which tbh isn’t analyst isn’t figuring out the efficacy on. If you are MD/PHD type person sure.

^I’m not sure if you’ve had direct experience in your career working on biotech financings or IPOs as a lead-left bookrunner, but based on nearly a decade doing this and watching tons of analysts and associates develop underneath me, biotech IPOs and financings are not “just internal memos.” The closest thing to what you’re describing is the fact sheet / script every bank keeps for its ECM origination team so they can do investor calls and not sound lost, and that’s maybe 5-7% of the work. The rest is high-impact work where you’re translating messy technical science into a clear, defensible investor narrative: what the endpoints mean, what the trial design implies, what’s clinically meaningful vs noise, how durability and safety will be interpreted, and how the program stacks up versus competitors. You don’t need an MD/PhD to do that well because you’re not inventing biology, you’re synthesizing inputs and pressure-testing the story using the same tools investors use (research, KOL work, comps/precedents, positioning) so you can anticipate the real pushback.

And analysts/associates aren’t just observers in that process, they often take first passes and give comments directly to the company on their data decks and presentations: what to emphasize, what to highlight, what to de-emphasize, and where you might be over-showing something that just invites investors to pick holes. You also see investor feedback in real time across different investor types, and you’re directly shaping messaging as that feedback comes in, alongside the financing mechanics (pricing, dilution, financing-hangover risk). M&A is absolutely important (and it’s weighted 2x ECM in my model for a reason), but in biotech, these financing/IPO reps are some of the most directly translatable skills for becoming a strong VC-style investor - underwriting risk/reward off imperfect data, identifying what truly moves the needle, and learning how real money reacts to a story in real time. And I’ve seen plenty of people without science backgrounds do very well on the investing side because the edge is synthesis and judgment, not letters after your name.

Great list. Thank you for doing this

very helpful!

Great for those pursuing banking as a career. Wld caution those looking to exit to HC PE / Biotech HF / life sciences VC investing to assume this list of group caliber in winning or executing mandates = ability to transition to selective investing roles.

The Citi or Jeff HC banker will still have a harder time than the GS/JPM HC banker, and similarly true for LAZ/MOE vs a TD Cowen / Cantor Fitzgerald

Do you think exits at a growing pharma group like Jeff/Citi will improve in the coming years, assuming current trends? Wondering as an incoming SA.

^Jefferies has been doing an amazing job over the past year. The Phil Ross hire has clearly brought them a ton of M&A momentum/credit, and it really feels like they’re putting Centerview in their place a bit on certain mandates, and they're still a top bank in the IPO/Financing space.

One underrated signal of franchise strength is who can actually convene the market. The JP Morgan Healthcare Conference in SF (happening next week) is still the definitive biotech conference - everyone drops what they’re doing, comes to SF, hotel rates go insane ($2,000/night at 3-star hotels), and you basically have to be there if you’re a company, investor, pharma exec, or banker. What’s been interesting is Jefferies has basically built a second JPM-like anchor event with Jefferies London in November. Especially after this year, the consensus I’ve heard is that Jefferies London is now the clear second JPM-like week on the biotech calendar, especially for european biotechs/pharmas. So if Jefferies keeps compounding like this, I do think exits should keep improving over time.

I can't really talk to Citi that much as I haven't seen them make any huge moves/hires that banks like Jefferies/Evercore/Leerink/JPM have done over the past year to bolster their M&A teams.

Jefferies urgently needs to find a bigger hotel to host that conference in.

^ totally agree. I think after this year though they'll definitely have a bigger venue next year. Saw a video of Brad Loncar of BiotechTV interviewing Phil Ross at the conference and if they had a bigger space they definitely wouldn't be doing it smack dab in the middle of the check in area with so much background noise.

Jefferies London: Jefferies Chairman of Global Healthcare Philip Ross discusses the environment for biotech and deals

also protip to students: BiotechTV, FierceBiotech, StatNews, and Endpoints are the best biotech news sites to reference what's going on in biotech.

Cowen is leagues above Cantor

Very informative read. Thanks for putting this together.

Wow i'm surprised Leerink's healthcare services group really ranks that low on the broader healthcare rankings. They presented to us back in November and while the biopharma team/MD were really impressive with their pitch, they sent over an associate to represent and pitch the healthcare services team and the associate was saying braggadociously that they're a top group on the street and that they work with some of the biggest payors/providers/companies.

Former Leerink junior here. Take that healthcare services associate’s pitch with a massive grain of salt. Unless Services is your absolute last resort or you have a burning passion for the space, do not prioritize it over Biopharma. The healthcare services group has been in disarray since the group head left for PWP and deal flow has been drier than the sahara desert for years. The internal consensus is that the group is a drag on firm profitability and is likely only kept alive so leadership can push the narrative that they cover all of healthcare rather than just being a biotech shop. I wouldn't be surprised if the group gets axed. Consequently, most juniors are looking to lateral, especially given the worse culture and lower pay.

If you already applied to Services based on that info session, i'd reach out to the campus recruiting team immediately to switch your preference. You also need to be careful when networking with the services team because they have a history of funneling strong candidates into the Services pipeline regardless of what the candidate's actual preference is. I heard of this happening to a rockstar intern a few years ago who got maneuvered into a Services seat by a senior banker who was fond of him despite his first choice preference being Biopharma. I heard he ended up doing the smart thing and grinded Biopharma technicals on the side during the summer and immediately re-recruited to a top EB for full-time (Centerview/Dyal) rather than accepting the return offer. He almost certainly would have stayed had he been in the Biopharma group, so don't let yourself get trapped in that position. you'll have a much better experience on the biopharma time and get much better exit opportunities.

There's another thread I saw on here a couple weeks ago that really accurately lays out the culture at Leerink between the different groups and offices: Leerink Partners Culture? | Wall Street Oasis

What happened to Lazard Healthcare? Have heard mixed things lately on this forum around hiring philosophy etc. can anyone confirm?

Left to Leerink. Lazard is dying unfortunately

Lazard was just announced to be on a sizeable deal today, representing Orna as the exclusive SS advisor on their $2.4B sale to Lilly. TBH a lot of the commentary I've seen on WSO that the HC group is dying/withering is overblown, they're still a solid group. Congrats to the Lazard team!

Lilly to acquire Orna Therapeutics to advance cell therapies | Eli Lilly and Company

List way too biased to the short run. Anyone in the industry knows that a ranking based on a single year is absolute brain rot and has no utility. Banking groups move up and down based on a number of factors. While year on year deal flow changes, legacy is usually cemented. You can run the same analysis for tech and start saying MS Menlo fell off or you can just accept some groups have been stronger for decades and decades and will have that legacy pulling for them. That’s what matters for exits. Centerview really joined the spotlight in the last 3-5 years and will def be a solid name. That said, they don’t have the legacy; thus, exits are legitimately aweful.

Guarantee you this list will flip on its head 3 years from now and it won’t matter. Legacy is what groups are ranked on and is what analysts should optimize for.

Awesome list - unrelated but any advice for an incoming biopharma analyst to be successful? Interned in another industry group and have no previous biopharma experience/science background.

I’d give the Pharmagellen biotech guide books a read “guide to analyzing biotech clinical trials” and “guide to biotech forecasting and valuation” as they are pretty solid. Also take the Breaking into Wall Street course on pharma modeling.

Pharmagallen book is a good read the framework is very useful

Could anyone share good biotech financial models or resources (e.g., rNPV, licensing models, deal valuation, etc.)?

Thanks in advance!

Use the Breaking into Wall Street pharma modeling course, it’s super solid and is great preparation

Wall Street Prep Biotech Sum of the Parts Valuation

Google this this is a good course

Where do likes of OpCo, Truist, RJ fall?

I haven't seen them on the biopharma M&A side but they do show up on the ECM side, mainly as like a 10% econs fourth bookrunner or co-manager role. They usually are brought on very late into the process right before the deal flips public

Very informative read, would argue it suffers from quite a bit of recency bias, but incredible insight nonetheless.

Thank you for wasting an afternoon on this weak project intern! Three reasons why this is neither a “data-driven”, nor “definitive” ranking.

Announced M&A is not equal to fees nor contribution, especially in biopharma where sell-side and buy-side experience are valued separately and where it is hyper common for 2 or 3 banks to take each side. Unless you have an adjustment for when the bank is primary advisor on a deal, I wouldn’t blindly take deal-value and call it a day. In fact, I think it’s reckless running data analysis on incomplete/inconsistent data— just keep the discussion qualitative if you’re unable to find proper numbers or else you’d guarantee to make mistakes.

2. Though computing a Z-score doesn’t require the dataset to fit a normal distribution, the interpretation and usage of Z-scores heavily depend on the shape of the data. That’s to say it’s absolutely juvenile to approach the analysis the way you did and sum + rank Z scores when the population data is obviously skewed in the first place. If you’re going to make an attempt to substantiate your view with data, maybe revisit an intro statistics class to familiarize yourself with the fundamentals and prevent sloppiness in the future.

3. Lastly precedence is king in this industry and whatever 1-3 year rolling data you use is meaningless within the context of group strength.

This isn’t very high quality analysis :/

Just finished JPM week so now I have the time to respond to this. No offense, but the level of hostility in your message is really weird and makes it seem like you have the temperament/demeanor of a first year analyst trying to defend their firm’s honor on WSO because their bank/group didn’t land where they wanted it to land. If that’s what’s going on, fine, but then the productive move is to give actionable improvements, not try to tear down the whole thing as if it’s worthless. I literally said in the post I’m not claiming perfection and I want serious feedback so it can improve over time.

Now, Before this 99% of “rankings” on here were just vibes, brand name, who had the big fan clubs, and people arguing in circles with zero transparency. At minimum, this is a concrete, explicit framework based on real deal activity, and if you don’t like an assumption, you can point to it and propose a better one. That alone is already a massive step up from the random “S tier / A tier” posts created by 1st or 2nd year analysts who don’t really know what they’re talking about.

On the substance, I actually agree with one of your main points on M&A crediting. If co-advisors and primary advisors are getting treated the same in a purely mechanical dataset, that can inflate perception, especially on mega deals. I’m happy to adjust the model so primary advisors get more weight than co-advisors, similar to how I treated ECM lead-left versus passive bookrunner roles. If others agree, the cleanest tweak might be to either give lead advisors a 1.5x multiplier or discounting co-advisors to something like 2/3 credit.

On the “only using 2025” point, that wasn’t random. Markets and franchise strength are not static, and the last year had an unusual amount of senior movement and platform change, which in a lot of cases dramatically changes the deal flow dynamics of a group. Really the only place that I’d argue would have a “Ship of Theseus” like dynamic going on in their ability to win deals regardless of which senior bankers are on the platform is Goldman Sachs just based off their brand name, i.e. it’s like the old time saying that no IT manager will ever be fired for choosing Microsoft over some unknown vendor. A longer lookback can absolutely be valuable, but it can also bake in history that doesn’t reflect the current team or current momentum. I’m open to adding a second version that uses a longer window (e.g., 2 years) alongside the 1-year view so people can see both “current-state” and “through-cycle” rankings.

On the Z-score point, the irony is you are describing the exact problem the log transform is meant to fix. Deal value is heavy-tailed; if you do not compress the right tail, a couple mega-deals dominate the signal and the output becomes “largest deal wins” with extra steps. I used log-adjusted values so the scale is less outlier-driven, then Z-scored purely as a normalization step to put different pillars on a common SD-based scale, not to claim the data are normally distributed. If you or anyone else think a more robust approach is better (percentile ranks, winsorization, median/MAD, etc.), I am happy to run it and see what changes.

And just to be clear: judging by the other comments, it seems like plenty of people agree this is useful and are engaging with it in good faith. If you want to make it better, I’m open to that. Nasty posts that try to denigrate and tear someone down are one of the biggest reasons why people don’t take the time to post on here and help other students.

get rekt anon

What about HL?

Not biopharma. HC services. Maybe some pharma services as well.

^Ya i agree with @CapTableTriage, I personally have never seen them on a biopharma M&A process before, so I am assuming that they are more broader healthcare oriented which HC and pharma services would fall under. Maybe we need someone to step up to become @The_Broader_Healthcare_Banking_Expert

Thank you so much for putting this together. I have exploding offers between two top groups that I'm really torn between, do you mind if I PM you?

Absolutely, feel free to PM/DM me, happy to give my two cents.

bump

Thanks for making this, GOATED.

Excellent contribution to this site! +SB!

I really enjoyed this post. It was nice to see data driven rankings. Is it possible for you to do more rankings like this for other sectors like Tech or Industrials?

stifel 2026 BiopharmaMarketUpdate this is the recent one the previous ones are equally good, they also have themes like Oncology vs Immunology

is there any WSO Mentor who are in life sciences Investment Banking? Thank you!

^feel free to DM me

feel free to reach out

woohoo 2026 Midyear Outlook for Healthcare Investment Banking J.P Morgan is up , must read!

Are Citi and Leerink better now? Given the GSK nuvalent deal?

not sure about Citi, but man Leerink had an amazing week, they not only did the GSK/Nuvalent deal, the largest M&A deal in 2026, but they also were the lead-left bookrunner on the Parabilis IPO, the largest biopharma IPO ever, outdoing the Moderna IPO.

Also, a lot of people have DM'd me on when I plan on refreshing the ranking, I plan on doing it near Dec. 2026 when stuff gets slow since it takes a while to do and is just before when summer analyst recruiting really kicks off.

I guess if I had to redo the rankings, I would give Lazard and Moelis a much higher subjective score, as both have had a great year, especially Lazard.

On the note of DMs, I'm more than happy to take any questions or give any advice, just note that I check this account very sporadically and I get a lot of DMs, so don't be surprised if it takes a while for me to get back to you.

@The_Biotech_Banking_Expert curious to hear your take on how you read advisor roles on multi-bank biopharma M&A deals, especially ones where Centerview isn’t involved.

For example, on the recent $10B Crinetics / Vertex deal, JP Morgan and Leerink Partners were both listed as sell-side advisors and then Morgan Stanley and Lazard were listed as the buy-side advisors. Beyond just the ordering of names in the press release and filings, how can you usually tell whether one bank was really leading the process versus both being more or less equal co-advisors?

Are there any other specific tells that people in the industry look for?

Molestiae velit qui nobis suscipit delectus aut dolore. Odit id ullam vero non similique accusamus voluptatibus est. Beatae est possimus qui autem. Rem voluptatem saepe et dignissimos. Corporis esse consequatur sed autem aperiam.

Et non eius sunt rerum est placeat corporis voluptas. Aperiam consequatur dicta natus est odio natus qui. Necessitatibus hic voluptatum sunt. Incidunt aut explicabo et atque quia et.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Qui et consequuntur fugit voluptatem culpa vitae est. Et necessitatibus illum fugit. Molestiae quae maxime omnis necessitatibus animi vel. Veritatis qui sit eum fugit.

Dignissimos at natus molestiae ipsa in. Ea ipsam quos iusto debitis. Maiores sunt enim totam ea.

Modi eaque facere tempore aut quidem aut laborum. Cupiditate error magnam et. Labore est voluptatem et cum. Et est non neque.

Animi quia illum voluptatum aperiam rerum. Voluptatem sunt nisi dolore ducimus cum cum quis. Ex commodi est quaerat rerum. Ipsa voluptas cupiditate deleniti aliquid. Rerum odit dolorem ea vero ratione laudantium quia.

Optio ut et nemo omnis culpa. In qui voluptatem qui voluptas est praesentium quod ducimus. Et sed magni quod. Dolores repellendus reprehenderit et non. Accusantium in cupiditate debitis nesciunt.

Iste cupiditate vitae neque et commodi modi vel. Deleniti quam rerum quia quia repellendus quo. Aut et quo voluptatem exercitationem eveniet qui.

Culpa est rerum maiores magnam. In veniam excepturi quia sed numquam sit qui.